Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Trevor Castledine

Senior Director, Private Markets

Amid the seemingly never-ending ‘hunt for yield’, high return real estate debt strategies are attracting investors’ attention. How are today’s asset managers seeking to deliver 7-10% net returns in this relatively conservative asset class? New research shows funds using a variety of levers in search of results.

Many investors are familiar with real estate debt in its more conservative form: a safe-as-houses replacement for core investment-grade fixed income, generating a hundred or so extra basis points per year with low Loan-to-Value (LTV) ratios (50-55%). Adding a bit more flexibility in terms of collateral type, geography or LTV (e.g. 65%) can boost the premium to 300-500 basis points per year, giving returns of approximately 4-6% in Europe and 5-7% in the US.

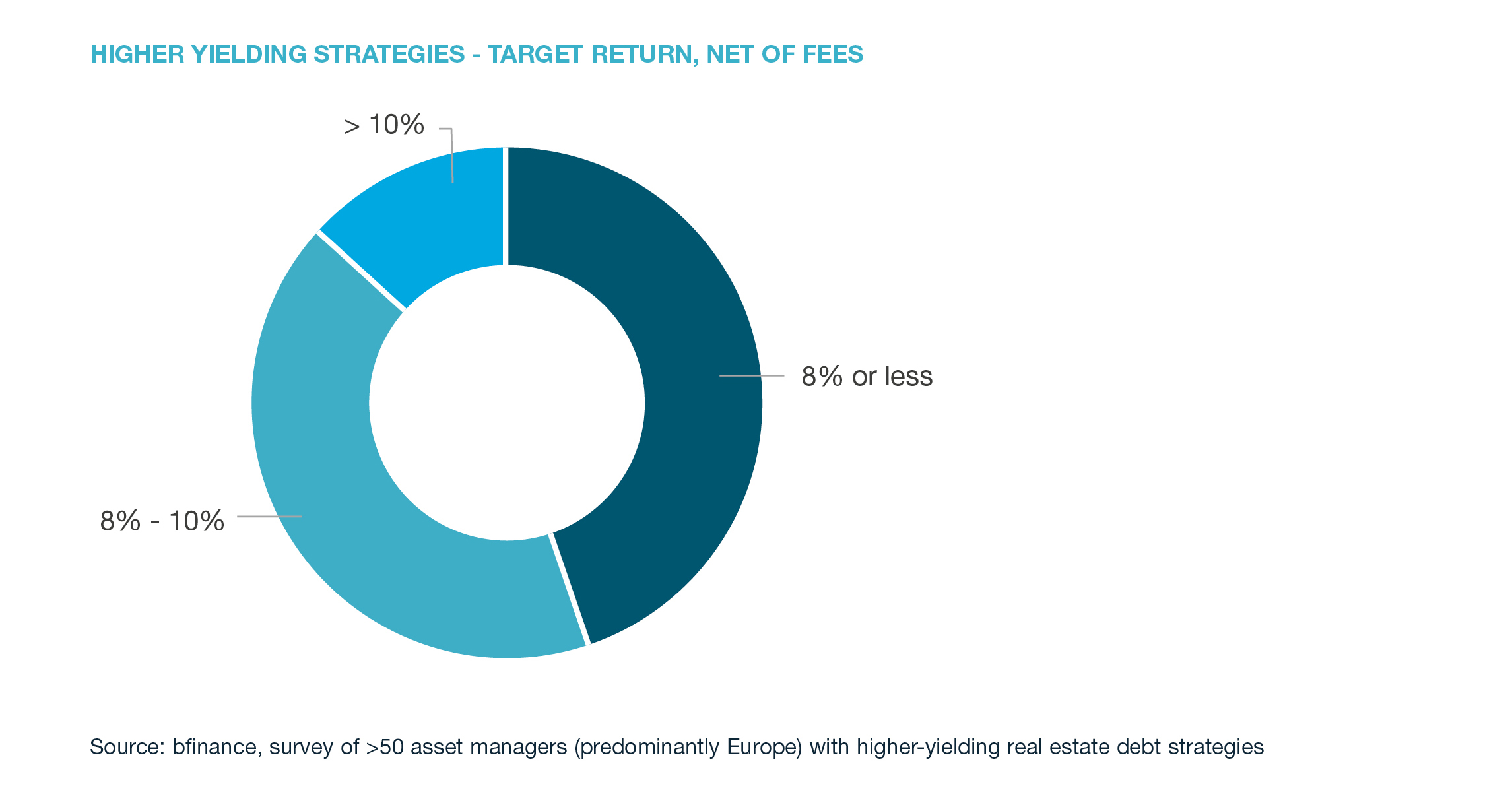

Yet the asset class also has a higher-yielding side. Investors who are prepared to take on still more risk will find an increasingly wide variety of offerings delivering net-of-fee returns of 7-10% per year, if not more. Demand for these punchier strategies among bfinance’s international institutional client base grew significantly in 2020 and has remained strong in 2021.

We see such investors using such strategies in a range of ways: they can complement high yield bond portfolios, bringing diversification and volatility reduction; they can sit alongside private corporate debt, with similar returns – but very different risk exposures; they can even supplement property portfolios, with minimal (if any) reduction in target returns versus core/core+ real estate equity strategies but meaningful diversification and faster deployment.

What are the main ‘risk levers’ in real estate debt?

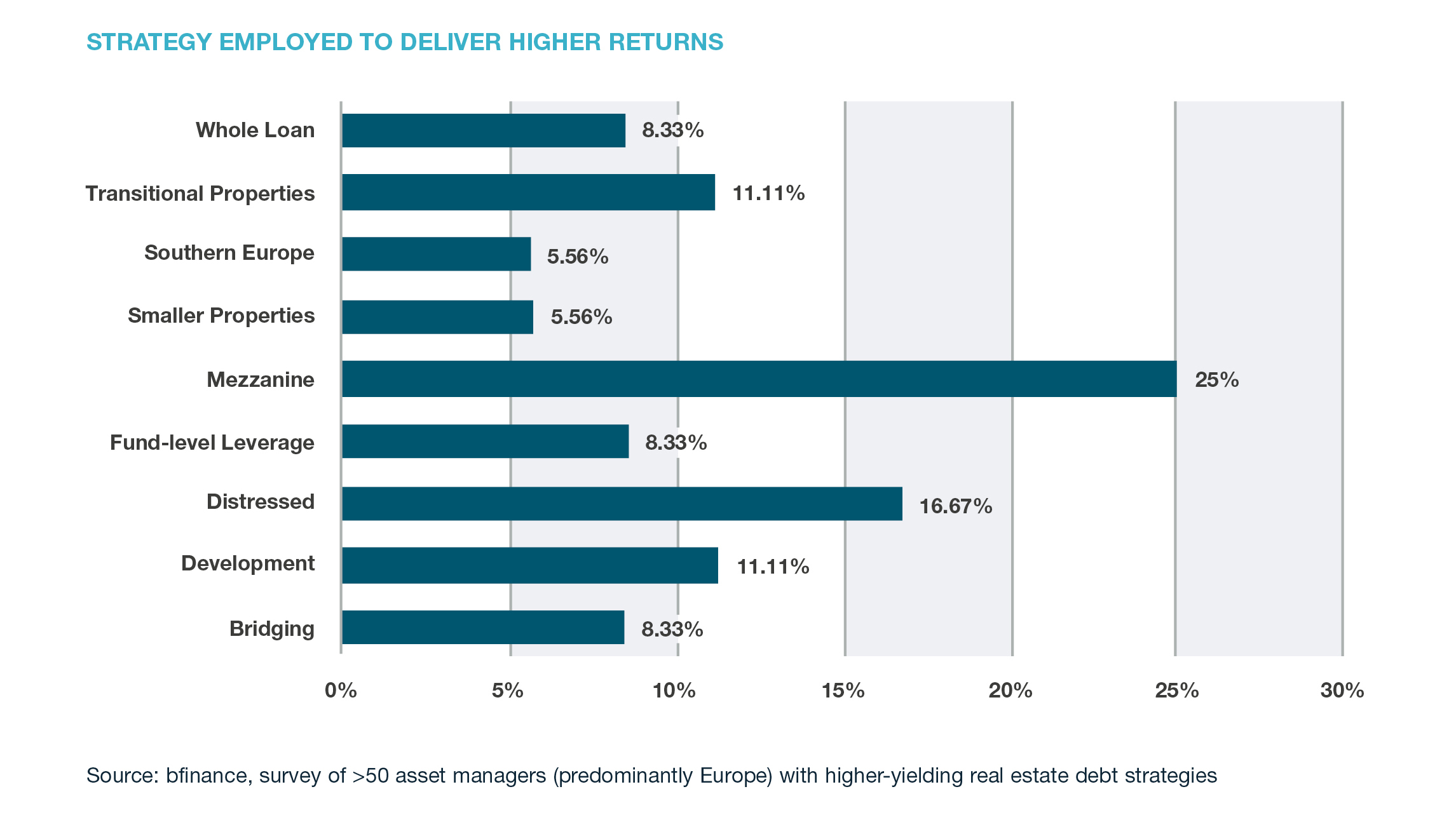

Crucially, investors must ensure that extra yields do not come at the expense of disproportionate increases in risk by understanding which approaches the manager is using to deliver an enhanced return.

Some of the levers have been popular for years: mezzanine debt and higher LTV ratios (whole loans), for example, have long been used to provide outsized returns; this trend was true even before the Global Financial Crisis (GFC), although the post-GFC regulations affecting banks’ capital ratios dramatically enhanced asset management opportunities in this and other private debt sectors. Others are becoming more widely used in today’s climate: newer strategy types are more likely to tap into specific niches, such as smaller properties, riskier geographies, distressed assets and development or bridging finance.

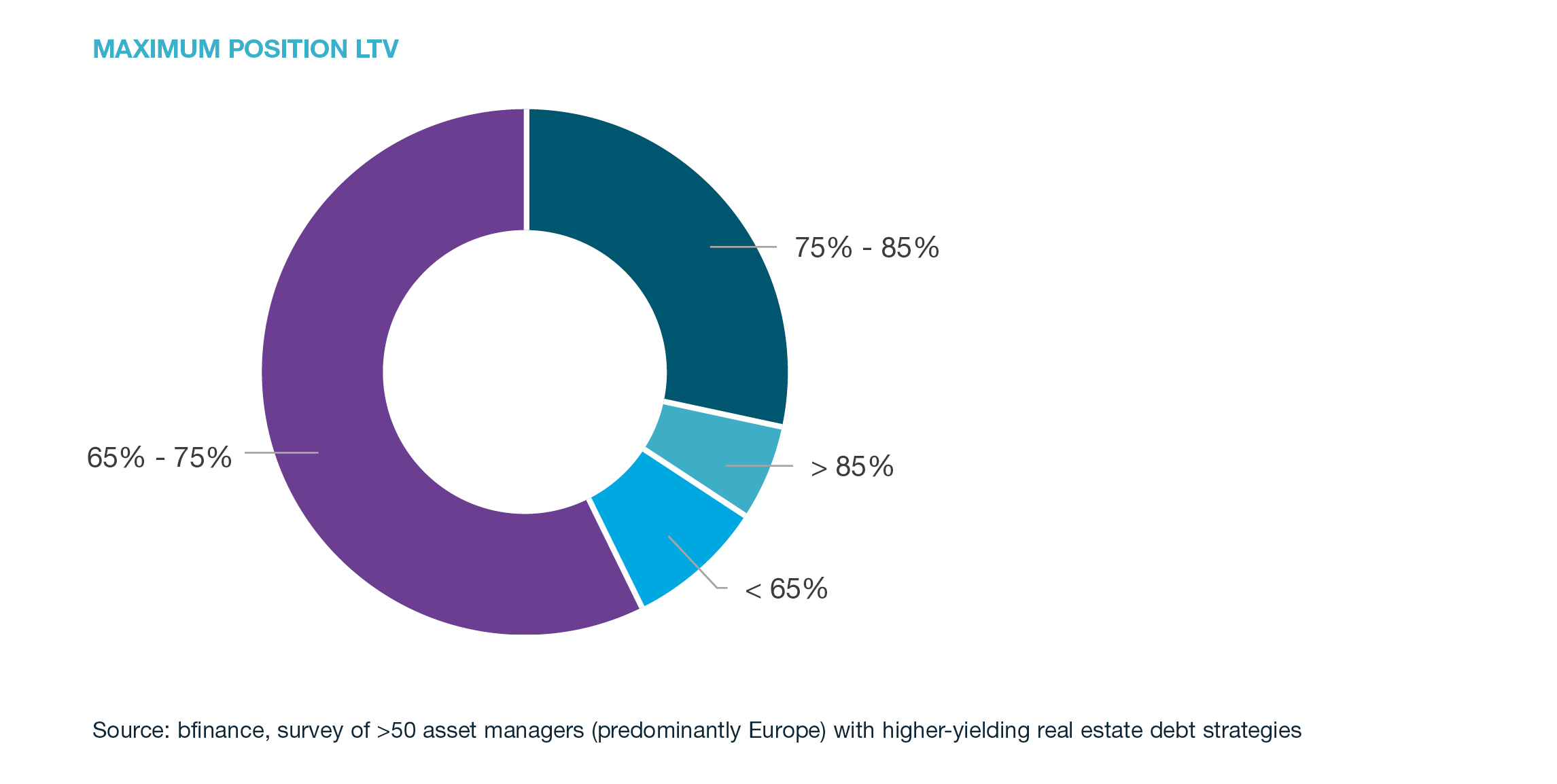

LEVER 1: INCREASE LTV RATIOS

We note that the majority of strategies captured here – nearly two thirds – are not pushing LTV beyond what one might consider a relatively ‘comfortable’ level of 75%.

Although equity providers are willing to pay higher margins on debt that covers a higher proportion of the cost of an asset, higher LTVs make it more likely that the lender will incur a loss if a default happens. Moreover, higher financing costs can also make defaults more likely. It can therefore be tricky to strike a balance between extracting a higher return and the LTV limit at which one feels comfortable. This is particularly challenging in the current Covid-19-influenced climate, since it is harder to establish property valuations with the required level of confidence.

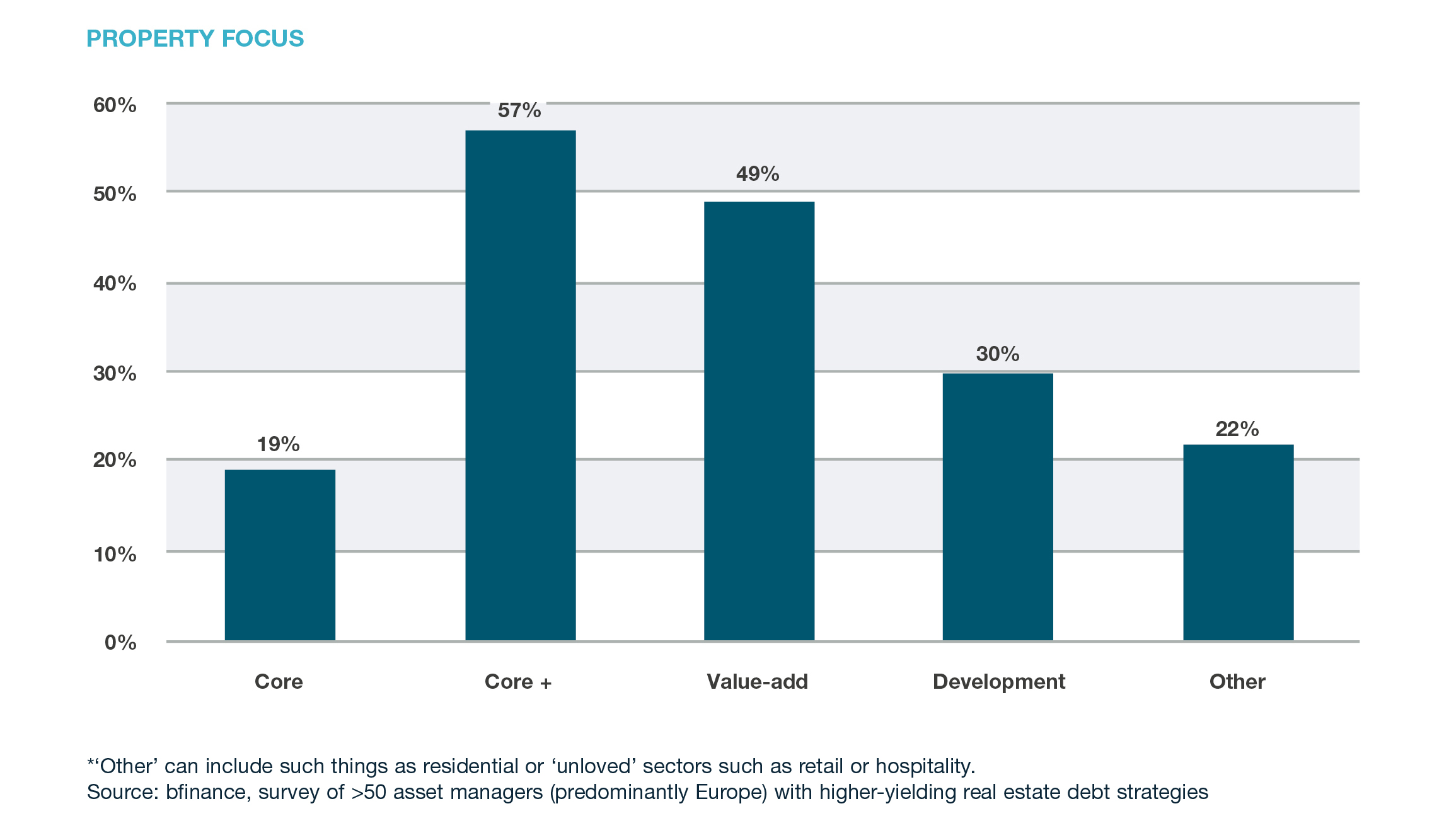

LEVER 2: CHANGE THE COLLATERAL

There is no shortage of lenders queueing up to work with owners who can offer the security of prime, stable Real Estate with blue-chip tenants on long leases. Financing other property types, however, can (often, but not always) command higher yields.

These choices result in very different risks. Non-core or cyclical property types might prove less resilient through economic cycles. Transitional properties, which might be untenanted or have tenants on short leases, can involve risks being taken on a successful repositioning or a change of use intended to deliver higher yields in future. So-called value-add property, where significant additional expenditure may be needed for refurbishment or even construction, brings further potential risks, and higher rewards yet again.

The chart above shows the percentage of managers that lend against the relevant type of property. Outside of the ‘IG’ world, most lend against more than one property type. Mezzanine and whole-loan strategies tend to focus on core+ and value-add properties, while strategies that lend against development properties tend to focus on first-lien debt at more conservative levels. Strategies that combine stretch levels of financing with higher-risk collateral are also available – and not for the faint-hearted.

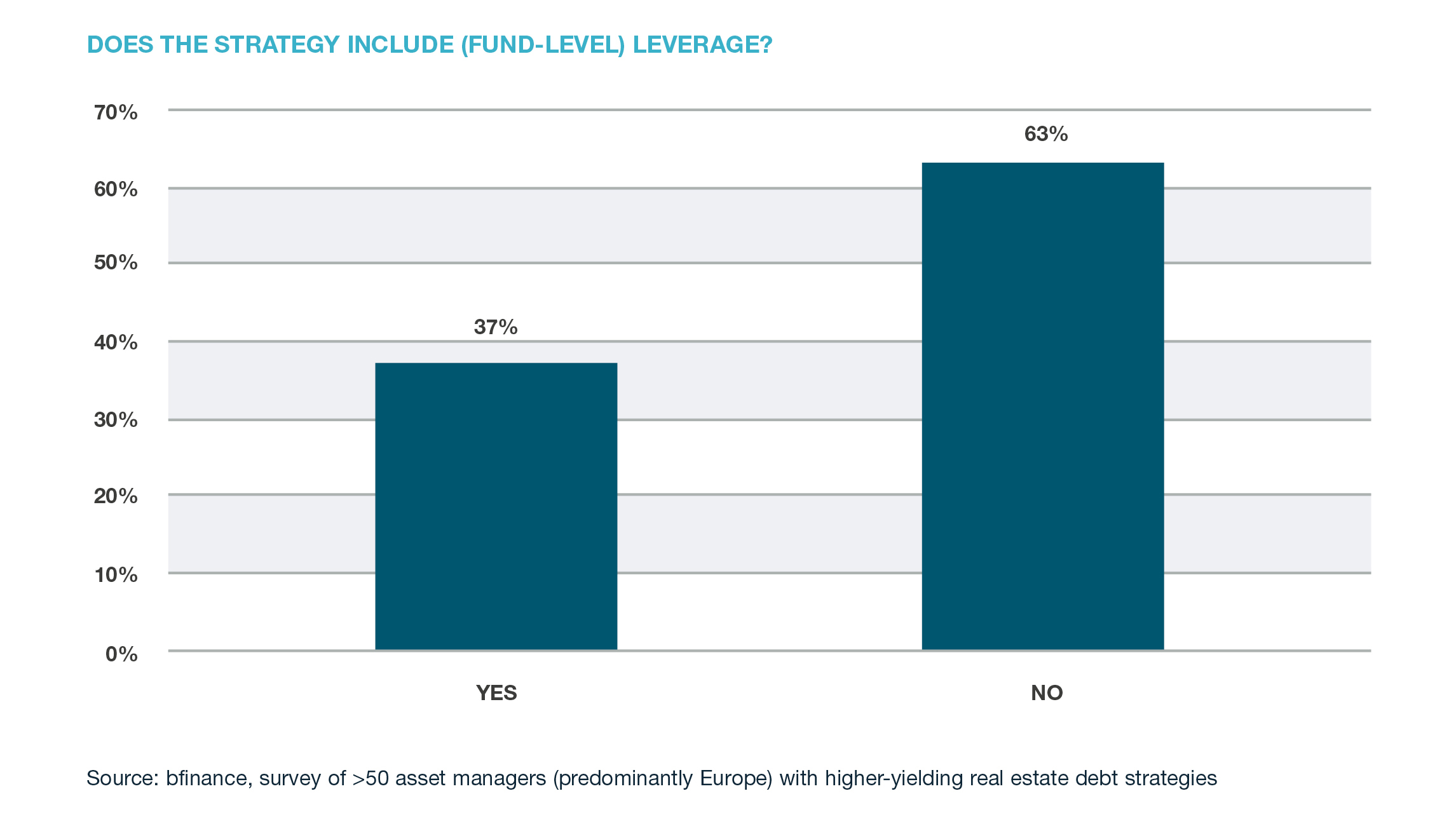

LEVER 3: ADD LEVERAGE

Fund-level leverage is used by more than 40% of the managers in this sample, although it may not always be the main source of higher returns. While most strategies seek to generate additional yield from the assets themselves, leverage can be an effective tactic for enhancing returns, particularly where the underlying assets are of very good quality and can therefore support higher leverage at a portfolio level. It’s important to note that the 40% figure would have been notably higher with a more US-oriented sample.

Aside from fund-level leverage, individual positions within the portfolio can also be levered. Mezzanine loans, for example, deliver higher returns but at the expense of subordination to other lenders and higher expected losses proportionately should something go wrong, although sensible structuring and a proactive workout approach can mitigate some of these risks.

LEVER 4: LOOK TO UNDER-SERVED GEOGRAPHIES

A minority of managers focus on regions that are less well-served by lenders, resulting in more attractive returns. Yet there is rarely a supply/demand ‘free lunch’: a weaker economy makes credit risk implicitly higher; some legal systems make it harder to take enforcement action when defaults occur. Geographical differences are not only relevant on a country-by-country basis: even within a single jurisdiction there may be higher-yielding locations. Local knowledge and targeted origination capability are needed to make these trade-offs profitable.

LEVER 5: SEEK DISTRESS

While lenders typically aim to avoid risk, significant upside can be generated by acquiring properties at a discount and then gaining possession through effective enforcement. This approach may generate little (if any) yield, but the overall IRR can be very attractive. Anecdotally, even ‘performing debt’ managers typically report higher returns overall from positions where they have had to take enforcement action. One doesn’t have to play the vulture: distressed properties that have historically been financed by ultra-conservative lenders might simply need a more flexible or higher-LTV solution in order to get through current difficulties.

Managers in focus

We see a number of different players now active in the higher-yielding real estate debt space, with different organisational backgrounds and a variety of capabilities. For example, the 2009-11 period saw teams emerge from the banking world, where they could no longer manage their product amid new regulations, and setting up their own fund management businesses. Many of these start-ups have grown and now have institutional quality teams and attractive track records. More recently, we have seen core senior lenders moving towards the higher-yielding parts of the market, as well as real estate equity managers who have spotted a gap on the debt side and moved to take advantage of the opportunity. Meanwhile, a number of corporate debt managers are adding real estate secured debt to their stable.

As attractive as this sector may now be, asset owners must ensure that investment managers possess the appropriate skill sets to deliver on their strategies. Most of the ‘levers’ above require very specific knowledge, experience and resources. And, as shown, managers are frequently using a combination of approaches to enhance returns. A critical eye on the alignment between strategy and capability is the key to successful manager selection.

ABOUT THE SAMPLE

The data presented above includes more than fifty asset managers with viable institutional-quality strategies in the ‘higher-yielding’ part of the real estate debt space. Readers should note that there is a European bias in the findings (due to the fact that this particular survey was conducted on behalf of a European client), whereas the overall real estate debt manager universe is highly skewed towards the US. Apart from geography, the sample is broadly representative. Fund sizes range from less than EUR250 million to more than EUR1.5 billion, with a median of around EUR500 million; these sizes are quite modest in comparison with more conservative strategies, reflecting the specialist nature of the asset class and the complexity of deployment. The vast majority (80%) of funds have closed-end structures, with a few open-end strategies which tend to be on the larger size.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.