Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada) Alternative Risk Premia & Alternative Beta

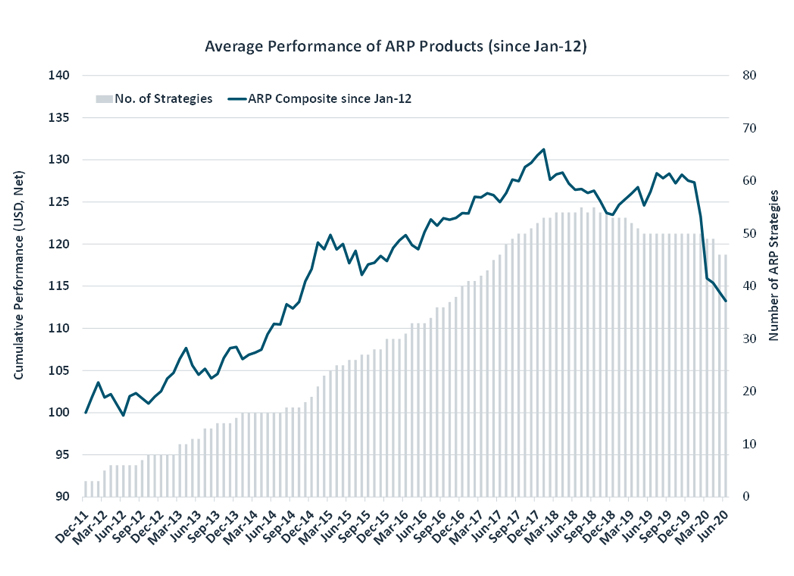

The no-longer-nascent alternative risk premia sector now features more than 50 externally managed strategies, an increase of more than tenfold since 2011. Investor appetite for ARP continues to be driven by a need for uncorrelated return streams and strong demand for low cost, systematic diversifiers.

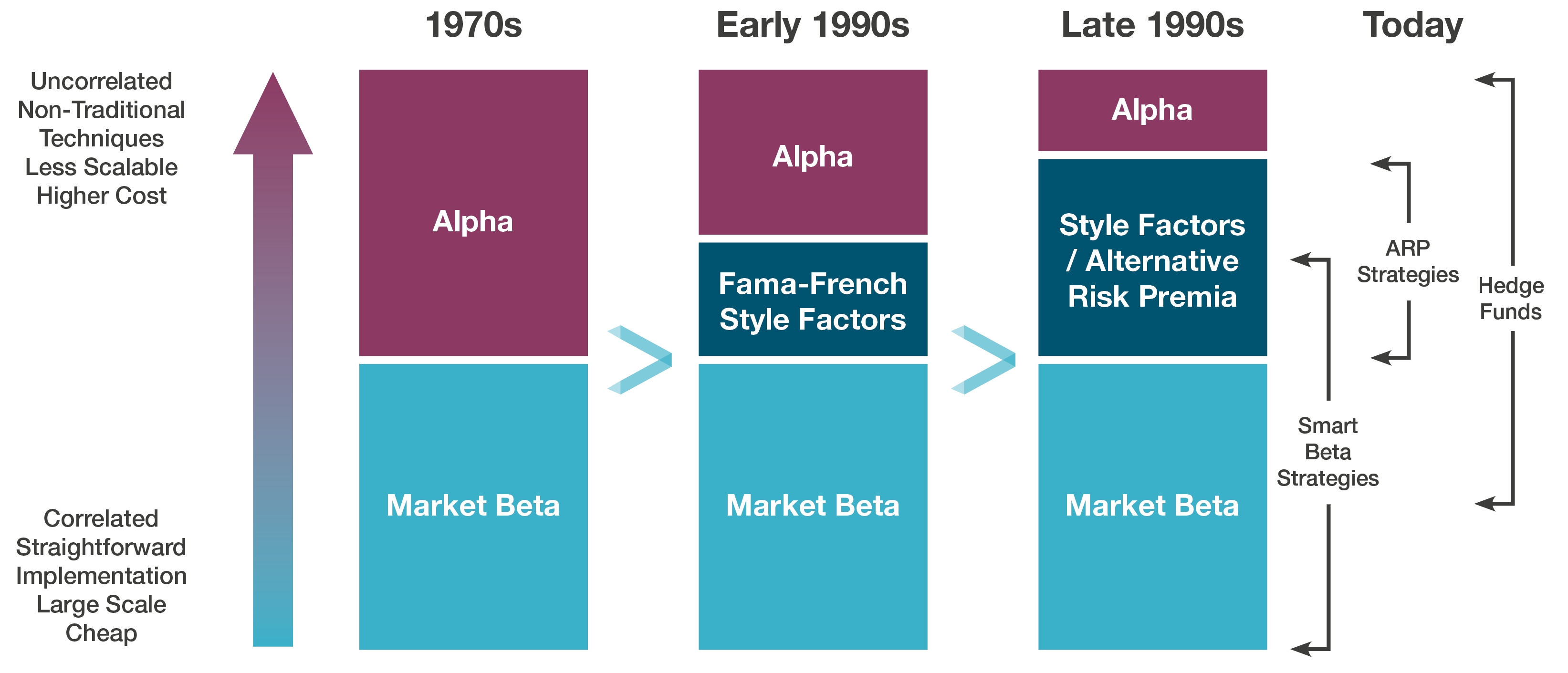

The rise of risk premia

The understanding of return drivers has evolved significantly since the early 1990s. Analysis of various markets, beginning with equities, has identified a number of “style premia” or "risk premia” underpinning excess returns that would previously have been considered “alpha”.

This paradigm shift has given rise to a number of industry developments. Smart beta strategies – long-only portfolios with tilts towards relevant style premia – have become a mainstay of the investment landscape. Active managers have adapted to compete in a climate where alpha is framed differently. And the recognition of such premia has also led investors to exploit them using non-traditional techniques, to deliver very low correlation with the markets in which those premia are found: “ARP” was born.

What are “alternative” risk premia?

Statistically, risk premia are defined by return distributions with a positive drift over time (the premium) and a negative skew (the risk). ARP are positive, persistent return streams which (1) can be generated using a systematic, rules-based process, (2) are largely uncorrelated from the underlying market from which they are generated (thanks to the use of non-traditional investment techniques such as shorting and leverage, as well as the use of derivatives and other synthetic instruments), and (3) can be explained, i.e. an economic or behavioural rationale exists for why they would have a positive expected return over time.

All ARP share a number of defining attributes. Formally, it should be:

- Attractive in having a positive expected return over time

- Explainable in having an economic rationale for why returns exist, either directly as compensation for bearing an identifiable risk, or the reward from exploiting an identifiable behavioural anomaly, or structural bias, of other investors

- Persistent in being present across time, having evidence (in and out of sample) that it is a rewarded investment approach

- Pervasive in being present across markets (different asset classes and geographies)

- Accessible in being both liquid and investible using a systematic investment process

At risk of over-simplification, the risk premia universe can be split into two broad families, although they are not mutually exclusive. “Academic” ARP can, in many cases, be described as market neutral (long/short) versions of so-called ‘smart beta’ strategies. They exploit well-documented premia such as value, carry, momentum and defensive. With some exceptions these can be implemented across the four main liquid asset classes (equities, fixed income, currencies and commodities).

- Carry: Higher yielding assets expected to outperform lower yielding assets

- Momentum: Tendency for recent price behaviour to persist into the future

- Value: Expectation that cheaper assets will outperform expensive assets

- Defensive: On a normalised basis, low risk / higher quality assets expected to outperform higher risk assets

“Practitioner” ARP, the second family, are systematic implementations of well-established strategies typically employed by hedge funds. These include merger arbitrage, trend following, volatility arbitrage, event driven and seasonality/flow. These strategies tend to be based on recognised behavioural anomalies or structural biases. This group are sometimes referred to as “hedge fund betas.” More recently we have seen the “practitioner premia” space branching into different segments: more “macro-like” ARP, where the timing of premia exposures and adaptive portfolio construction are important source of return, and complex ARP strategies which border on multi-strategy hedge funds.

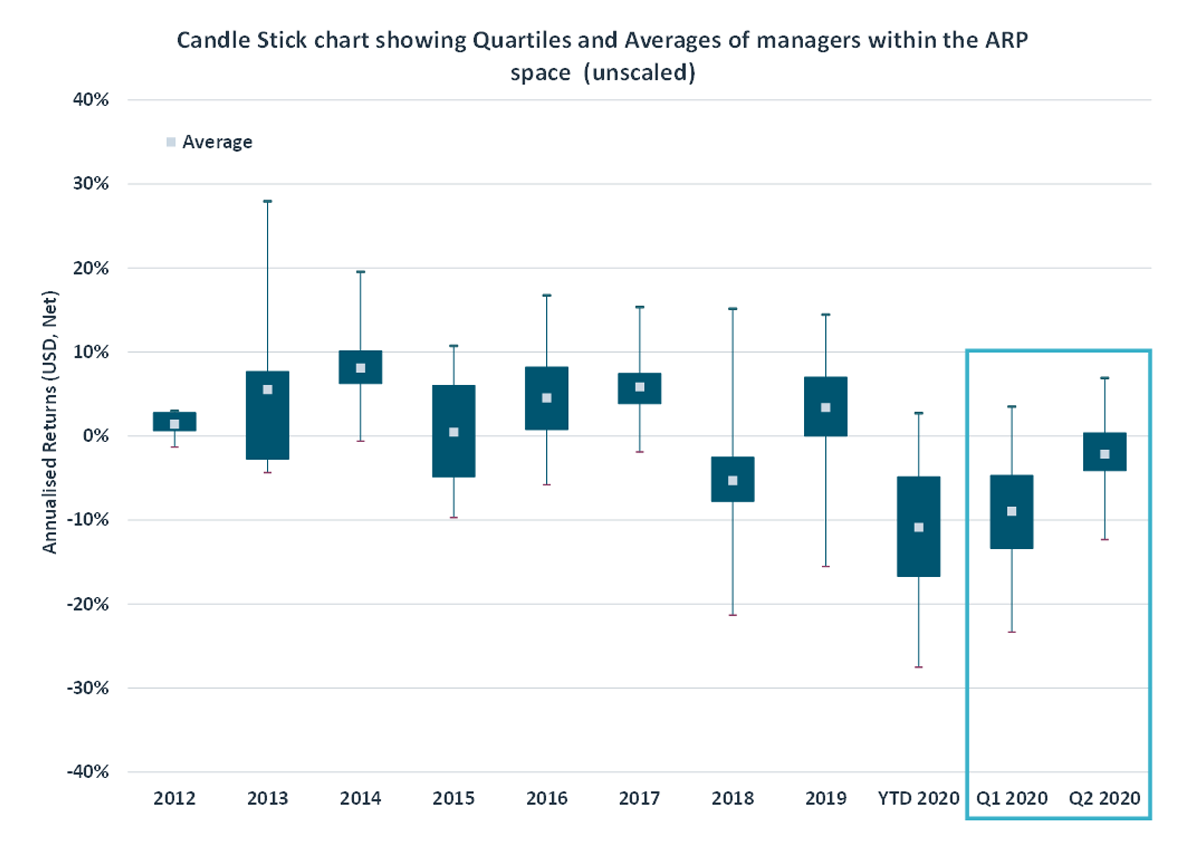

How have ARP strategies performed?

Over the longer term, an expected risk / return ratio of 0.6 – 0.8 is not an unreasonable assumption for the ARP universe. However recent performance has highlighted the differences between the asset managers in this space, with relatively high performance dispersion arising from both premia selection and implementation approach. This underlines the importance of careful provider selection in the ARP space.

Return dispersion aside, the diversification characteristics of the ARP universe have remained exceptionally strong, with average equity betas typically around 0.1*, and generally low pairwise correlations amongst ARP managers.

* Rolling twelve-month beta of ARP managers to the MSCI World was 0.07 at March 31st 2019.

Alternative Risk Premia & Alternative Beta

Benchmarking Alternative Risk Premia

Benchmarking Alternative Risk Premia

A challenging period for factor investing has left investors scrutinising the performance of Alternative Risk Premia strategies.

The Diversification Debate and ARP Results

The Diversification Debate and ARP Results

The see-sawing stock markets of 2018-19 provide an interesting window in which to examine the performance of “diversifying strategies.”

Hedge Funds Plus Risk Premia: Fantastic Fusion or Baffling Blend?

Hedge Funds Plus Risk Premia: Fantastic Fusion or Baffling Blend?

A growing number of investors are now blending Alternative Risk Premia (ARP) and Hedge Funds in one portfolio, or even in one mandate. Yet just how coherent are these combinations?

Are Alternative Risk Premia Strategies Proving their Worth?

Are Alternative Risk Premia Strategies Proving their Worth?

This year has been something of a rollercoaster for traditional markets, particularly equities, following a period of sustained low volatility and positive returns.

On the Hunt for Liquid Alternatives

On the Hunt for Liquid Alternatives

Diversification is a very personal property. The definition of a good diversifier varies with each investor’s existing exposures, liquidity profile and risk tolerance, as well as the market environment.

How Have Alternative Risk Premia Strategies Performed?

How Have Alternative Risk Premia Strategies Performed?

There is now a critical mass of ARP managers with live track records near or above the three-year mark. And their performance is illuminating… Have ARP strategies been delivering on their promise of strong risk-adjusted returns with low correlation to traditional asset classes?

The Changing World of Alternative Beta

The Changing World of Alternative Beta

When implementing an allocation in the rapidly-growing ARP (“alternative beta” sector, a great deal can fall through the cracks between theory and practice.