English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada) - European institutional investor

- 2015 to present

- Portfolio Solutions

- TBC

- TBC

- TBC

- TBC

- Portfolio risk reporting

Our specialist says:

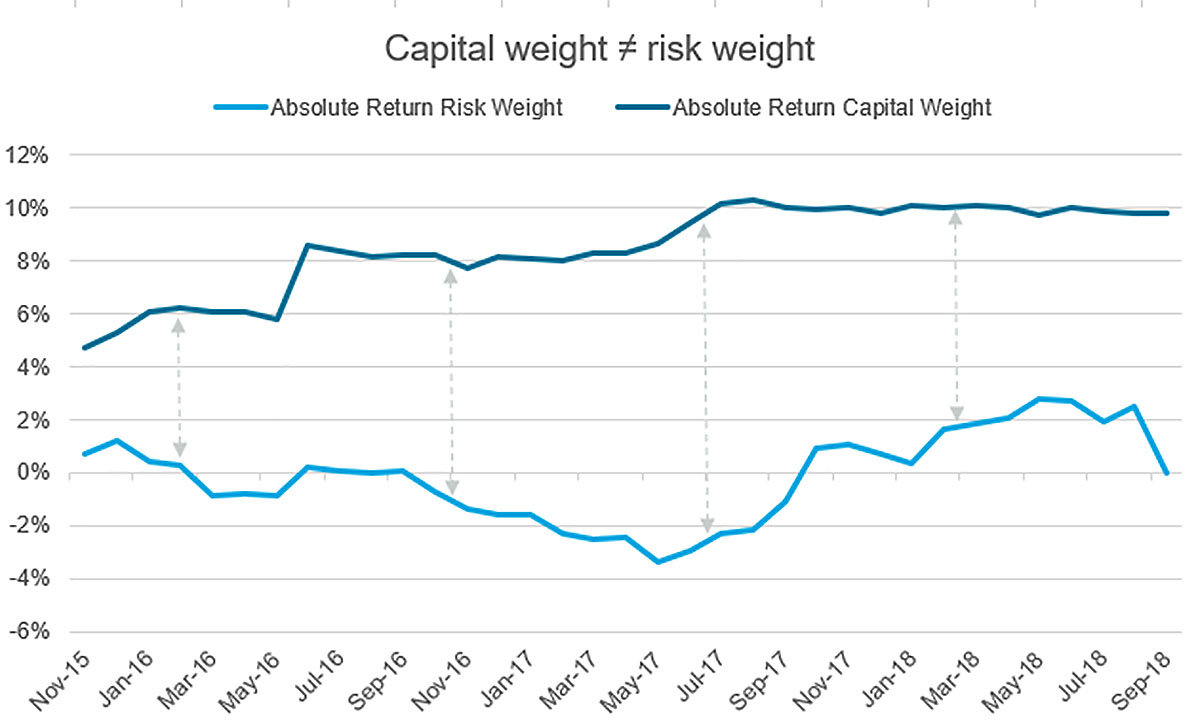

We regularly assess how new managers or changes to the client’s asset allocation might change the portfolio’s risk profile and distribution. As we see in this case study, capital weights often misrepresent where portfolio risk is generated. It is not always clear from the start which elements of the portfolio contribute to risk in which way.

Engagement at a glance

The client engaged bfinance Risk Solutions to provide holistic portfolio risk reporting, following the selection of a group of alternative absolute return managers that were intended to improve portfolio diversification. The investor wished to monitor the risk characteristics of the absolute return strategies in context of the broader portfolio, being conscious that diversification cannot be measured in isolation.

Client-Specific Concerns

The in-house team did not have the spare capacity and ready expertise to monitor both the risk exposures of absolute return managers and the overall portfolio risk exposures on a regular basis.

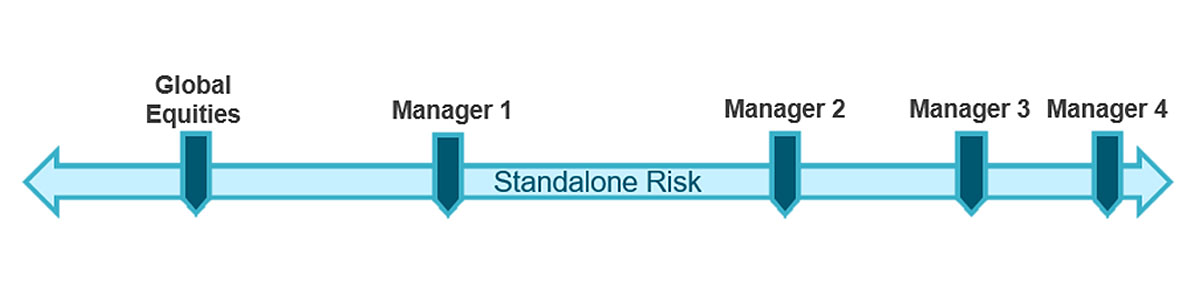

The relevant absolute return strategies have an aggregate 10% capital weight in the portfolio and include multi asset Trend and Macro managers. On a standalone basis, each manager can be characterised from relatively risky to risky.

Outcome

- bfinance provided detailed benchmarking of performance and fees paid to 14 external managers across 7 asset classes: European Equity, US Equity, Emerging Market Equity, Euro Credit, Euro Asset Backed Securities, Emerging Market Debt and US Loans.

- On a monthly basis, bfinance provides a tailored risk report that evaluates total portfolio risk and how this risk is generated via the portfolio’s components. All investments are considered, from global equity managers to commodities and credit managers. Using this analysis, the client can assess the risk properties of the absolute return managers in context of the wider portfolio.

- Despite being risky investments on a standalone basis, the absolute return portfolio has a portfolio risk weight of 0% versus a capital weight of 10%, offering alpha without increasing risk.

- From September 2016 to October 2017 the absolute return portfolio had a negative risk weight: the absolute return managers actively reduced total portfolio risk.

- We expect increased diversification benefits from these strategies in a higher volatility investment environment.