Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada) - Italian Family Office

- 2023

- Multi-asset, global

- EUR 600 million

- Develop a strategic asset allocation

- Strategic Asset Allocation

Our specialist says:

We see engaged investors keen to become more actively involved in the modelling process and seeking suitable customisation, instead of merely adopting a consultant's model. Some investors are expressing the desire to use their own economic forecasts while others are interested in delving deeper into the modelling of asset classes and integrating their own beliefs into the process. Being able to support clients in formulating their own CMAs is something that bfinance happily supports.

Client-Specific Concerns

In early 2023, an Italian family office engaged with bfinance to create a Strategic Asset Allocation (SAA) for its new asset portfolio. The investable universe included a broad spectrum of public and private markets, ranging from global government bonds to non-performing loans, and including strategies investing in European and the US assets. The project’s primary goal was to support the client in devising an optimal portfolio allocation that aligns with the portfolio’s investment objectives and constraints, specifically aiming for an 8% annualised return, or a 500 spread over long-term expected inflation.

Outcome

- Offering forward-looking capital markets assumptions: The investor expressed a desire to incorporate their views into the capital market assumptions generation process. This included specific macroeconomic forecasts alongside returns adjustments derived from in-house discussions. bfinance specialists provided their base set of capital market assumptions and refined those based on the client’s requirements.

- Providing frontier analysis to support decision-making: By utilizing capital market assumptions, bfinance supported the investor by conducting optimisation analysis. The focus was initially on uncovering any fundamental biases in the capital market assumptions, which can be uncovered by running unconstrained optimisations. Once the assumptions were calibrated, the optimisation provides a range of theoretically optimal portfolios: those were used to define an optimal SAA and determine suitable minimum and maximum ranges for the strategic allocations. The investor took a particular interest overweighting private markets.

- Conducting stress tests on a forward-looking and historical basis: Specific stress scenarios provided by the client were modelled and their impact on the optimal portfolios was assessed: a housing market crash, gas rationing, inflation expectations and supply chain disruption. Each scenario was associated with predicted macroeconomic outcomes which allowed for their explicit modelling.

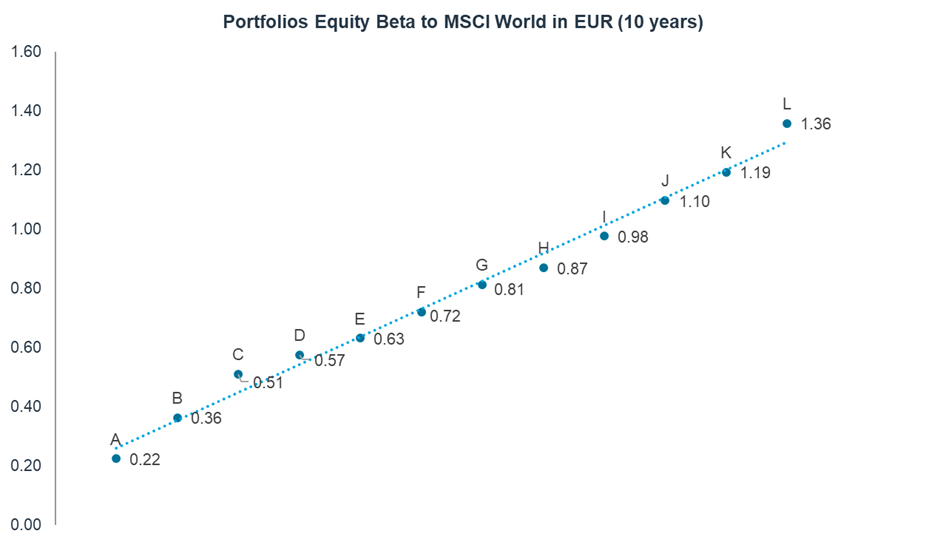

Portfolios A to L have been generated following the optimization process. For a higher risk return profile, optimal asset allocations move towards greater exposure to equity and private markets, as highlighted by the increasing equity beta on the chart.