Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada) - UK Government Pension Fund

- Q1 2022

- Real Estate (Social Impact), UK/Europe

- GBP 45 million

- Direct pooled fund

- 5%–7% net return p.a. (possibly higher risk/return)

- ESG Advisory, Manager research

Our specialist says:

With the surge in investor appetite for socially responsible real estate investments, the number of available strategies has expanded considerably in recent years. Domestic and international investors are attracted to the long-term and inflation-linked cash flow metrics of these offerings, as well as their strong supply/demand dynamics and positive ESG profiles. However, understanding the long-term sustainability objectives—the what—and the processes in place to achieve them—the how—is critical to ensuring that private capital meets social investment in a meaningful and productive way. Generating attractive returns is very possible in this sector, but investors need to scrutinise managers’ actions and make sure they can demonstrate a clear path towards the realisation of positive social and financial impacts.

- 106Considered

- 30Long List

- 12Shortlisted

- 5Finalists

- 1Selected

Client-Specific Concerns

This investor, a local government pension fund, was looking to invest GBP 45 million in Private Market strategies with high social impact—a new, dedicated impact allocation separate from its broader portfolio.

During initial client discussions, it became evident that private equity and private debt were unlikely to be appropriate asset classes, due in part to the client’s return objective (5%–7% net return per annum). As a result, the client decided to narrow the focus of its search to socially impactful Real Estate strategies.

This was the investor’s first foray into ‘Impact Real Estate’ and its team wanted to identify a strategy that would create a meaningful social result—without compromising any future return—using leverage of less than 30%. The client also wanted to limit development risk, a key element of many impact real estate strategies, to less than 20% of the portfolio. Additionally, forward funding or a forward purchase agreement, while expected and desirable from an impact perspective, had to carry adequate risk mitigation.

Beyond these metrics, the client wanted to identify a manager that could bring a strong social and environmental ethos to the effort, including credible, firm-wide policies and processes. In addition, the client wanted to see a strong, proven approach to impact reporting even though many managers in the sector are relatively new and still in the process of aligning their reporting with current best practice.

Outcome

- Training on impact in private markets: bfinance’s ESG and Private Markets specialists provided dedicated and extensive client education on impact investment given that this was a first-time allocation to a rapidly evolving set of illiquid strategies. This approach provided clarity on the available opportunities and laid the foundation for the assessment of managers’ approaches.

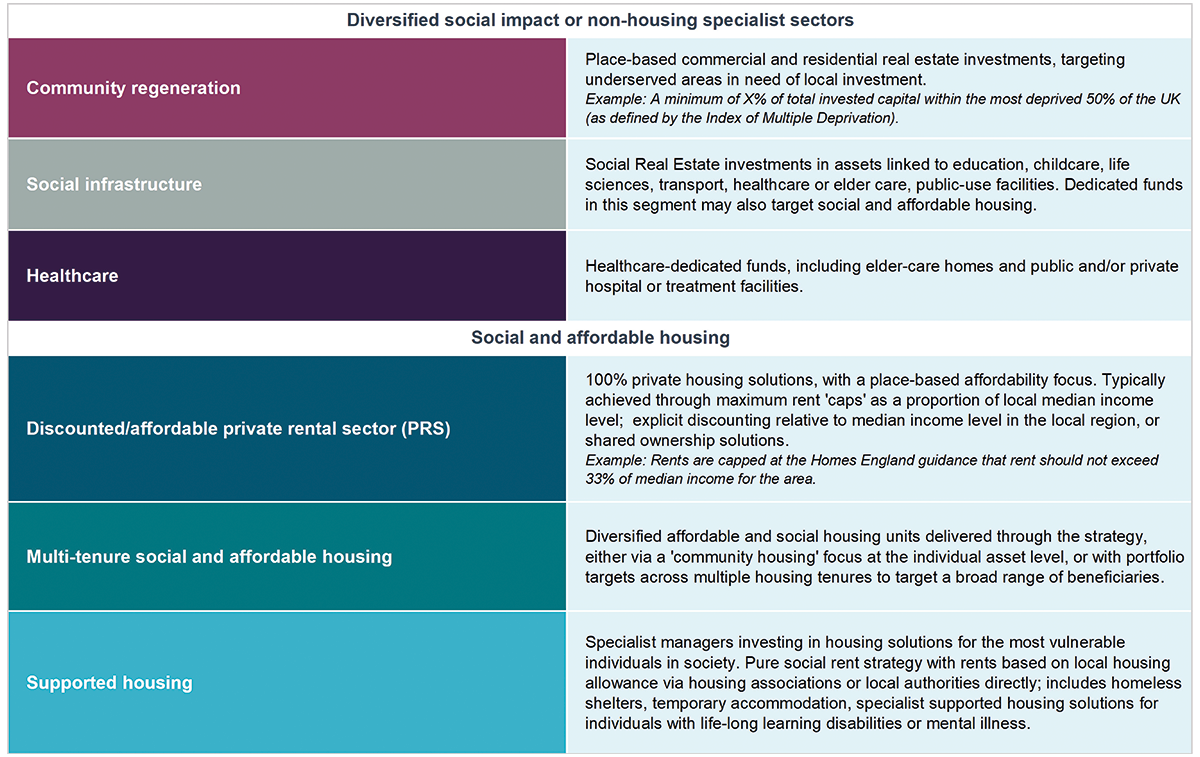

- Providing insight on different strategy types: by conducting a comprehensive manager search, bfinance identified rapidly evolving strategies oriented towards social impact in the residential and commercial sectors—and uncovered managers willing to accept seed funding to establish new vehicles focused on this impact segment. More than 30 real estate strategies targeting measurable social impact now exist in the UK, including UK-focused vehicles and diversified European funds. These can be sub-categorised into seven distinct sub-sectors: four for housing (affordable private/discounted private rental, discounted multi-tenure housing, supported housing (including homelessness or specialist supported) and three non-housing segments (social infrastructure, healthcare and community regeneration).

- Evaluating impact and ESG approaches: the bfinance team conducted in-depth analysis of managers’ approaches to social impact and ESG, including a clear focus on potential ‘additionality’, i.e. would the specified impact only occur with this investment? This analysis looked at principles, investment processes and wider company practices. Many UK managers are using the Impact Management Project framework developed by industry participants for clear performance indicators and seeking sign-off on their models from entities such as British impact advisory firm The Good Economy. Not all managers have yet obtained that type of external impact assessment, however, and social impact audit histories are still limited to a handful of first movers in their respective disciplines.

- Putting clients' priorities first: this particular investor valued social impact above environmental objectives, so bfinance ranked product offerings across a spectrum of impact opportunities. In the category of community regeneration, for example, we saw some managers focusing on environmental concerns, but their strategies lacked clear social targets that would drive additionality (these strategies were deemed unsuitable). The client wanted managers to go beyond metrics such as ‘increasing employment in the local area’ and address urgent societal needs, such as the lack of housing for vulnerable people. Investor sentiment on these topics varies; we find that more politically conservative councils (and their pension funds) are more receptive to shared ownership as an ‘Impact’ sector when compared to more liberal councils. One key question: were managers meeting or exceeding the minimum? In areas such as shared ownership and affordable private strategies, for example, bfinance examined whether managers were going beyond the UK’s mandated affordable housing requirements to achieve planning permission.

- Managing development risk in a socially responsible way: Taking development risk is essential in this sector—particularly in housing—due to the lack of available supply and the importance of providing additionality. Delivering appropriate impact outcomes while also avoiding excessive exposure to development risk—such as cost excesses and timing overruns—requires a careful balance. For example, a forward-funding model, in which the manager bankrolling the construction of a building also provides interim finance to allow construction to take place, can enhance impact but may place more risk on the asset manager/investor unless steps are taken to ensure otherwise. Importantly, these steps should not include transferring development risk onto a third-party housing association or local authority.