Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada) - UK Corporate Pension Fund

- Winter 2020

- Private Markets

- TBC

- TBC

- TBC

- TBC

- TBC

Our specialist says:

When the investor entered Fund I there were fewer comparable choices this niche. The desire to re-up efficiently should not obstruct a thorough re-assessment of the manager’s capabilities versus current peers, as well as proper scrutiny of how the earlier fund has been managed.

Engagement at a glance

A leading UK corporate pension plan was contemplating an investment in a manager’s second infrastructure fund, having already invested in the first. Although the manager was offering an extremely compelling fee discount to first-close investors, the pension fund team was keen to make a considered decision and sought external support for re-underwriting the manager and its strategy.

Source:bfinance

Client-Specific Concerns

While the investor had a long-standing positive relationship with the manager, it had a number of specific concerns including: the performance of certain Fund I investments, the integrity of the projected return metrics at Year 10 when carried interest would be crystallised (Fund I was entering Year 5), the manager’s ESG capabilities throughout the lifecycle of investments, and whether the team had sufficient bandwidth to manage a second fund. More broadly, the investor was keen to understand how the strategy compared to other options available in the market, understanding that there are now many more strategies available for greenfield infrastructure investment than there had been at the time of Fund I.

Outcome

- bfinance conducted a thorough due diligence process including numerous meetings with the manager, one-on-one meetings with members of its team and reference discussions with investee company executives as well as other investors.

- Estimated valuations in 2026, when Fund I’s carried interest would begin to crystallise, proved to be a key area of focus. Detailed asset level analysis (including the introduction of sensitivity cases) was undertaken to understand the key levers driving value over coming years and evaluating how key assumptions made by the manager compare to similar investments made by other managers that have been assessed by bfinance.

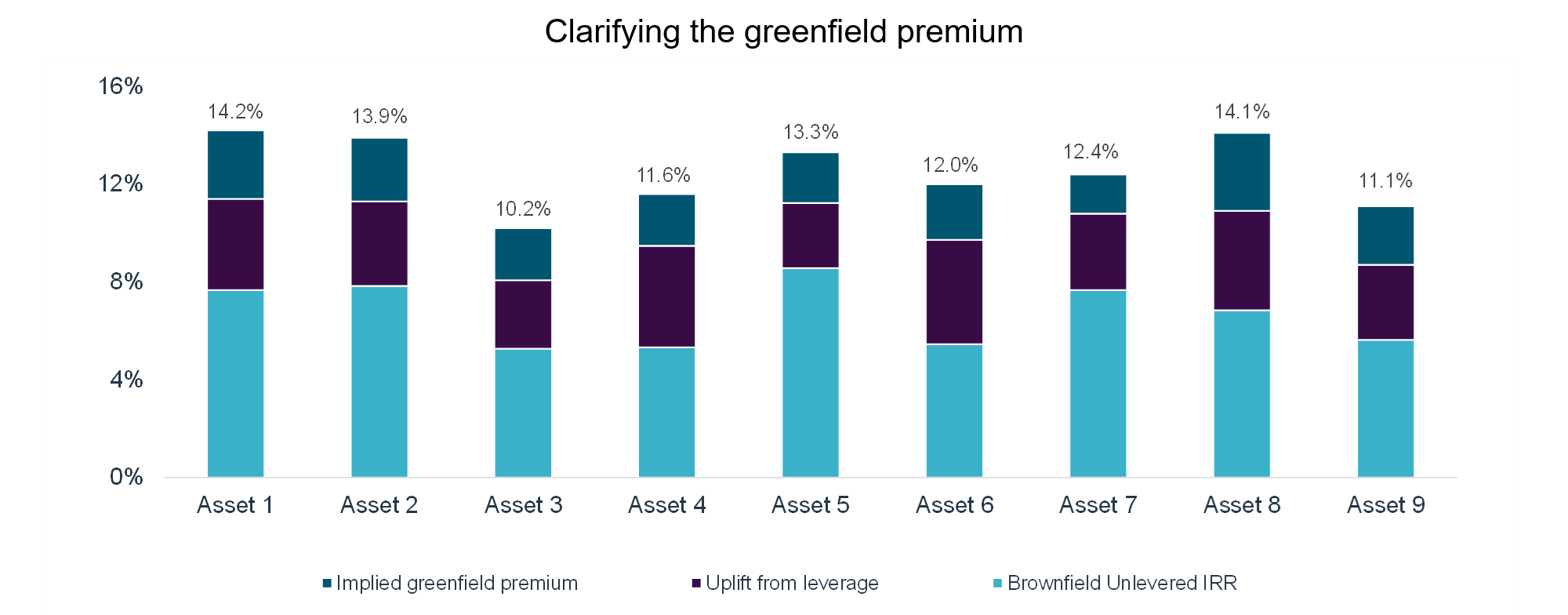

- The manager had undertaken many investments at the development stage of the asset that were originally unlevered. As such, bfinance also sought to clarify the impact of introducing leverage on returns for each of these investments post-construction. This enabled clarity around the “greenfield premium” generated by the manager, supporting the investor’s commitment to this sector.

- Deep analysis was performed on two investments in Fund I that encountered challenges during the construction process. By having access to multiple stakeholders at these projects bfinance was able to form a view on the manager’s role and where it could have done better. It was clear from the analysis that the manager was now well-placed to handle such situations should they arise on Fund II.