Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada) - Canadian Pension Plan

- 2023

- Global Impact Equity

- USD 20 million

- Manager research

Our specialist says:

Impact equity portfolios often have very differentiated holdings, with high active share and tracking error. For this mandate, the challenge was to identify strategies that were mindful of relative risk and positioning so that it could become a 'core' holding for the investor without diluting the impact credentials.

Engagement at a glance

The investor was looking to upgrade their sustainable ESG offering to a stronger impact proposition which could demonstrate positive impact contributions across multiple sustainable development goals, measurable additionality, strong stewardship, and detailed reporting on impact and engagement activities. Critically, strategies had to go beyond 'ESG integrated' or 'sustainable' and deliver on a dual objective of positive non-financial impact plus alpha.

A track record of at least three years was preferred to balance inclusion of newer offerings in the still developing listed equity impact manager universe with evidence of successful strategy execution.

Client-specific concerns and Outcome

- Participating managers: Despite the unusual ‘core’ approach to impact, and minimum requirements of track record length and structure (a pooled fund vehicle was required), participation from this growing manager universe was strong with 30 offers received.

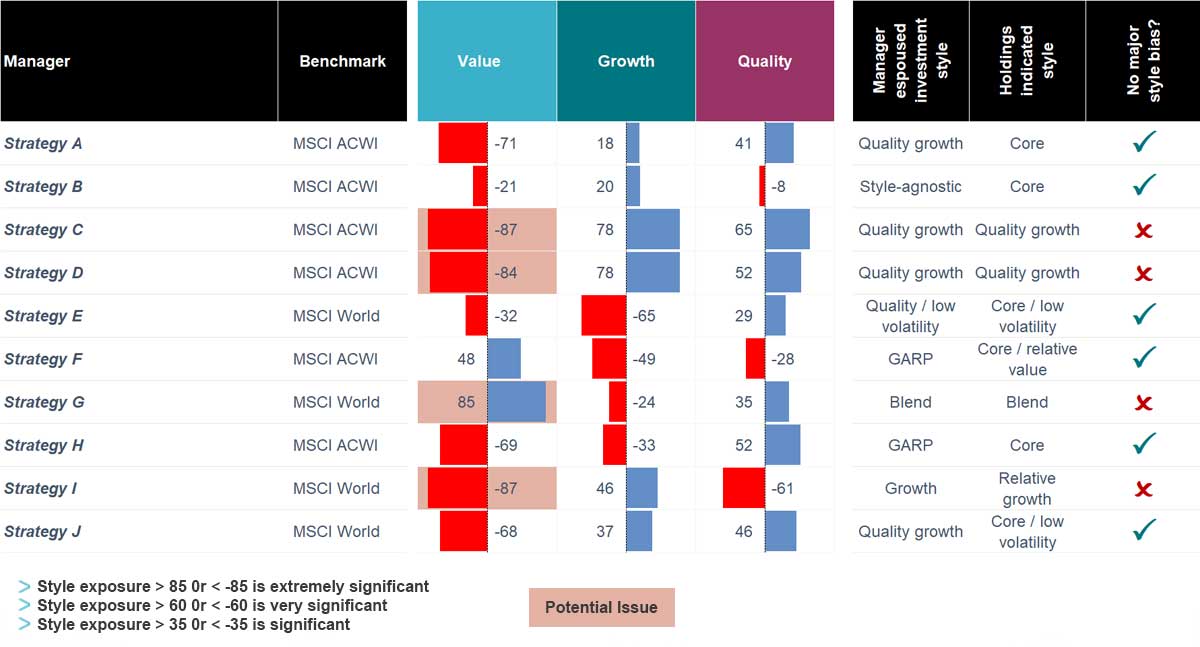

- Achieving balance: Many impact propositions are highly differentiated, seeking 'enablers' and innovative businesses which are not widely held in traditional active, core global equity portfolios or large index names. There is also a bias in the impact universe to various growth styles. In this case, the investor was seeking an impact strategy without a strong style bias that could be used as a primary exposure to equities. bfinance mapped style biases and track record volatility over time and evaluated the nature of impact approaches for each strategy to assess this.

- The style analysis considered both managers’ espoused investment styles and the overarching style indicated by the fundamental characteristics of their current portfolio holdings (which can often differ). This drew out proposals with strong style biases which would be less suitable for this investor, such as two quality growth approaches at a material valuation premium to the global market in the analysis extract shown above.

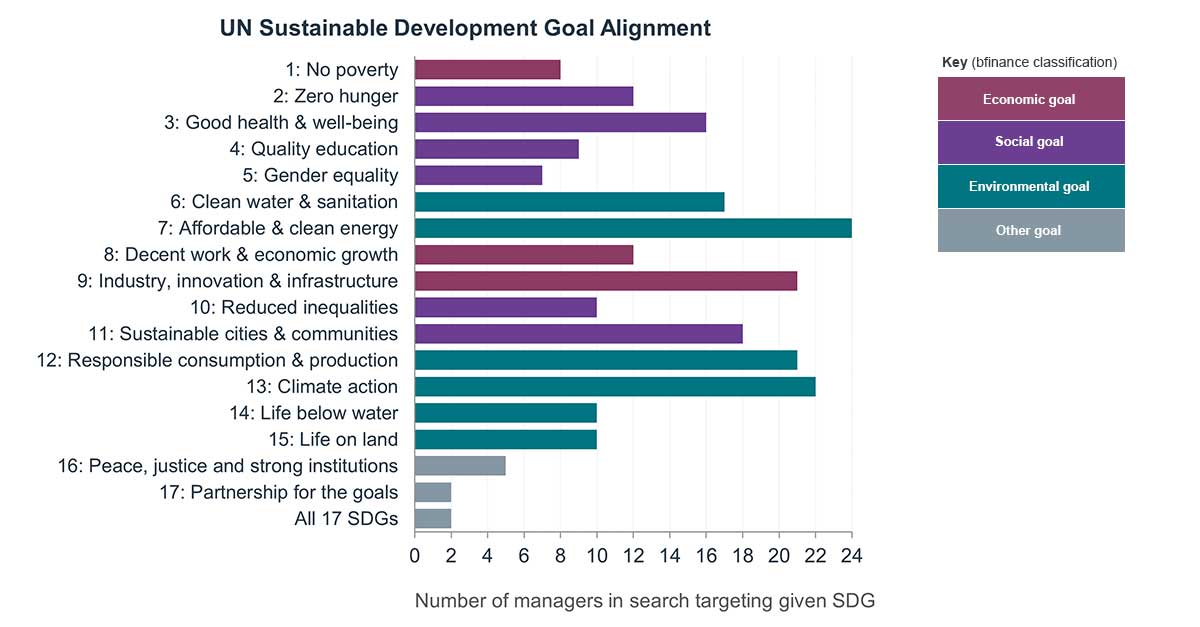

- Assessing impact types: To sift through 'impact-washing' and cut to the substance of whether strategies were true impact or just sustainable, we deepened the early-stage qualitative assessment of impact objectives, impact within the investment process, and mapping UN SDGs which managers claimed to address.

Figure 1: Landscape of search proposals by SDG alignment

Source: bfinance, based on manager provided data

Figure 2: Extract of style analysis

Source: StyleAnalytics, bfinance, based on manager provided data

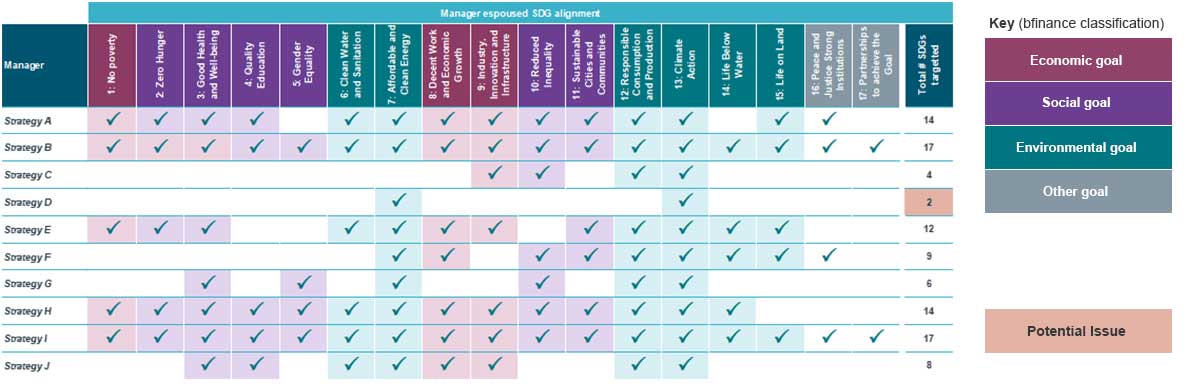

Figure 3: UN SDG alignment across strategies

Source: bfinance, based on manager provided data