English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Mathias Neidert

Managing Director, Head of Public Markets

Emerging Market Debt indices staged a significant drop in February. Active managers should have provided some protection against losses, with significant average underweight positions on Russia, but many have been hit by transaction cost headwinds and Ukraine exposure.

With Russia’s ongoing military action in Ukraine, our thoughts and sympathies are with the people suffering from these tragic events.

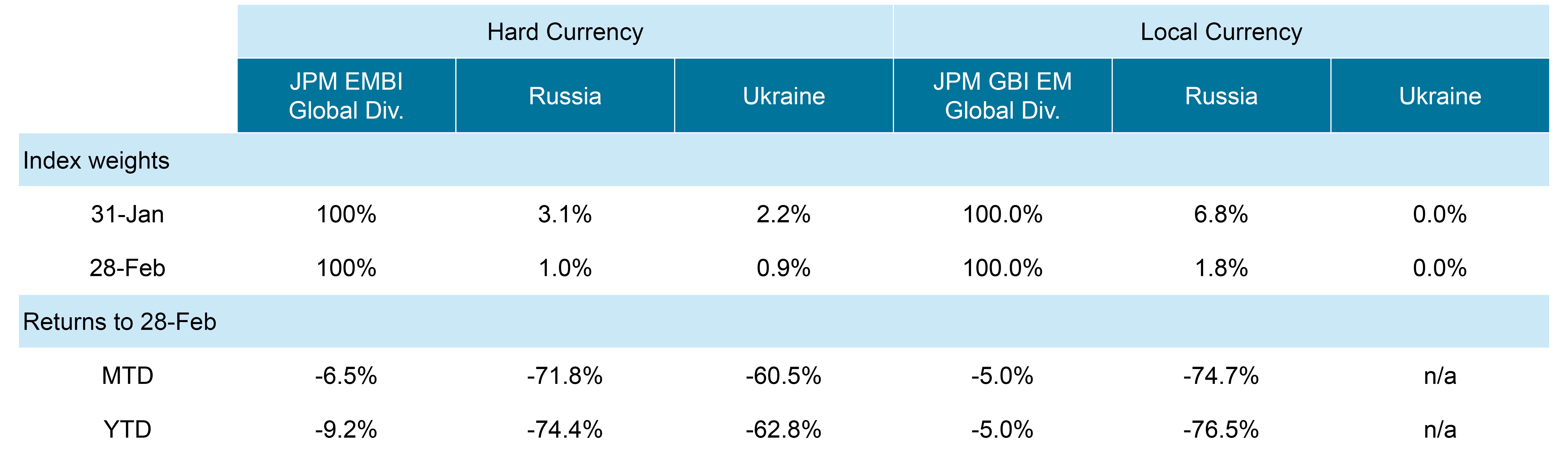

Turning to the more mundane concerns of financial markets, Emerging Market Debt investors have of course been exposed to significant financial losses. JP Morgan’s hard currency EMD index (EMBI Global Diversified) lost 6.5% in February, led by Russia—whose share of that index fell from 3.1% to 1.0% as a result of a 72% crash. Meanwhile, the Local Currency EMD index (GBI EM Global Diversified) lost 5% in February, with Russia’s share falling from 6.8% to 1.8%. Ukraine’s bonds also suffered severe losses; the country represented 2.2% of the Hard Currency Index before the invasion but does not feature in the Local Currency index.

Source: JP Morgan

While Russian sovereign debt remains part of these indices for now, it is far from being sufficiently liquid. Although the full details of sanctions and bans are still unclear, restrictions on transactions and the exclusion from SWIFT make it far more difficult—if not completely impossible—to trade Russian sovereign bonds. JP Morgan has already announced that new debt issued by sanctioned Russian entities will not be included in its indices going forwards, although the existing bonds remained as of March 1st. As for Russian hard currency corporate bonds, trading continues—albeit at large discounts and wider spreads.

Broader EM Impact

The impact of the crisis on EMD performance has so far been confined to the region. Overall, the figures are not extreme: while the spread of the JP Morgan EMBI Global Diversified index widened by 87bps in February to 472bps, this figure is far from the level reached during the COVID-related upheaval of March 2020 (721bps).

Indeed, there might be silver linings in store for EMD investors. The conflict is set to drive further commodity inflation--starting with oil and gas—which will boost the many commodity-exporting countries in Latin America, the Middle East and Africa. Should Russia be cut off from the global supply chain, those countries would benefit still further. Meanwhile, inflation will impact spreads, real yields and currencies in other EM countries.

Scrutinising manager performance

While investors with EMD exposure have broadly suffered, active managers should have been well placed to outperform against benchmarks. At the end of 2021, we estimate that 69% of Blended EMD fund managers—those able to use both Hard Currency and Local Currency bonds—were underweight Russia (versus a 50% EMBI/50% GBI EM benchmark, which had Russia’s weight at 5.3%). The average position was 1.5% less than the benchmark; more than one in four funds had less than half of the benchmark level of exposure. This latter group included a number of ESG-focused strategies—some of which had a strict exclusionary approach to Russian sovereign debt.

However, it’s interesting to note that many of these managers were offsetting light Russia exposure with stronger exposure to CEE countries at the end of 2021, creating an overall neutral stance to the region. This is particularly evident in cases where ESG has been a leading motivation for the underweight position. Indeed, if we look at the combined basket of countries that have been most directly affected by the crisis so far—Russia, Ukraine and Belarus—only 41% of managers were underweight versus a 50:50 composite benchmark (6.6%).

While we did see many managers reducing those positions ahead of the most severe days of correction—which should have supported outperformance—they did so in a climate of widening bid-ask spreads; depressed bid prices will have created a severe transaction cost headwind which may not be reflected in the index numbers.

Side pockets would be beneficial to new investors, who would be shielded from any future impairments

When looking at performance, it will also be important to remember the fund’s valuation approach. Some price holdings at bid, others at mid; the latter may appear to have superior performance when bid-ask spreads widen (and the opposite when they contract), even if the holdings are identical. This same technicality can also favour the Local Currency index (the GBI-EM is priced at mid) versus the Hard Currency index (EMBI, priced at bid). The bottom line: in any environment where a market (or part of it) becomes illiquid—no or few trades, no or few quotes—it becomes harder to compare the performance of funds to the benchmark or to each other.

Investors that are selecting Emerging Market Debt managers at the moment must pay careful attention to any outstanding exposures. Fund managers will find it increasingly difficult to offload any remaining Russia positions in the portfolio: these bonds can be considered in default with low probability of recovery, rendering the debt effectively worthless. Managers may need to decide whether to write off the debt or side-pocket it in the hope of a long-term recovery. Side pockets would be beneficial to new investors, who would be shielded from any future impairment. Ukraine debt, meanwhile, is still theoretically tradeable and being serviced, meaning that outstanding positions here are a little less concerning. Should Russia succeed in toppling Ukraine’s government, however, Ukrainian sovereign debt would likely come under similar restrictions to its Russian counterpart.

An uncertain picture

The road ahead depends on the evolution of the situation on the ground, where Ukraine’s forces have already surprised onlookers with the strength of their resistance. The future will also be defined by the shape and extent of the sanctions applied against Russia and Russian entities; the various restrictions and bans are evolving rapidly, with new details and decisions continually emerging from the US, Europe and others. Meanwhile, the wider geopolitical consequences are of course still unknown—and may be extreme indeed.

Asset managers should continue to provide more-frequent-than-usual communication with investors through this troubled period and offer the maximum level of transparency on potential exposures and portfolio impact.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.