English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

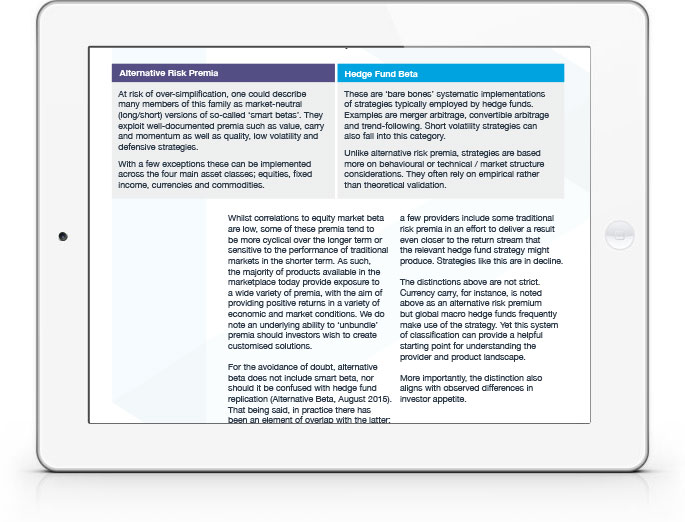

What alternative beta is…and what it isn’t: Defining and categorising the alternative risk premia universe, we note a helpful distinction between more academically established “alternative risk premia” (value, carry, momentum etc) and “hedge fund betas” (systematic implementations of merger arbitrage, convertible arbitrage, trend following etc).

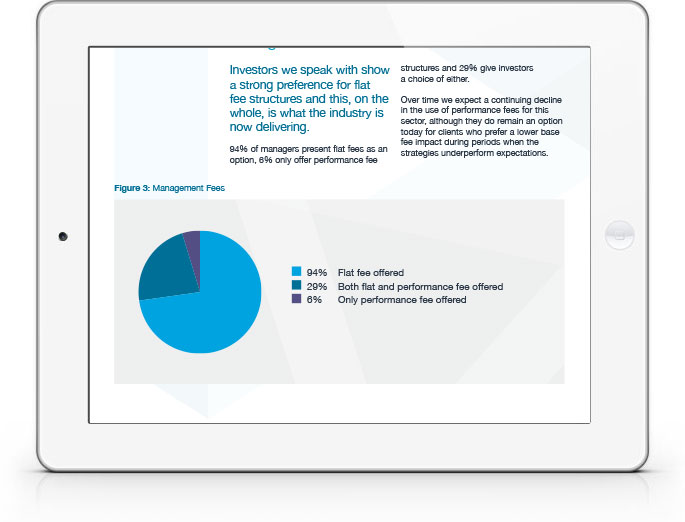

Products and providers: Approximately 40 firms now offer a relevant institutional-quality Alternative Risk Premia product. In terms of key characteristics, is conceptually convenient to split the universe into broad-spectrum asset managers (two thirds) and hedge fund managers (one third). The paper also includes data on current fee levels and structures.

Implementation variation:Looking under the bonnet reveals very significant implementation differences and portfolio construction differences. There is low correlation between managers targeting nominally similar risk premia. Pairwise correlation averages just 0.37 (maximum 0.74).

WHY DOWNLOAD?

The alternative beta product universe has evolved rapidly as asset managers push to take advantage of rising appetite from asset owners.

During the past nine months alone, the number of institutional-quality firms offering an established strategy has increased by more than 30%, based on bfinance data. Some “early-bird” pricing has been phased out, although substantial discounts are available for investors prepared to fund newer products. There has been some refinement of product type with a decline in the development of strategies which blend more ‘traditional’ risk premia into the mix.

Amid these changes, the sector continues to be remarkably heterogeneous, unlike its increasingly commoditised ‘smart beta’ cousin. This diversity is not purely the result of obvious variations in the types of risk premia being targeted by individual firms. It also arises from significant practical differences in their methods of implementation and portfolio construction.

Many of these strategies are rather challenging to execute profitably, despite their relative conceptual simplicity, and the firms involved - ranging from hedge funds to broad-spectrum global asset managers - bring different infrastructure and expertise to the table. Even nominally similar managers exhibit relatively low correlation with each other when compared with managers in other systematic strategies such as CTAs.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.