English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Anish Butani

Senior Director, Private Markets

Investors have appeared satisfied, so far, with the resilience shown by their infrastructure portfolios through the turmoil of 2022. The combination of inflation sensitivity, low real interest rates and robust buyer appetite have supported a sense of continued momentum in the sector. Yet mounting concerns are prompting a re-evaluation of exposures and expectations. What should investors watch out for in the current climate?

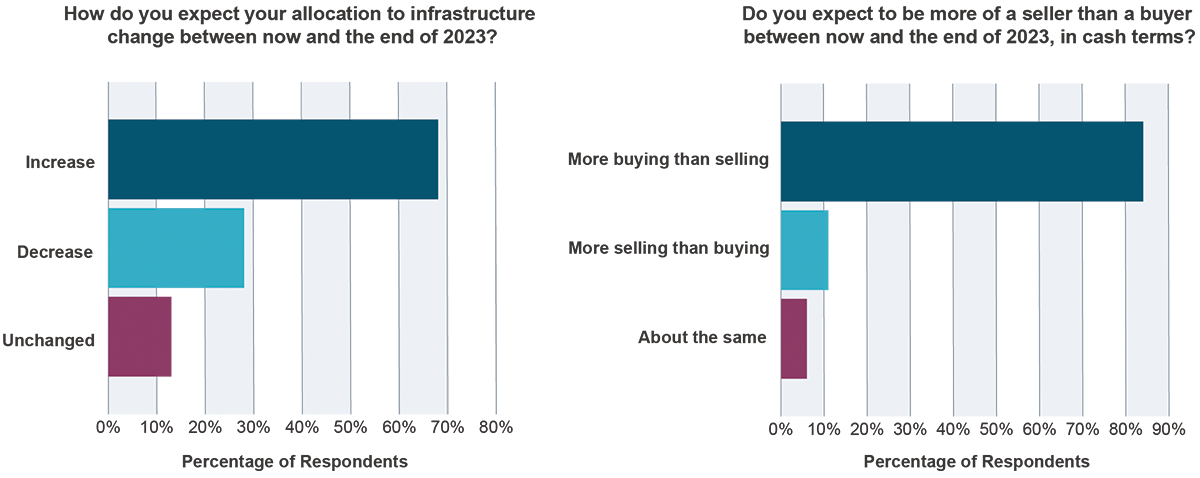

Only a few weeks ago, in September 2022, I had the privilege of chairing the PEI Infrastructure Investor Forum in London. The mood among the industry professionals in attendance was benign, if not positively bullish. One asset manager panelist asserted that infrastructure “has defied gravity,” appearing to capture the tone of the room. Indeed, our own data on core/core-plus open-ended infrastructure strategies shows gross returns averaging 5.6% in the first half of 2022, with apparently robust yields. Nearly 70% of the investors attending this event were expecting their allocations to infrastructure to rise between now and the end of 2023.

Equity risk overlays have yielded significant benefits for many investors over the past couple of years. It is, however, far from straightforward to implement a strategic approach in this area that works over the long term. Those that take on the burden of funding tail protection strategies without thorough long-term commitment at all levels of the governance structure may find themselves suffering the same fate as CalPERS, whose team abandoned its protection measures just before the Covid crisis—and lost out on well over a billion dollars in returns as a result.

Endorsing this positive expectation, the 2022 bfinance Asset Owner Survey—also conducted in September and due to be published in a few days' time—highlighted infrastructure as the asset class where investors are most likely to be increasing exposures over the next 18 months. More than 40% of investors around the globe expected exposures to rise, with fewer than 5% predicting the opposite (the conference figures were higher, of course, as one might expect from a thematically-focused event).

September snapshot: allocations on the rise

Source: Investor polling, Infrastructure Investor London Forum, September 2022

Yet if “a week is a long time in politics” – a quip attributed to British Prime Minister Harold Wilson during an earlier collapse in the value of the British pound (that of 1964) – then a month is undoubtedly a long time in investment. The mood among infrastructure professionals today, at least behind closed doors, is pointing to greater tension. The sharp pivot in public markets since the end of the summer has focused minds on the profound ongoing 'regime change' and its implications.

This period will represent the first true test for infrastructure as a mature asset class: the sector has evolved dramatically over the last decade (see this ‘Infrastructure 3.0’ article from 2017). It will be a period when assumptions are tested: assumptions about the role that infrastructure plays in a portfolio, inflation protection, diversification from the broader market, liquidity, political risk and more. Blind spots and failings will undoubtedly emerge. The era of ‘easy money’—cheap financing as well as buoyant fundraising—will have hidden a number of sins. With tail risks aplenty, expect to see some notable losses, whether they are the result of bad practices or simple bad luck.

What should investors look out for in the current climate? Four issues to watch—discussed in more detail below—include:

1. Valuation revisions;

2. Higher debt servicing costs;

3. What type(s) of drawdown

4. Fundraising slowdown;

5. Areas of opportunity.

1. VALUATION REVISIONS

When it comes to valuations in the unlisted space, investors should not expect infrastructure to defy gravity forever. We have already seen substantial volatility in listed infrastructure trusts: based on a recent sampling, share prices were trading at a discount to NAV (averaging -12%) in mid-October, having peaked at a premium to NAV of 9% in August, and the discount has subsequently narrowed to around 5%. That being said, many of these listed yieldcos are London-based and affected by the volatility in UK government bond markets.

While there will be a valuation adjustment in the unlisted space, corrections should be less severe or rapid than those we are currently seeing in the real estate or the listed investment trust space. In core infrastructure, where returns should remain robust due to the contracted and regulated nature of assets, investors should interrogate how portfolios are performing relative to their discount rates (a measure of expected returns): underperformance versus stated discount rates will be more meaningful than 'absolute return' figures.

Macroeconomic factors will have a strong—but not necessarily straightforward—impact on valuations. Firstly, rising government bond yields should have a harmful effect: these impact risk-free rate assumptions that feed into overall discount rates. Yet most managers claim to have maintained a “buffer” in their calculations to account for the environment of very low risk-free rates over the last decade. Expect to find out just how prudently these “buffers” have been adopted.

Conversely, higher-than-expected inflation should theoretically have a positive effect. Inflation can support higher project-level cash flows, yields and valuations if relevant linkages and factors are in place. Investors should not, however, be complacent on this subject (see Will Your Infrastructure Investments Withstand Inflation?). Inflation will also increase the costs associated with infrastructure projects (particularly construction costs). Indeed, a world of strong USD inflation may be particularly problematic: depending on location, the revenues of assets may be exposed to weaker inflationary forces than the costs involved in building or maintaining those assets.

2. HIGHER DEBT SERVICING COSTS

Debt servicing costs can also have a profound impact on project cash flows (and valuations), given the significant amount of leverage involved in most infrastructure assets. Yet the extent of the impact will vary greatly depending on the nature of the investment and the financing arrangements used.

'Core' and 'core-plus' infrastructure assets are typically more highly levered than value-add, but also tend to involve long-term fixed-rate financing, which provides protection. Where assets do have to be refinanced in the short-term or are not financed using fixed-rate debt, refinancing assumptions will have to be updated to reflect latest market rates and less debt may potentially be obtained. Asset managers are expected to manage refinancing risk across their portfolios with care and maintain some headroom (12-18 months) before re-levering assets. As such, it would be a surprise if an entire portfolio faced a “wall of refinancing”; plenty of borrowers will continue to access debt markets as part of their normal business and, unlike the post-GFC climate, there will be a functioning credit market supplying capital.

As the era of cheap financing comes to an end, equity will have to work harder if the industry is to deliver the level of returns that investors desire.

Waters are likely to be far less calm, however, in the world of core-plus and value-add infrastructure assets that are exposed to more volume risk and revenue uncertainty—particularly those assets that are due to be harvested by mangers over the next 12-24 months as fund terms approach their expiry. Typically, vendors either look to complete a refinancing before launching the sale of equity or run a “stapled” refinancing in parallel to such a sale. A combination of higher all-in cost of debt and lower EBITDA generation will have a meaningful impact, not just on the amount of leverage that can be obtained, but also on the equity returns for investors in funds that are divesting assets over the near term. One particularly interesting space to watch will be fibre broadband, where build-out projects will be impacted by a high-inflation, higher-rate, low-growth environment. A number of infrastructure managers have made significant entries into this space, funding substantial capital expenditure using a combination of debt and equity. Whereas some markets (such as France) are supported by government concessions in rural areas, other countries (such as Germany and the UK) have encouraged competition among players to grow market share for future revenues. As debt becomes more expensive and revenues take longer to materialise, we may see the capital structures in this space coming under strain—potentially resulting in some consolidation.

As the era of cheap financing comes to an end, equity will have to work harder if the industry is to deliver the level of returns that investors desire. Managers will no longer be able to lever up assets to the extent they had done previously in order to execute deals or enhance returns. Value creation will therefore be in the spotlight. Certain types of financing arrangement—such as investment grade 'HoldCo' debt, which has emerged during the past five years—may no longer be viable.

3. FUNDRAISING SLOWDOWN

Industry participants are keeping a sharp eye on fundraising momentum. There is currently large capacity for inflows to the asset class and it remains to be seen whether investor appetite will remain stable—although investors polled by bfinance in September indicated strong sentiment in favour of increasing allocations over the next 18 months. If we look purely at so-called 'mega funds' (targeting around US$ 15 billion or more), we find three managers currently trying to raise a combined US$ 75 billion over the next six months. Those massive vehicles will no doubt be watched closely for signs of protracted fundraising, since this might be seen as symptomatic of a broader decline.

Investors should be increasingly mindful of this momentum when allocating capital and take a more cautious approach to funds that may have a harder time gathering assets, such as newer strategies. That being said, fundraising difficulties should not necessarily be seen as bad for investors. For example, it will be interesting to see whether any softness in capital raising results in positive adjustments to fund terms. The last few years have seen hurdle rates—the level of returns above which managers can charge ‘performance’ fees in addition to regular management fees—steadily falling on like-for-like strategies. This trend has been influenced by a benign fundraising climate and declining return expectations. In addition, a shift in market dynamics from seller to buyer may also support attractive purchase valuations and, as a result, a potentially attractive upcoming vintage over the next 9-12 months.

We may also see a shift in managers' willingness to run open-ended strategies strategies versus closed-ended ones. Managers have been trending towards ‘evergreen’ solutions in recent years. According to bfinance research, there were over 15 new open-ended strategies launched in 2022 alone, bringing the manager universe to more than 40 strategies, which raised over US$ 20 billion in the first half of the year alone. Yet, challenges around liquidity (in the face of a potential wave of redemptions) and NAV volatility should be watched with care.

When considering the subject of fundraising, it's worth thinking about the role of infrastructure in investors' portfolios. In some cases, buyers were drawn to this asset class as a 'fixed income replacement' with the ability to deliver income in a zero-interest rate world. This argument is somewhat less compelling in a world of higher interest rates: cash yields of 4-5% will not be the draw they once were. Yet there were other factors driving the rise in demand for infrastructure over the past decade, such as inflation protection, diversification and growth.

4. AREAS OF OPPORTUNITY

While there are concerns that short-term fiscal policy—particularly in the form of windfall taxes—may adversely impact the asset class, infrastructure remains a key area of focus for governments that are looking to boost growth. For example, the Inflation Reduction Act (IRA) that was recently passed by the US Government commits more than US$ 369 billion to subsidies and tax credits over a decade in order to encourage decarbonisation and cleaner energy. In particular, the IRA offers a 30% tax credit for US offshore wind energy projects that begin construction before 2026, with large incentives directed towards users of domestic manufacturing. In Europe, the heightened focus on energy security may lead governments to support a new wave of renewable energy technologies in order to make them investable for infrastructure funds.

Even where governments are not offering explicit support, the climate agenda will remain prominent as an area of opportunity for asset owners. Asset owners are continuing to develop their sustainability goals, with an ongoing focus on the energy transition. Decarbonisation will remain a key theme, whether that involves decarbonising existing infrastructure assets or repurposing assets for the low-carbon economy (such as transporting hydrogen via gas pipelines).

More broadly, the current fiscal pressures faced by governments may present opportunities for the private sector to help deliver social infrastructure via Public Private Partnership arrangements.

Looking globally, we are also seeing opportunities emerge from the reconfiguration of supply chains—a theme which is currently being strongly influenced by geopolitical risk considerations. Is the recent JV between Intel and Brookfield to build semiconductor chip factories in Arizona a sign of things to come?

Has the industry learned the lessons from the past?

Investors should always be extremely careful about assertions that any part of the asset management industry has learned from the mistakes of the past and is therefore well positioned for the next tidal wave. This is particularly true of an asset class that has changed so dramatically since the last true economic crisis.

Various lessons have, of course, been learned: approaches to topics such as leverage and interest rate swaps are certainly informed by previous pain. It is common to focus attention on the errors showcased by history. However, if the history of economic and market crises teaches us any lesson at all, it is that a new trip hazard will surely emerge.

Investors’ confidence in infrastructure is not, we believe, misplaced—provided they back the right manager. The asset class is well placed to ride out volatility and a variety of risks. Careful scrutiny and selectivity will be key to success.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.