English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

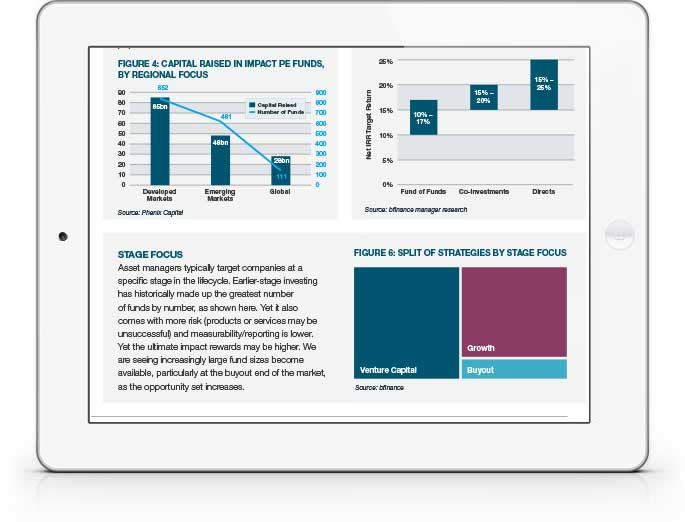

The rise of impact private equity funds: new funds are appearing on a weekly basis. Data snapshots illustrate the manager universe, categorised by fund type, geography, impact objectives, stage focus, target IRR ranges for different categories and more. We now see significant groups of buyout funds, large (>US$1 billion) funds and dedicated fund of funds – the hallmarks of an increasingly mature sector.

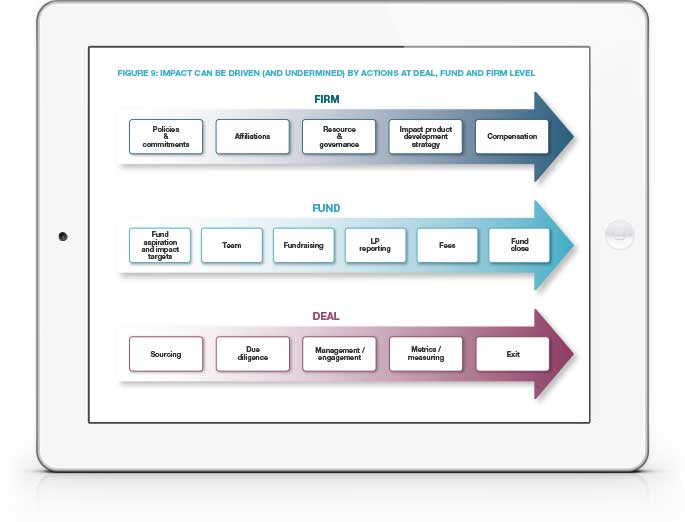

Impact at every level: managers’ approaches can be driven (and undermined) by actions at multiple levels: the deal, the fund and the firm. It is important for managers to exhibit overall consistency within and between these layers.

Leaders and laggards: manager research specialists identify ‘best practice indicators’ and ‘potential pitfalls’ across fourteen areas. None of these represents a silver bullet but, together, they can help investors to form strong-yet-pragmatic expectations. Analysis must be nuanced and sensitive to strategy and fund type.

WHY DOWNLOAD?

Private equity strategies with an explicit mission to deliver impact are a relatively new and rapidly evolving breed. They first appeared in the mid-2010s and new strategies (predominantly closed-ended) are now appearing on a weekly basis.

Amid concerns around ‘impact-washing’ it is crucial to set meaningful standards. Yet black-and-white requirements are problematic in an essentially immature asset class. Actual track records are short; KPIs are problematic; managers are often unable to demonstrate intentionality, additionality or a clear theory of change to the extent that one may wish. The investor must find a way of navigating a highly imperfect world.

In this melée, it is important to understand: what is an appropriate standard to which investors should hold ‘impact’ private equity managers accountable? What do the stronger and weaker approaches look like now? How does this vary according to the stage of capital— buyout versus venture, for example—and fund type? Fund of funds are further from the underlying assets than direct funds, for example, but have great potential to drive stronger processes and standards among GPs. Venture capital may be less able to provide existing measurement frameworks than buyout but may have great potential for long-term impact.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.