English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

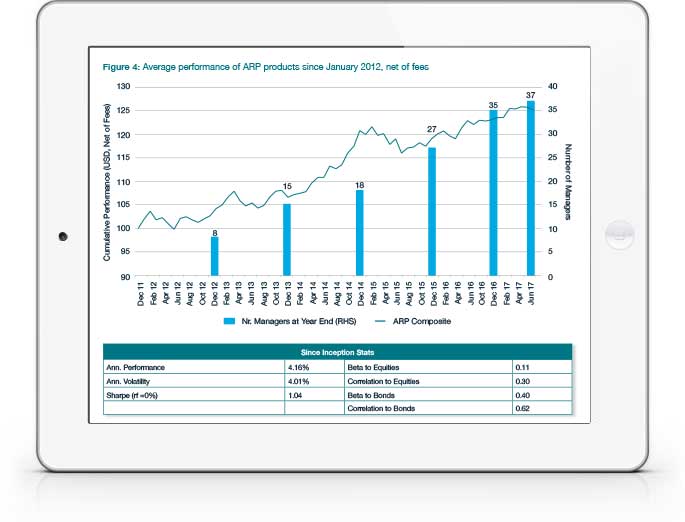

Making the grade: With a substantial body of live track records now available, have ARP strategies been delivering on their promise of strong risk-adjusted returns with low correlation to traditional asset classes? In aggregate, the answer appears to be “yes,” with an average return of 4.16% after fees, a beta to equities of 0.11 and annualised volatility of 4.01%.

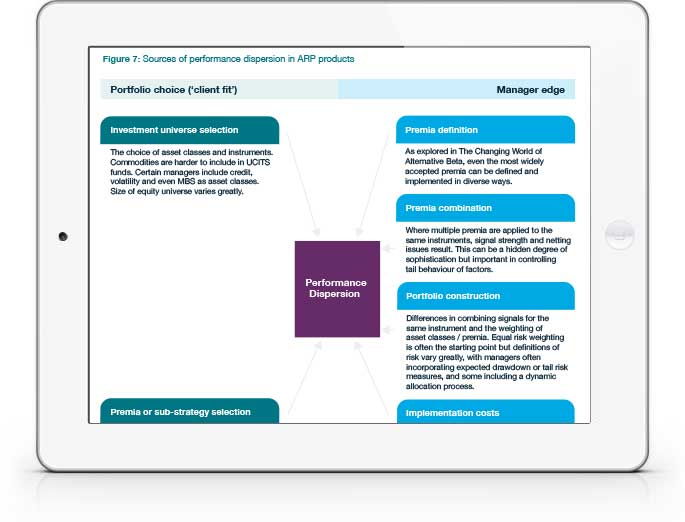

Large dispersion: However, the group exhibits very high levels of performance dispersion.

Implementation matters:Importantly, that variability appears to be greatly affected by managers’ individual implementation methodologies – not just the high-level questions of premia and asset class choice. Approaching this sector as a straightforward descendent of smart beta, or treating the selection of premia as the most important part of the decision-making process, could be a sub-optimal approach.

WHY DOWNLOAD?

The rapidly growing alternative risk premia (ARP) or “alternative beta” sector has gained significant ground as asset owners have sought effective – and cost-effective – diversification.

Despite the attractions, a lack of straightforward performance data for the sector has proven to be an obstacle for some. Investors must pick through potentially over-fitted back-tests or carveouts and attempt to make comparisons to live track records which, where available, have not been particularly extensive.

Yet, on the final point at least, matters have improved significantly since bfinance’s last ARP-focused white paper, The Changing World of Alternative Beta. We now see a critical mass of providers whose live track records are reaching or have passed the three-year mark.

This body of data does not only provide a far stronger sense of the realised performance of ARP strategies to date. It also gives a firmer basis for assessing modelled or back-tested data, which still represents a very significant component of manager analysis and selection. Finally, it may make the space more accessible to investors with minimum track record constraints.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.