English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Toby Goodworth

Managing Director, Head of Risk & Diversifying Strategies

Since the publication of Managing Currency Risk in a Two-Speed World (2017) we have seen more investors moving towards enhanced currency management, usually as an upgrade from static hedging. This article addresses three further questions. 1: how have enhanced currency overlays performed relative to static hedging, and why? 2: what is the real cost? 3: Should we hedge emerging market currencies?

The bfinance team has scrutinised the costs, capabilities and performance of dozens of currency overlay providers. Analysis reveals that enhanced currency overlay managers, as a group, have added excess returns versus static FX hedging and, more significantly, have lowered overall portfolio risk and introduced uncorrelated return streams. Yet outcomes are highly specific to an investor’s base currency, exposures, cashflow needs and more.

1: HAVE ENHANCED CURRENCY OVERLAYS BEATEN STATIC HEDGES?

Unlike asset classes such as equity and bonds, there is no wholly acceptable method for determining the past performance of a group of active currency overlay strategies.

Overlay providers’ “live track records” will not equal the performance that an investor would have received. A true starting point is not a cash position, or even a passive benchmark, but a set of continuously fluctuating foreign currency exposures that are as unique as the investor themselves. The investor’s performance is not solely dependent on the currency composition of the overlay manager but on the investor’s risk tolerance, cashflow requirements and strategy preferences. Meanwhile representative “pro forma” track records are subject to all the usual challenges which pro forma track records tend to exhibit: hindsight bias, inaccurate trading cost estimates and so forth.

The question of outperformance currency management is a deeply complex one.

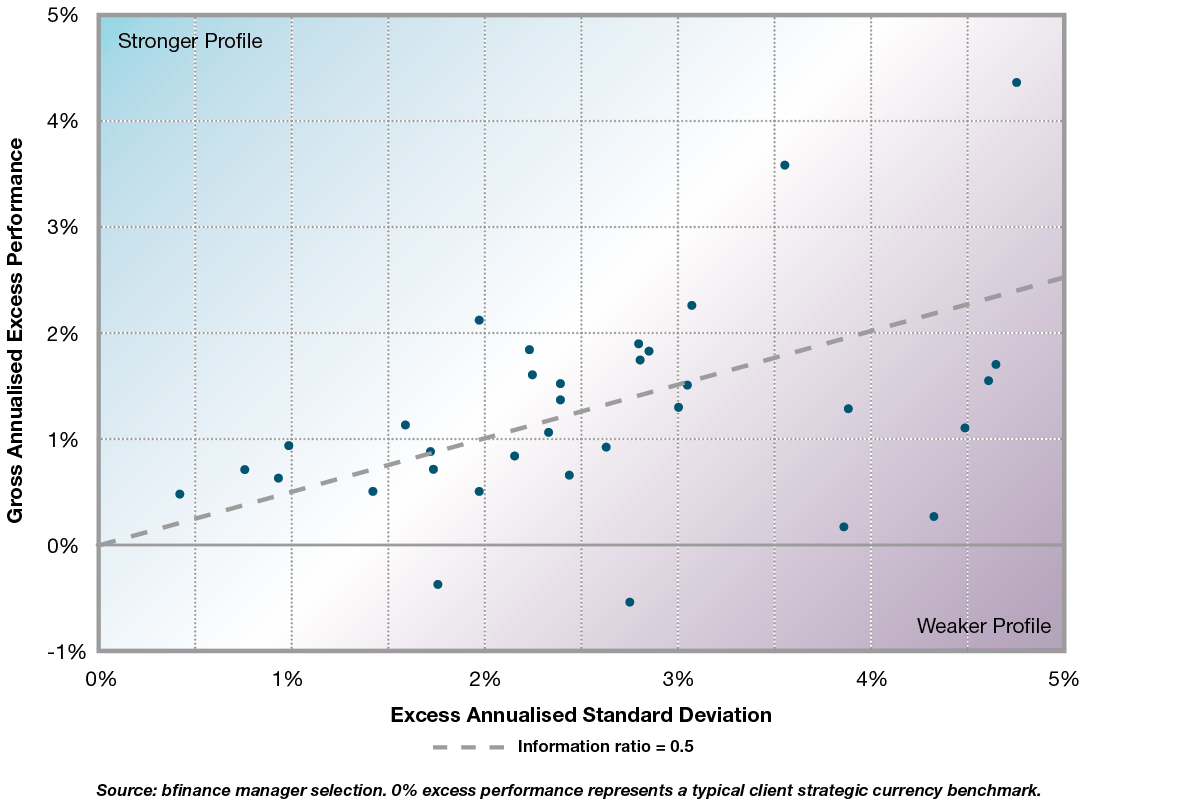

That being said, we can draw some conclusions from the data. In Figure 1, an examination of what we judge to be suitably representative five-year track records of providers vying for a mandate in 2018, 5% had underperformed a passive hedge gross of fees. (Note: the zero position was a strategic 50% hedge on developed market foreign currency exposures, since this is often seen as the position of ‘least regret’ for many asset owners.) Meanwhile, 58% had outperformed by more than 1%, while, 50% had an information ratio of 0.50 or higher (grey dotted line).

Figure 1: Manager excess risk vs. return over five years

It may be interesting to compare these results with those of currency hedge funds, whose focus is purely on absolute return generation as opposed to managing risk exposures. Over a similar five-year horizon, various sources (which do suffer from survivorship and reporting biases) indicate an average gross return of around the 5% mark, with 10% volatility. In other words, the enhanced overlay crowd has been delivering risk-adjusted returns on a par with their true active counterparts.

Looking separately at the question of diversification, we observe that excess returns generated from enhanced currency overlays (over and above that of a passive / strategic hedging program, generally show very low or meaningfully negative correlations with major asset classes (global equities and global fixed income), over both short-term and long-term horizons.

In theory, enhanced currency managers have a huge amount of scope to add value. Yet we would note that this scope is strongly influenced by the investor’s base currency. For example, the application of a simple minimum-variance dynamic hedging strategy to an Australian dollar-based portfolio of global foreign equities over the last 25 years suggests optimal hedge ratios over three- and five-year periods that range from virtually zero (2002, 2011) to almost fully hedged (>80% in 1992-3, 2007). The average ideal ratio was 47% between 1992 and 2017 but that figure has risen to 62% for the post-GFC period.

Despite the positive comments, a word of caution is warranted. When selecting FX overlay managers, we urge investors not to put too much weight on past performance. The challenges of track record analysis, coupled with the very high degree of specificity to a client’s individual portfolio and geography, make conviction on the manager’s investment process and execution capability much more important than historic data.

2: WHAT IS THE REAL COST OF ENHANCED CURRENCY OVERLAYS?

With any currency overlay program, be it enhanced or passive, there are two main expenses: management fees and transaction costs. While the former tends to attract attention in conventional asset classes, the latter often proves more significant in this sector.

Transaction Cost Analysis is absolutely critical, and frequently done poorly.

The management fees for enhanced currency overlay management do vary, with median fees at 11bps p.a. and best-quartile fees well into single digits (March 2018). This gap pales in comparison to the variations in providers’ transaction costs, where execution expenses were shown to differ by a staggering 400% - a cash drag that can surpass fee differences between cheaper and costlier providers. Transaction Cost Analysis is absolutely critical, and frequently done poorly. Through 2017-18 we have forged a partnership with New Change FX which has proved very influential in our clients’ manager selection decisions.

Investors should also keep an eye on providers’ strengths and weaknesses in trading particular currencies: managers with otherwise excellent trading capability can have serious weak spots. In one recent case, the difference between the best and worst providers in terms of their efficiency at trading in the investor’s base currency produced a figure almost equal in cost terms to the management fee itself!

More broadly, investor focus on cost efficiency and best execution, coupled with the wide variation in expenses seen above, has helped to drive a move towards specialist providers in this sector.

When considering the cost of enhanced overlays versus passive currency hedging, investors should also factor in the cost of maintaining liquidity for cashflow purposes. Lighter cashflow requirements can be one of the major attractions of enhanced overlays versus passive hedging. The latter can also generate major opportunity costs, such as forcing sub-optimal redemptions in the face of unexpectedly large negative cashflows.

3: SHOULD WE HEDGE EMERGING MARKET CURRENCIES?

While all enhanced currency overlays are expected to cover the full range of developed market currencies, EM currencies do continue to represent a line in the sand. In the most recent manager search conducted by bfinance in 2018 for an Australian client, 70% of providers proposed including EM currencies. This “yes” camp included all FX specialist managers, a significant number of diversified asset managers and some banks.

EM currencies continue to represent a line in the sand.

Across both developed and emerging markets, the manager’s decision on whether to incorporate currencies is typically determined by requirements on the minimum liquidity/depth of the market or the cost of trading. This decision should also factor in the dynamics underpinning the investor’s home currency and its relationship with EM currencies, as well as the size of the investors EM book in aggregate.

Providers that choose not to cover EM currencies often cite the prohibitive expense of trading in these markets, as well as promoting an economic expectation that EM currencies will appreciate relative to developed market currencies over the long term, and thus not hedging EM should be the preferred approach. However, in not hedging EM FX, it may leave the investor open to additional material associated volatility. As such careful consideration needs to be given to the trade-off between impact, cost and risk-return benefit. Through our conversations with asset owners globally on this matter it seems that considering EM within the context of an enhanced hedging strategy is on the cards more often than not.

Considering the case

The arguments in favour of enhanced currency overlays are not wholly founded on returns: improved cashflow management and better portfolio risk profiles are primary considerations. However, the relatively strong results generated by this group of managers provide interesting food for thought.

First and foremost, investors considering taking a more active approach to managing currency exposures must remember that these are customised solutions - not products. In each instance, the “case” and the choice of provider should be tailored to the fund’s specific needs.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.