English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

Understanding the ARP landscape: a review of risk premia, ‘academic’ versus ‘practitioner’ and ‘macro’ versus ‘micro’ factors, premia specification challenges. New data shows consolidation and contraction in the asset manager universe after a period of rapid expansion, with 47 funds now available to investors.

Towards better benchmarking: key advantages and disadvantages of different yardsticks including risk/return objectives, manager composites, bank ARP indices and ARP benchmarks. We examine a new ARP benchmark launched this month, which will help to add clarity to the sector.

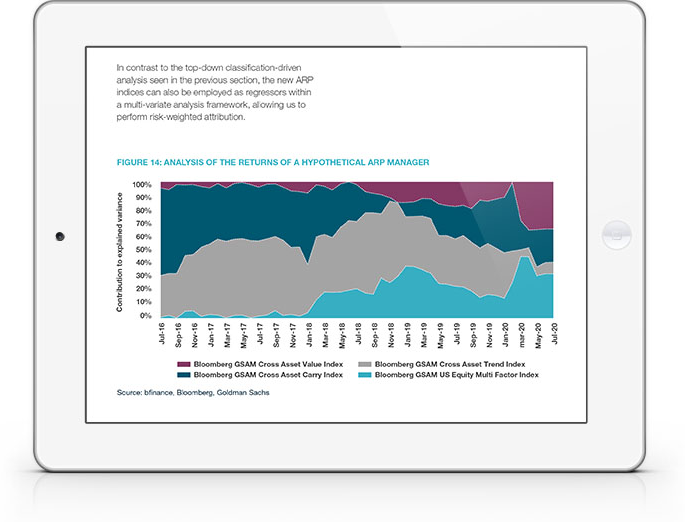

A clearer picture on performance: with new tools in mind we examine the performance of the bfinance ARP manager composite, the benchmark back-tests and the return attribution profile of a hypothetical ARP manager using the new indices as regressors.

WHY DOWNLOAD?

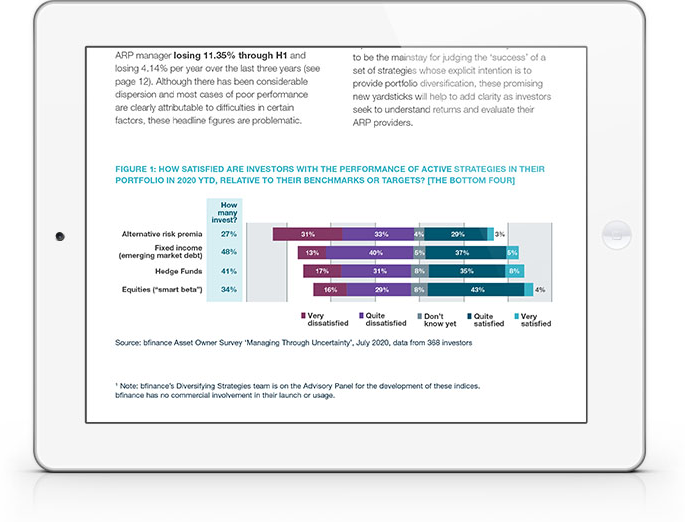

The July 2020 bfinance Asset Owner Survey indicated that, of the 27% of investors that use Alternative Risk Premia, nearly two thirds (64%) were dissatisfied with 2020 YTD performance “relative to benchmarks or targets” – the worst feedback among all sixteen asset classes assessed. The average ARP manager lost 11.35% through H1 and lost 4.14% per year over the last three years, albeit with considerable dispersion between managers.

Yet how can investors gain a robust understanding of performance? Both hedge funds and ARP struggle with this question: they are judged against absolute return objectives, supplemented by peer comparisons of varying relevance and indirectly relevant benchmarks.

With this challenge in mind, we warmly welcome the newly launched suite of ARP benchmarks from Bloomberg and Goldman Sachs Asset Management, who have kindly contributed to the development of this report. While absolute returns will likely continue to be the mainstay for judging ‘success’, these promising new yardsticks will help to add clarity as investors seek to understand returns and evaluate their ARP providers.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.