English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Pravir Sharma

Pravir Sharma

Senior Associate – Diversifying Strategies

Investors holding stakes in global macro strategy hedge funds have not enjoyed an easy ride over the past decade. Yet as inflation surges, oil prices rise, vaccine rollouts stall and the US Federal Reserve signals an early end to its bond-buying program, these strategies are receiving more attention due to their reputed ability to profit in times of pain.

Since the onset of the Covid-19 pandemic, investors have been visibly reengaging with global macro, one of the hedge fund industry’s oldest—and arguably most idiosyncratic—strategies. In the past 19 months through October 2021, global macro strategies have gradually added $139 billion in assets under management (AuM) according to industry estimates compiled by market research firm HFM, bringing the industry total to $462 billion, an increase of 43%.

It is hardly surprising that investors are searching for strategies that can dilute equity, credit and duration risk in their portfolios: after a year of rapid growth in most developed market economies, buoyed by generous government-led fiscal support packages and loose monetary policies, inflation has made a comeback. Investors are now facing the discomfiting reality that both inflation and macroeconomic volatility may rise in the near term—and prove more tenacious than most policymakers care to admit.

Yet global macro, judging by its recent track record, is by no means a straightforward answer to these challenges.

Global macro strategy: Marked resilience but weaker returns?

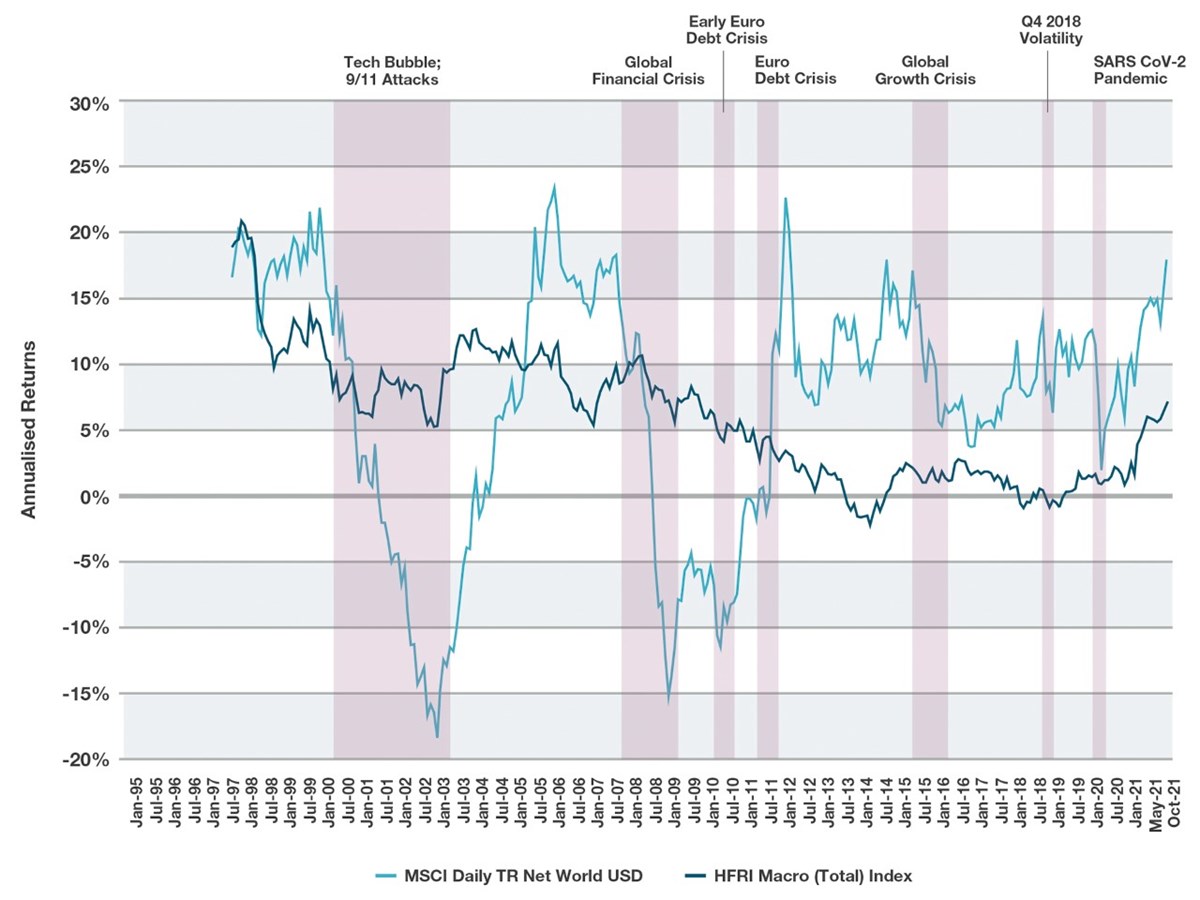

Across time, this increasingly institutionalised sector has fulfilled its promise—most visibly highlighted by the global financial crisis (GFC)—to provide resilience amid market shocks (see Figure 1). Amid various subsequent sizeable market drawdowns, the majority of macro strategies have provided meaningful portfolio protection, based on the performance of the HFRI Macro (Total) Index—which, despite its inevitable flaws, still provides the broadest industry indicator of hedge fund strategy performance.

FIGURE 1: THREE-YEAR ANNUALISED ROLLING RETURNS: EQUITIES VS. GLOBAL MACRO STRATEGIES (JANUARY 1995–OCTOBER 2021)

Source: HFRI, Bloomberg. Chart reflects one data point per month per dataset, showing the annualised rolling three-year return for each index.

On a related note, global macro strategies have also provided resilience in periods of heightened volatility. During cataclysmic periods when the monthly closing value of the VIX has exceeded 40 (eleven occurrences since 1994), the HFRI Macro Index has produced an average return of -0.4% while the MSCI World Index has delivered -6.9%. In periods when the VIX closed out the month at a level between 30–40 (18 occurrences since 1994), the HFRI Macro Index returned 0.0%, again beating the MSCI World’s decline of -2.2%.

Macro events and volatility do not always work in managers’ favour, however, as illustrated by the way in which various global macro managers have struggled to navigate recent volatility in government bonds as central bank tightening has come to dominate headlines. Yet the long-term averages are compelling. The problem presented by existing datasets, however, is that average returns have been anaemic over the past decade: according to the HFRI Macro (Total) Index, flat to low single digit returns have been the ‘norm’ since the Euro debt crisis in 2010.

Diversification without a substantial positive return can still represent a helpful addition for a portfolio, but perhaps not one that justifies hedge fund fees in the eyes of some stakeholders. Indeed, if we take a 25-year window and model the inclusion of global macro (HFRI Global Macro Index) in 60:40 portfolios of equities and bonds, we can retrospectively generate a meaningful reduction in volatility with only a slight reduction in returns. More recent time periods, however, produce less compelling modelling-based arguments.

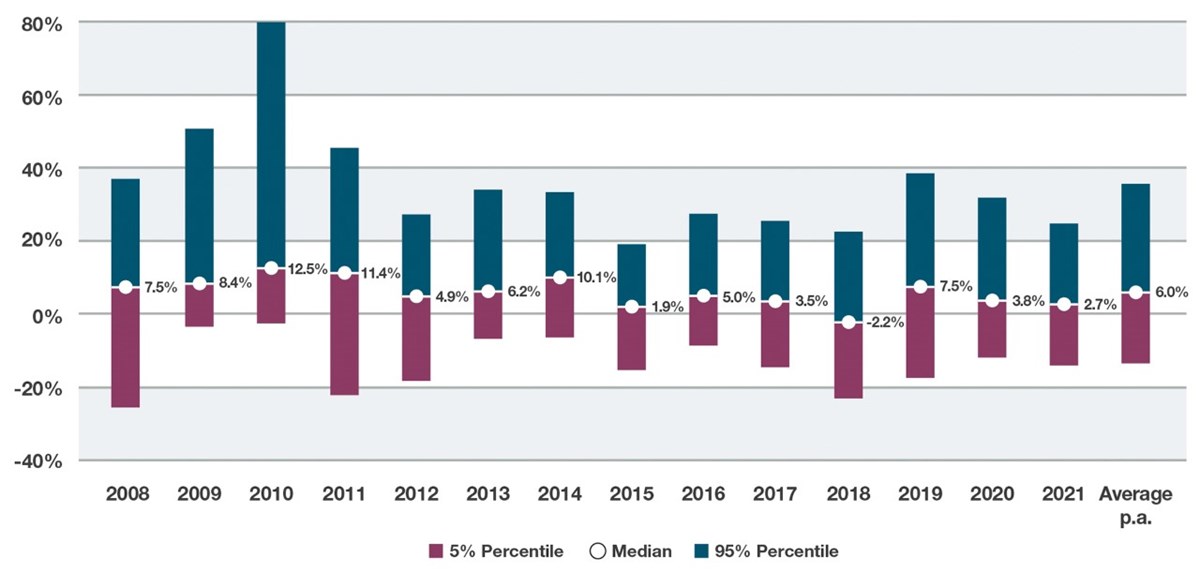

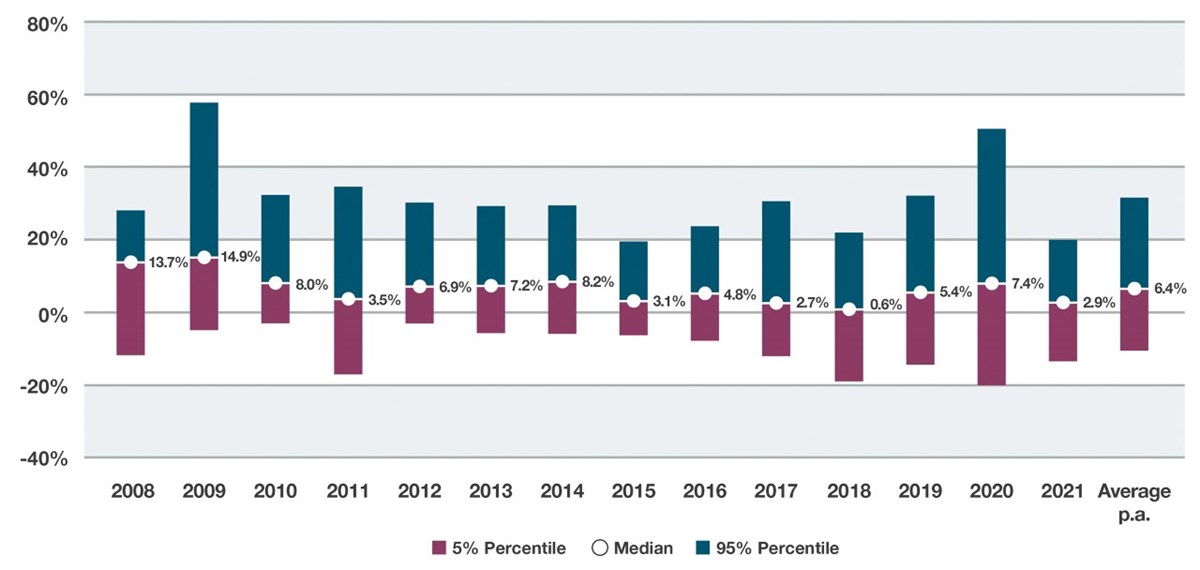

The picture does become somewhat brighter, however when examining manager-by-manager returns (Figures 2A and 2B). Here, amid the extremely wide performance dispersion that one might expect from such a heterogeneous assortment of strategies, we find that the median annual returns for Systematic Macro managers have averaged 6% since 2008, while the median annual returns for Discretionary Macro managers have averaged 6.4% through the same period. Investors need to take these figures with a pinch of salt, given the limited pool of managers that HFM had access to years ago, but the returns do illustrate the range of outcomes that investors have experienced.

FIGURE 2A: CALENDAR-YEAR RETURNS OF SYSTEMATIC MACRO MANAGERS (2008–2021 YTD)

Source: HFM; data as of 21 November 2021.

FIGURE 2B: CALENDAR YEAR RETURNS OF DISCRETIONARY MACRO MANAGERS (2008–2021 YTD)

Source: HFM; data as of 21 November 2021.

Amid such broad dispersion and variation, investors need to understand important distinctions and changes within the global macro landscape before determining whether it is appropriate to seek exposure to this sector as part of a diversified portfolio.

Global macro has evolved to attract an institutional crowd

Once synonymous with the hedge fund industry in the 1990s, when the likes of Julian Robertson Jr., George Soros and Michael Steinhardt made sweeping bets on currencies, interest rates, stocks, bonds and commodities around the world, macro gradually fell out of favour as the hedge fund sector pivoted towards an institutional client base. Today, more than 300 global macro hedge fund managers are operating around the world, the majority of whom are located in the United States and United Kingdom.

Contemporary macro managers use leverage much more sparingly than their predecessors and are far less inclined to make big bets or incur massive levels of volatility in their funds.

The types of strategies these managers run have changed dramatically in the decades since the so-called masters of the universe plied their trade. In the early 2000s, after the tech bubble burst, the industry’s newest investors—pension funds in particular—began to demand less volatile, lower risk-return patterns from their hedge fund managers that better matched their plan liabilities.

Successful macro managers adopted a more disciplined approach to trading and risk oversight, and attracted fresh capital, but the individualistic nature of the strategy began to shift. Contemporary macro managers use leverage much more sparingly than their predecessors and are far less inclined to make big bets or incur massive levels of volatility in their funds.

Although more aggressive than some other hedge fund strategies, global macro managers nowadays tend to prioritise return consistency over high performance, with most seeking to achieve returns of approximately 6%–10% per annum—although some strategies aim to deliver higher double-digit performance—while holding volatility within a range of 10%–15%. Investors do have some control in this regard: given that these strategies trade on margin, managers can readily scale volatility up or down to fit an investor’s risk-return profile by using a segregated account.

Systematic versus discretionary macro

Today, global macro managers usually fall into one of two stylistic camps: systematic macro and discretionary macro. Both groups tend to make use of a wide variety of macro-level investment securities across virtually all core asset classes (e.g. global equity, global fixed income, interest rates, currencies, commodities and volatility). Both apply top-down analysis to vast amounts of data; some managers also include bottom-up research on specific regions or markets. Both have the flexibility—in theory—to move quickly in response to changes in the market. Yet the two families are, in many other respects, extremely different.

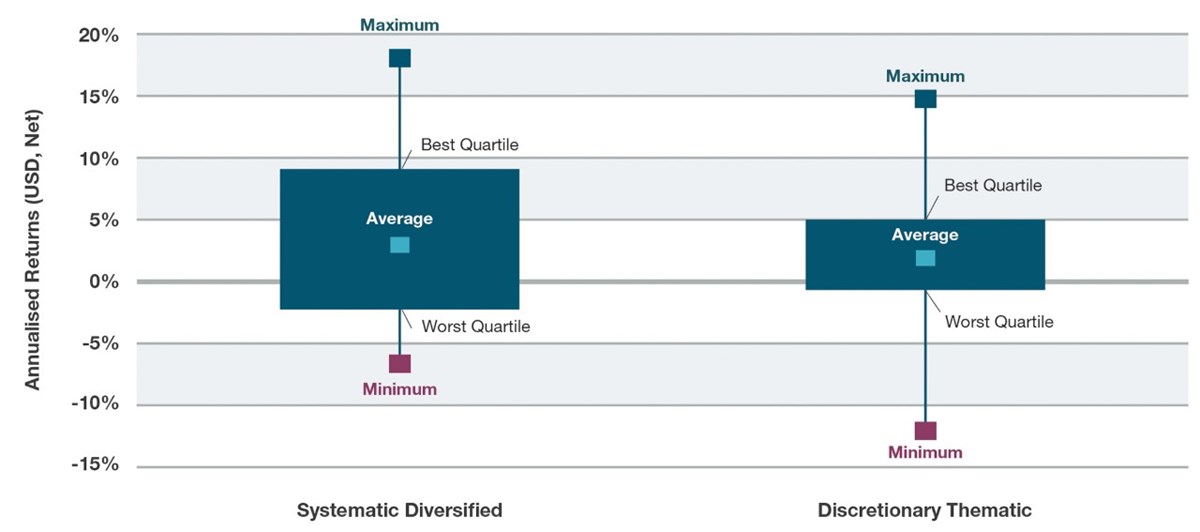

Systematic macro strategies have collectively exhibited less downside volatility in the years since the GFC than discretionary strategies.

Those managers that hew to a more traditional global macro investment style run discretionary macro strategies and take a top-down, directional (and still highly subjective) approach to market analysis, positioning themselves to capitalise on macroeconomic trends and dislocations. Portfolio construction is driven by the subjective views of individuals, founded in fundamental macro research that covers a wide range of sources (central bank publications, market sentiment surveys, political announcements, economic growth and inflation rates, unemployment data and more). This approach tends to result in concentrated and thematically oriented portfolios.

Systematic macro strategies, on the other hand, rely on quantitative models and statistical techniques. Managers build proprietary trading programs that seek to capture the long-, medium-, and short-term structural relationships that arise between macroeconomic risks and market responses, and formalise them as ‘buy’ and ‘sell’ signals. In essence these managers aim to systematise established discretionary global macro trading styles. This allows them to develop broader market coverage than a discretionary portfolio manager might be able to implement, with managers often trading as many as 50–100 markets across 20–40 models. It's worth noting that systematic macro strategies have collectively exhibited slightly less downside volatility over time, as shown in Figure 3, although the majority of that effect is attributable to performance throughout the GFC period.

FIGURE 3: QUARTILES AND ANNUALIZED NET RETURNS OF SYSTEMATIC AND DISCRETIONARY MACRO STRATEGIES (2008–2021 YTD)

Source: HFRI

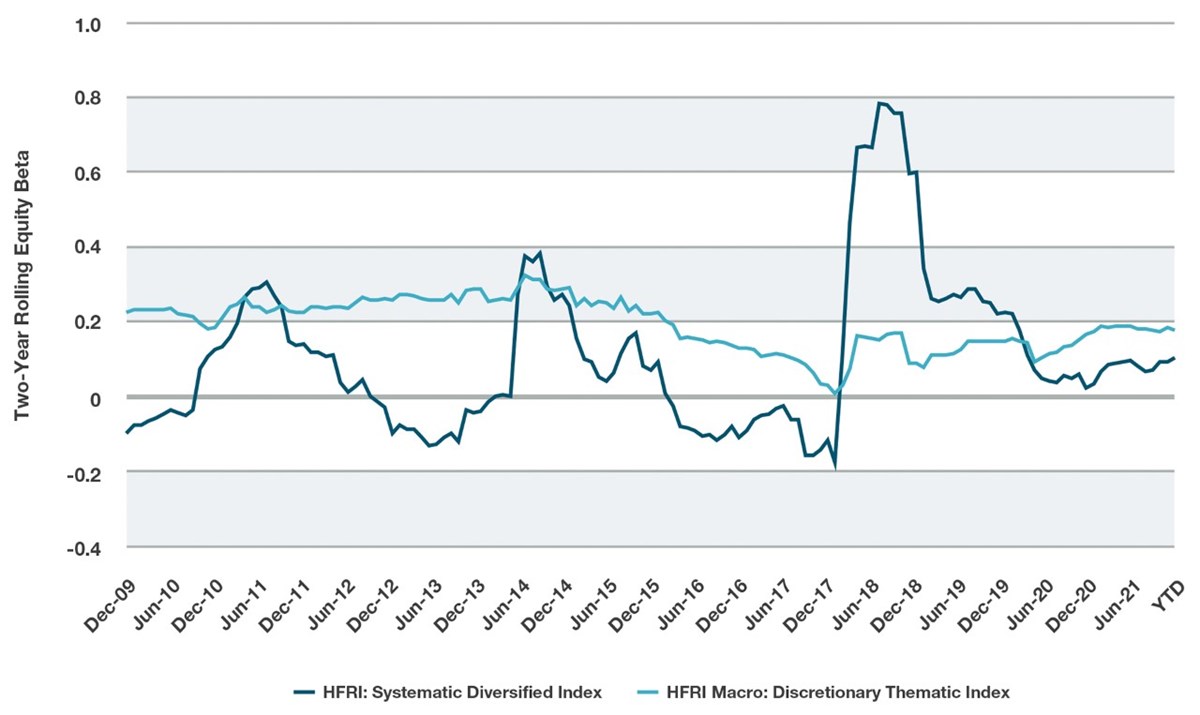

Systematic and discretionary managers tend to offer either low or variable net exposure to equity market betas. As shown in Figure 4, HFRI’s discretionary index has maintained a positive, albeit low, beta to equities, whereas the systematic index has proven more dynamic, with episodic periods of positive beta from a low or negative base. Systematic macro strategies often have an expected beta target of less than 0.20 “over a full market cycle”—and frequently incorporate a trend-following component that can serve to bolster their beta exposure when required.

FIGURE 4: TWO-YEAR ROLLING EQUITY BETA FOR DISCRETIONARY AND SYSTEMATIC STRATEGIES

Source: HFRI.

When looking at systematic macro managers, it can be helpful to sub-categorise them further: Some models are focused on relative value positioning, while others are more focused on directional market movements. Relative value models aim to identify mispricings in similar securities and position themselves for the prices of those securities to converge. These portfolios tend to be more strictly market neutral. Directional models, by comparison, will go long or short.

What about CTAs?

Systematic macro strategies—especially those with directional models—are often bucketed with commodity trading advisors (CTAs), because both seek to capture prevailing trends. CTAs have garnered considerable attention in recent months for their ability to provide impressive inflation protection.

Yet it is important to differentiate clearly between these two groups. Systematic macro strategies typically include trend-following programmes and have the capacity to respond dynamically to inflationary shocks and capitalise on subsequent asset price movements. While the trend-following components of CTAs are usually designed to wait for a trend to become established before entering or exiting a position, systematic macro strategies incorporate forecasting techniques and fundamental data to take a position in anticipation of a price trend—or trend reversal—before it becomes apparent. The goal is to deliver a smoother return profile than CTAs are equipped to deliver, particularly at market inflection points.

CTAs can also be hard to hold: years can pass before a trend reappears in markets, at which point a manager may be long an overbought market, or short an oversold one, just before the trend reversal occurs. Systematic macro strategies have proven to be more nimble and ‘weather-proof’.

Macro challenges lie ahead

Three key factors do now appear to be drawing investors to global macro, despite what many may see as a weaker decade for the sector: volatility, inflation and prospective equity market drawdowns.

While volatility has quieted somewhat since 2020, when the average daily closing price of the VIX was 29.3, it appears unlikely that it will settle back to pre-pandemic levels of 15–20. For the first three quarters of 2021, the VIX has averaged 21. US core inflation (excluding volatile food and fuel costs) has already hit 5% against a backdrop of global supply-chain chaos and staffing shortages in transportation and logistics. Central banks are now talking tough about their willingness to raise interest rates if inflation doesn’t ease by late 2022.

The probability of near-term equity market drawdown does appear to be increasing. In November, the US Federal Reserve confirmed that it would gradually dial back the bond-buying stimulus it launched in the earliest days of the pandemic and other central banks have followed its lead. Current asset valuations in both equity and fixed income markets appear increasingly fragile: stock markets have once again touched historic highs, government bond yields are historically low, and credit spreads in investment-grade debt have tightened so much that they have little room for further contraction.

Markets are increasingly likely to behave in unpredictable ways in the months ahead as the list of possible macroeconomic catalysts, which was already long, grows even longer. While the average returns provided by global macro may not have wowed investors in the post-GFC era and careful manager selection is still key, today’s climate appears to be highly favourable for this family of strategies—and systematic macro in particular.

Key takeaways

- Although global macro strategies have delivered highly variable results in recent years, these strategies may prove useful going forward based on their potential to dampen portfolio volatility and deliver uncorrelated returns.

- Given the heterogenous nature of global macro strategies, investors need to pay particular attention to manager selection and understand the distinctions between discretionary and systematic approaches to trading.

- As investors continue to use liquid alternatives to make their portfolios more robust—and less equity dependent—global macro strategies will continue to play an important role in portfolio construction.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.