English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Robert Doyle

Director, Equity

Recent bfinance reports highlight the extent to which style factors have driven equity returns through the COVID-19 crisis, with value materially underperforming at one end and quality delivering a high degree of protection at the other.

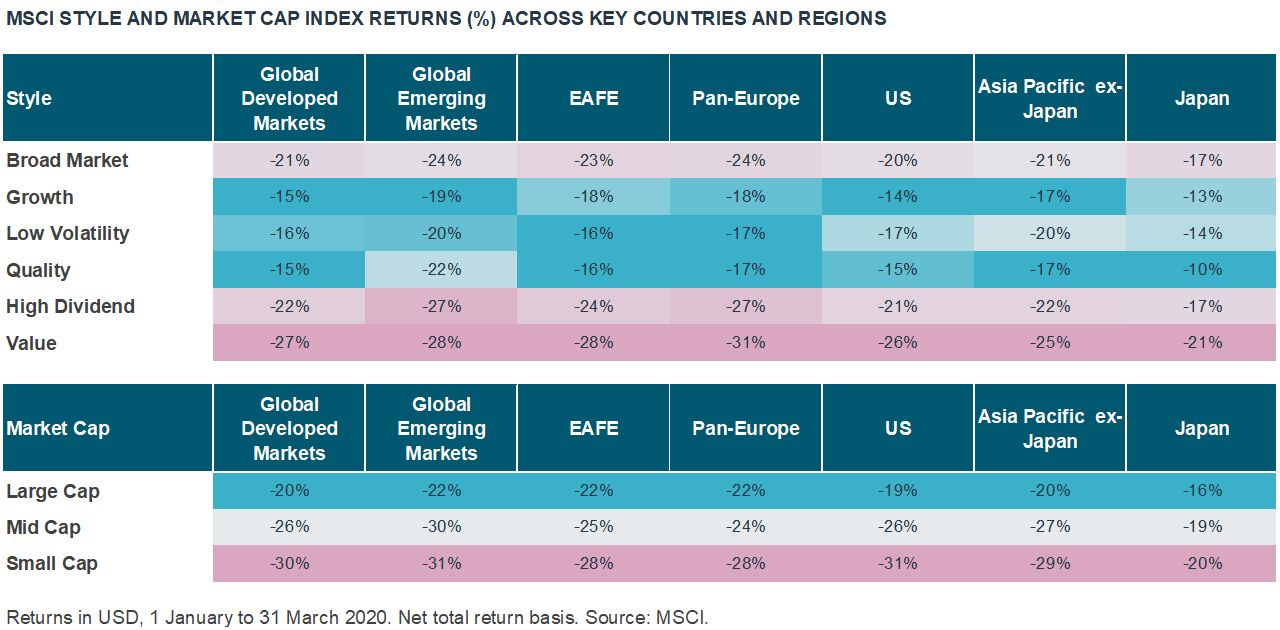

The first quarter of 2020 saw extremely high dispersion in the returns delivered by active managers, with a 42% difference between the best and worst performers in Global Developed Equities and a 6.4% spread between managers in the top and bottom quartile. Both figures are more than twice as high as those we have seen in recent, more “normal” quarters. A substantial amount of this variation can be attributed to style and size, where market indices showed considerable dispersion (shown below). For example, in global developed markets, the MSCI World Quality index was 12% ahead of the MSCI World Value index, while large caps outperformed small caps by 10%.

Based on both theory and practical evidence, one would expect quality and low volatility to outperform other styles in sharply declining markets, and this was indeed the case in Q1. The relatively strong performance from Growth indices can be attributed to a strong start to 2020, with this style outperforming all others through the first six weeks of the year. Value, meanwhile, underperformed substantially across all regions throughout the period while high dividend stocks, often closely associated with the value factor, also struggled.

These results contrasted with the fourth quarter of 2018, when a market “correction” saw the MSCI World Value index (-11.3%) beat its Growth counterpart (-15.4%) by 4%. That particular downturn was, to a large extent, driven by valuation concerns around growth (particularly IT-related) stocks following an exceptional 2017. In declines led by recessions or general economic weakness, growth and quality tend to fare relatively well. The perception that growth investing is more “risky” than its value counterpart appears increasingly flimsy.

The results of ESG indices are not shown here, but many of these also beat market cap returns in Q1. ESG strategy resilience is more evident when we look at the results delivered by asset managers that have been judged (by bfinance) to exhibit strong ESG integration into investment processes – a subject discussed in more detail below.

Are active “style” managers delivering?

Equity styles can be accessed in various ways – smart beta, systematic active equity strategies that have a high quantitative input for stock selection, and fundamental active equity managers that have a distinct leaning (sometimes advertised, sometimes not) towards a particular factor or factors.

Historically, the active piece has been dominated by investors describing themselves simply as having a growth or value bias. Today we find (in Developed Markets in particular) an increasingly varied and deep bench of active managers that have clear exposure to one or more styles – the most prevalent being quality, quality growth, low volatility and income, alongside growth and value. Indeed, the increasingly inflated markets of the last three years have driven a growing proportion of bfinance clients to seek active managers with style tilts that should theoretically enhance resilience (e.g. quality and low volatility). So, how have managers within these different style groups performed versus the benchmark, versus each other, and versus style indices that seek to capture the same exposure(s)?

Quality-focused active managers seem to beat Quality indices with a high degree of consistency

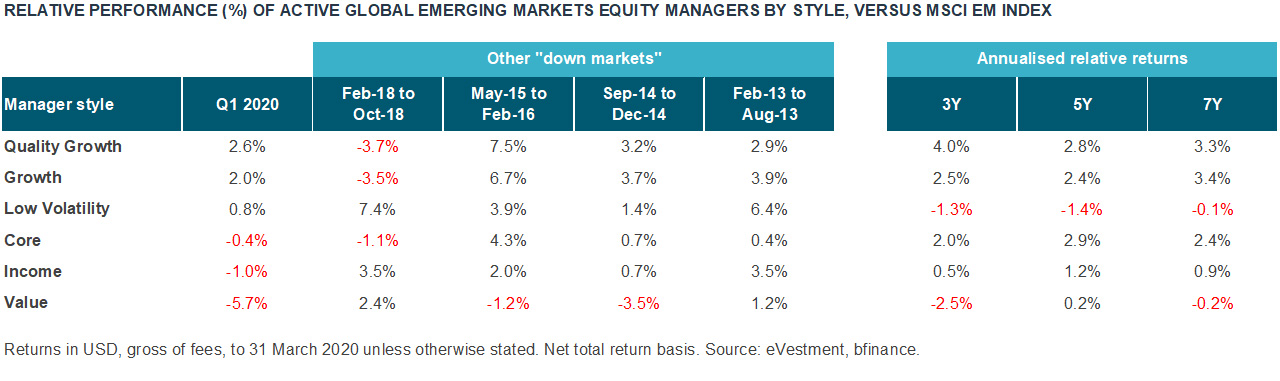

Over the last few years, bfinance has developed composites of managers with strong exposure to each of the styles below, basing the classifications on our analysis of the managers’ underlying portfolios. How managers label themselves is not relevant to this analysis: the portfolios speak for themselves. (Note: it is quite common for managers with strong low volatility or value exposure to accurately label themselves as such, whereas “quality” can mean very different things to different people – few, if any, managers would describe themselves as being focused on low quality companies!). The table below shows the results of these composites in Q1 relative to the MSCI World index and, by way of comparison, their performance through other periods (three, five and seven years, as well as other recent down-markets).

The median active global equity manager, as usual, delivered returns on par with the market. However, as shown above, managers focused on quality in global developed markets continued a very impressive multi-year run by delivering healthy outperformance in Q1 – on average nearly 8% ahead of the MSCI World index – aided by higher weightings in areas such as consumer staples, healthcare and IT, as well as a general focus on companies that can better withstand downturns (e.g. less cyclical business models, high levels of free cash flow). What is not shown here is that these managers also beat the relevant Quality index by nearly 2% (-13.5% versus -15.3%) in Q1. It’s worth noting that “quality” active managers do seem to beat Quality indices with a high degree of consistency: net of fees, the global quality manager composite has beaten the MSCI World Quality Index in seven of the last ten calendar years. We also find that the composite outperformed the Quality index in all market corrections and sustained downturns since (and including) the 2008 global financial crisis.

Managers with a strong exposure to growth factors also fared well in Q1, although – as mentioned previously in the case of the index performance – performance prior to the COVID-induced decline was a key contributor. In global developed markets they beat the MSCI World by 6%; in emerging markets they beat the MSCI Emerging Markets index by 2%. Growth managers have not shown a clear trend in terms of relative performance in down-markets through the last decade, though they have given strong performance through the last three, five and seven years (as one may expect in what has generally been an extended bull market). Interestingly, as was the case with quality, growth managers in global developed markets have an excellent record in outperforming the relevant (MSCI Growth) style index, having done so in eight of the last ten calendar years, while compounding an additional 3% of return per year over the last seven years.

Value and Income indices struggled in Q1, and the same was true for active managers with dominant exposure to these factors: active value managers trailed the MSCI World index by 6.4%. Manager performance in both cases was broadly in line with the relevant MSCI indices (Value and High Dividend Yield). This could be considered as particularly disappointing for value, where active managers have historically outperformed the MSCI Value index – albeit by less significant margins than their quality and growth counterparts. Indeed, global Value managers beat this Value index in eight of the last ten years (2018 being the only notable exception).

As with developed markets, emerging market equity managers with a value style endured a difficult quarter. The only ‘mainstream’ style factor that was really rewarded during the March downturn was quality, and this narrowness is unusual. When looking at the manager universe, we find that – relative to developed markets, where a large number of managers are focused purely on quality – very few such managers exist in the EM space. In pretty much all cases, managers with a clear quality bias have other style factors in place, most commonly growth. “Quality growth” managers did outperform the MSCI Emerging Markets index, but that outperformance was much more modest than we saw in developed markets – 2.6% on average. Further analysis of these managers indicates that those positive relative returns were driven more by active selection – stock, sector or country – than any favourable style tailwind.

ESG managers show their quality

The list of composites above does not – yet – include an ESG grouping. This is an area we have closely assessed – again, based on our analysis rather than any managers “self-labelling” of strategies, which we find to be a relatively unreliable indicator. Our view is that ESG is not, in and of itself, an investment style, instead being a form of analysis that can integrate within any type of investment process or style with the aim of making “better” long-term investment decisions. We note that MSCI – which publishes a variety of ESG indices – also does not classify ESG as a style within its “Factor Classification Standards”. Indeed, its ESG indices are constructed to have minimal (less than 1%) tracking error versus a broad market index, with the dual purpose of focusing on stocks with positive ESG scores while remaining country, sector and industry neutral, thereby eliminating any style biases.

We find that those managers with particularly strong ESG integration tend to have a broader focus on the quality factor and, to a lesser extent, growth. A dedicated ESG composite would have an overwhelming bias to these two styles, particularly quality. This is somewhat intuitive: quality managers generally focus on companies with business models that are sustainable over the long-term – an assessment which overlaps strongly with positive ESG characteristics. Indeed, we would consider each manager featuring in the quality composite to have a credible level of ESG integration within their process.

Looking ahead

Based on conversations with clients and prospective clients during April, it is clear that the events of Q1 have prompted asset owners to not only examine the performance of their active equity managers (i.e. whether they delivered as expected), but to consider whether these managers remain “fit for purpose” on a medium to long-term view. In thinking ahead, asset owners should give strong consideration to the style characteristics of their active managers and overall portfolio to ensure they are positioned to deliver an appropriate return pattern, with the aim of avoiding any unintended outcomes in particular market environments. In doing so, asset owners should be cognisant of the array of different investment styles available and move away from the “growth / value paradigm” that, in our view, is no longer relevant.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.