Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Weichen Ding

Senior Associate, Equity

Although the Low Volatility factor has delivered disappointing results during the Covid-19 era – and active low-volatility equity strategies produced extremely mixed performance outcomes as a result – some managers differentiated themselves through portfolio construction, sector positioning and the level of volatility reduction being targeted.

“[The problem] may simply be that the min vol anomaly first identified by Scholes and Black – greater and steadier returns – was simply too much of a free lunch to last forever, and has now gone the way of the dodo.” So concludes an article by the Financial Times’ global finance correspondent in March 2021. These are damning words for a factor that has, after all, provided at least some resilience in virtually every market downturn in recent memory.

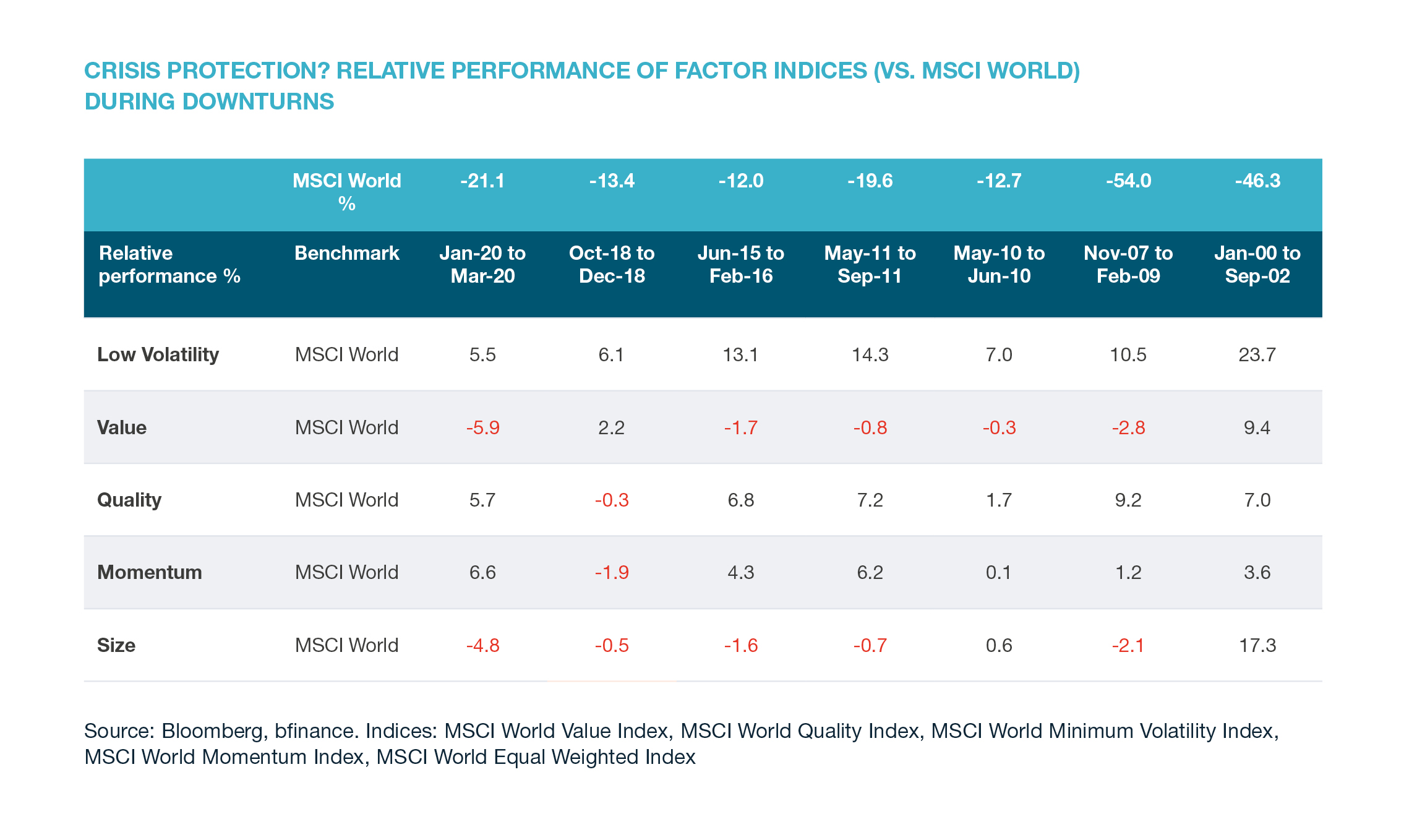

Crisis protection? Relative performance of factor indices (vs. MSCI World) during downturns

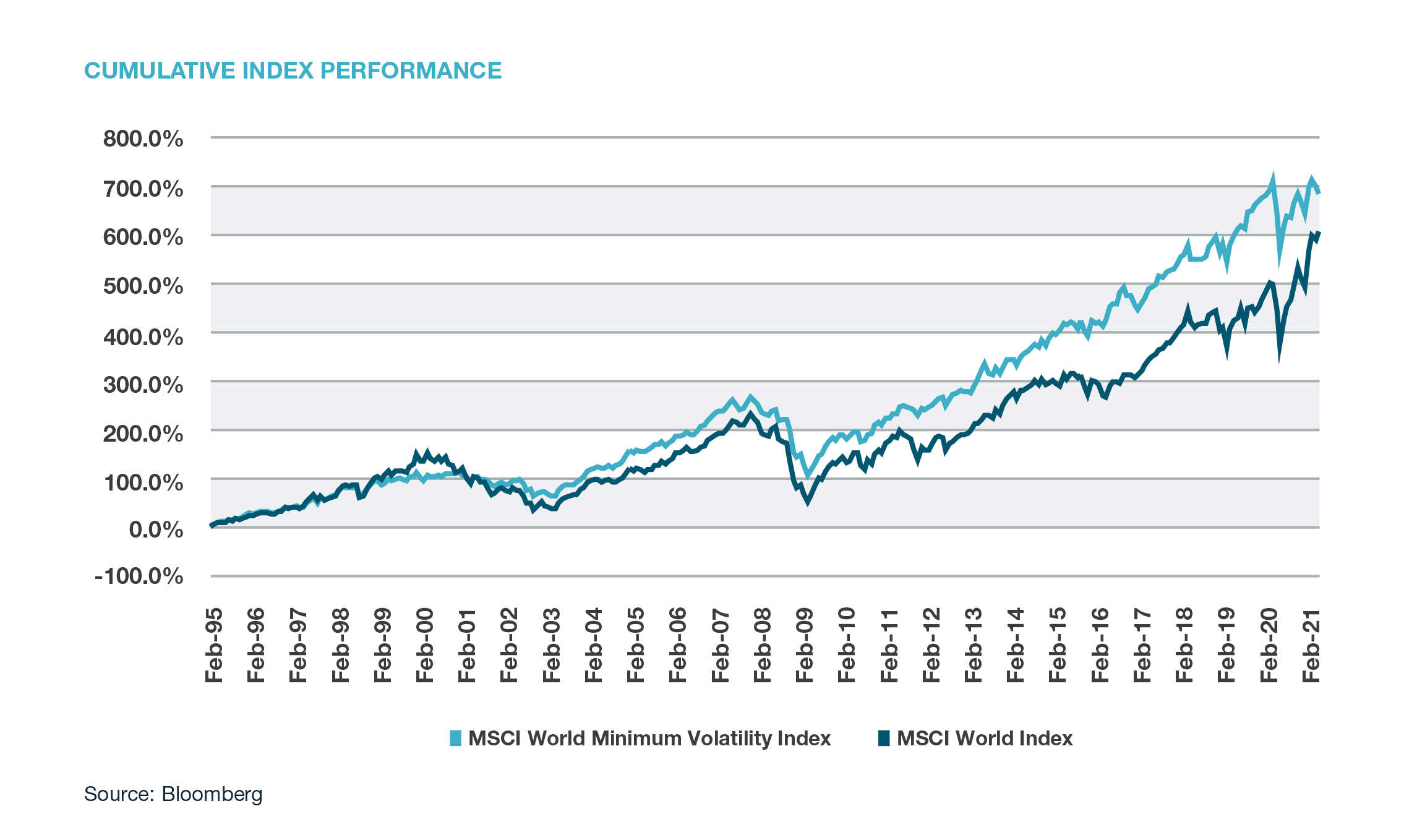

Low Vol, a favoured risk premium in the post-Global Financial Crisis factor-investing boom, fell from grace most decidedly in 2020 – a year in which the MSCI World Minimum Volatility Index returned just 2.6% versus the MSCI World Index’s 15.9%. Low Vol’s troubles have extended into Q1 2021, with lacklustre results sitting in stark contrast to the substantial resurgence of the Value factor.

The explanation behind recent poor performance is two-fold: the factor provided weaker protection during the March 2020 downturn in global equities than it had given during previous crashes, then lagged through the market’s subsequent gravity-defying bull run. While the latter is typical, the former was decidedly unexpected. The Covid-induced crash was, after all, one that turned conventional wisdom about downturns on its head, with technology (typically a more cyclical sector) showing the only real immunity while defensive sectors such as utilities fell victim to the sell-off. Between the unusual sector performance and a very wide sell-off (which produced beta compression), the Low Volatility factor – and with it an extended family of index and ETF products – came unstuck.

Those who still believe in the potential advantages of Low Vol should use the lessons of 2020 to reflect on the different ways in which these strategies can be approached.

Yet what of active managers? Quant equity managers were offering this style to investors on an active basis even before index strategies became popular, with many firms launching products between 2005 and 2010. There are now more than 60 active global equity strategies available with an explicit low-vol angle, of which 50 have a track record of more than five years. Among them, the median performer in 2020 (+3.8%) came out only 1.2% ahead of the MSCI World Minimum Volatility Index and still 12.1% behind the MSCI World Index, while the top performers still lagged MSCI World but beat the Min Vol index by nearly 12% (gross of fees).

In this article we explore what separates active low-volatility strategies from passive approaches and look at the key elements that set active strategies apart from each other.

The rise of the ‘free lunch’ factor

Although the low-volatility risk premium was discovered in the early 1970s, it did not lead to a popular investment style until after the Global Financial Crisis (GFC), which began in 2008. A combination of causes propelled it into the mainstream. First, investors began rethinking how much equity risk exposure they wanted in their portfolios after a crash of such seismic proportions. Second, the demand for factor investing began accelerating from 2008 onwards due to investors’ growing awareness of the extent to which active management returns were being driven by exposure to certain risk premia (‘smart beta’ became a must-have topic at industry conferences). Third, academics had already begun producing a growing body of research on the low-volatility factor, starting in the early-to-mid 2000s.

That body of research gave more thorough evidence for a phenomenon that had been identified thirty years earlier: high-beta and high-volatility stocks underperform low-beta and low-volatility stocks, defying basic finance principles that suggest that higher risk should be associated with higher reward. Academics also charted the behavioural biases that give rise to this anomaly: investors overestimate their stock selection abilities; buyers are attracted to more volatile securities (the so-called “lottery effect”); manager performance incentives can drive riskier investing; and portfolio leverage constraints encourage the use of higher-beta stocks.

Asset managers began offering this new investment style in the form of active quantitative equity strategies between 2005 and 2010. A few years later, index providers such as MSCI and Standard & Poor’s started to create low-volatility or minimum-volatility indices. In all cases, the premise was roughly similar: to create products for investors seeking long-term returns that would be broadly in line with (or indeed slightly better than) a market-cap-weighted index, but with significantly lower volatility. Investors would have to accept that they might not receive the full benefit, or upside, of rising markets (e.g. 80-90% upside capture) but could expect a significant degree of cushioning in downturns (e.g. 60-70% downside capture). In the decade prior to 2020, this premise was largely borne out in practice.

What have active low-vol managers delivered?

Active low-vol managers do not, in general, seek to provide as much volatility reduction as minimum-volatility indices. The latter usually seek to achieve the lowest possible volatility, irrespective of alpha; the former seek to find a balance between minimising volatility and achieving a certain level of return.

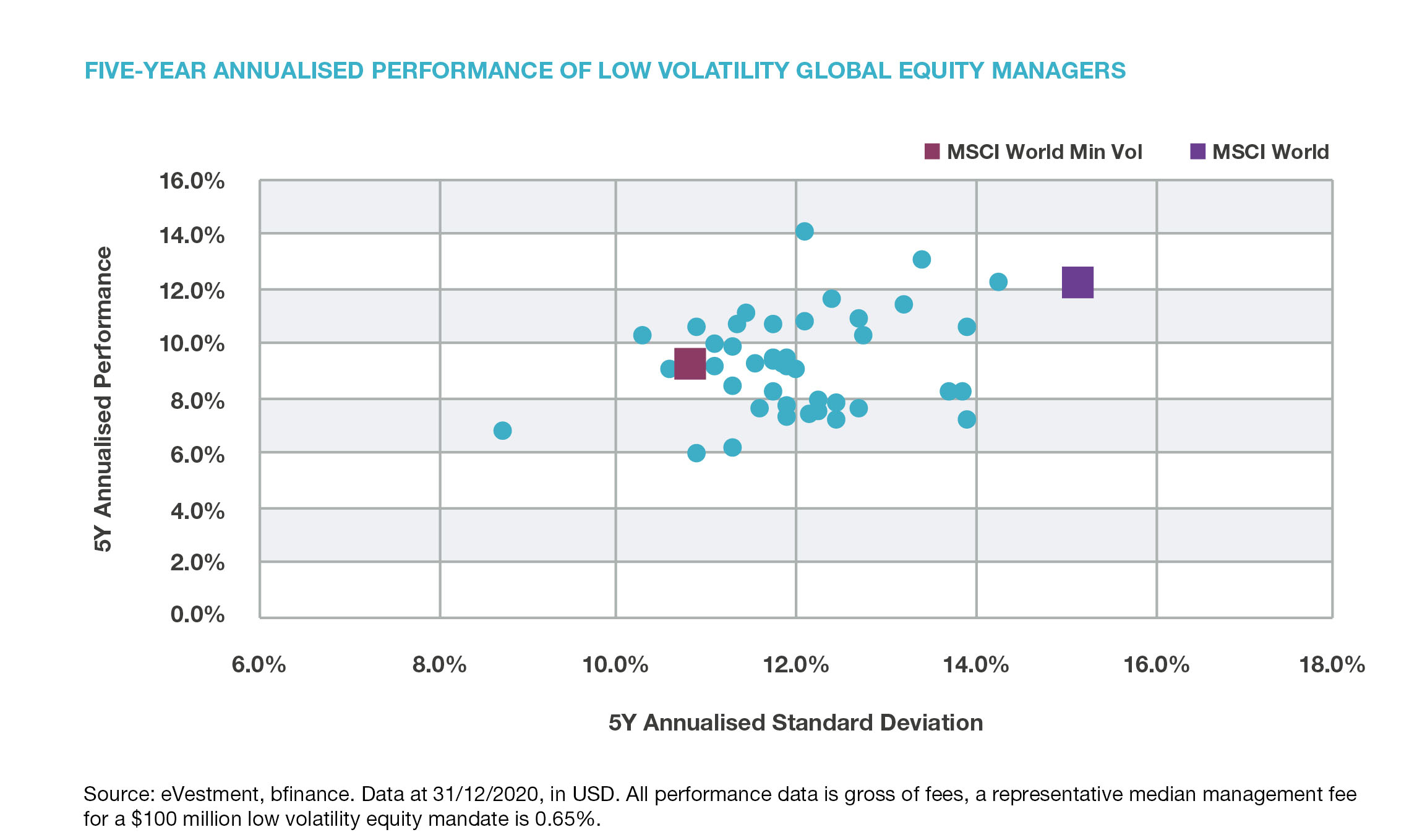

This risk-reduction premise has largely been fulfilled, based on the five-year risk/return data shown above: active managers have delivered volatility reduction of 10-40%. Average performance, however, has not met investors’ expectations, notwithstanding wide dispersion between the stronger and weaker managers. Few funds have succeeded in beating the MSCI World Index over the past five years – in large part due to the events of 2020 – and only around half of them have beaten the MSCI World Minimum Volatility Index over this time horizon.

Looking specifically at 2020, we see the average active manager beating the Minimum Volatility Index by 1.2% (gross of fees), despite underperforming in Q1, due to a higher risk profile. As noted above, the strongest managers ended up nearly 12% ahead of the Min Vol index (gross of fees), although they all fell short of the MSCI World. Those stronger performers also tended to have more sector-neutral approaches, less extreme volatility-reduction targets (strategies with 15-25% volatility reduction outperformed those with >35% volatility reduction) and less exposure to the Value factor.

Readers may be surprised at the degree of dispersion in returns, especially over a five-year view, for what is essentially a quantitative strategy whose returns should primarily be explained by factor exposure.

Key differences in active management approaches

What does Low Volatility mean in an active management context? It can be helpful to think about the universe of available strategies comprising two groups: those that generate a low-vol profile at the portfolio level and those that generate it at the stock level.

The first approach – Low Vol at the portfolio level – is more common. In these cases, quantitative equity managers have typically already developed an alpha model to rank stocks for their core strategy. Commonly, though not always, that same alpha model – or a tailored version of it – will be used for the low-vol strategy. Managers will then adjust their optimisation objectives to build a portfolio with desired risk/return targets: In the case of a core (beta = 1) strategy, the optimisation instruction might be to maximise returns with volatility similar to the benchmark; in the case of a low-vol strategy, the optimisation could be adjusted to achieve a certain level of volatility reduction. Managers typically apply risk models during the optimisation stage, incorporating other information such as correlation and idiosyncratic risk.

The alpha models and risk models used by different managers produce significant performance differentiation, yet many other drivers of disparity also exist – some of which can be even more influential, as the Covid-19 period aptly illustrates. They include:

- Sector bias. Some managers who use this method are sector-neutral to avoid unintended performance impact in scenarios such as 2020; others are less sector-constrained, typically with the result that they are overweight defensive sectors and underweight cyclical sectors.

- Amount of volatility reduction. Managers have very different volatility-reduction targets: 15% to 25% is quite common but some push further to target a true min-vol profile (35% reduction or more).

- Currency optimisation. This element is a major consideration if an investor’s base currency is not USD; currency volatility can significantly affect overall portfolio volatility.

- Other factor exposures. Although some Low Vol managers do consider other factors, including Value, Momentum and Quality, our research indicates that the tilts towards them do not tend to be significant.

The second approach – Low Vol at the stock level – involves using the low-vol factor to rank stocks based on their volatility and build the portfolio according to stock rankings without using an optimiser. There is some disagreement on whether it is preferable to use this approach. Some researchers argue that this type of strategy is less sophisticated as risk models are not applied; others show that this method offers greater transparency to investors and should lead to similar outcomes.

Looking ahead

Recent troubles will undoubtedly have a significant and lasting effect on client demand for low-volatility strategies; this shift is already evident in bfinance’s own manager search figures.

Yet, for investors who are generally concerned about equity market drawdowns caused by economic slowdowns (as opposed to those created by pandemic-related lockdowns), Low Volatility still has a significant potential contribution to make in terms of reducing overall risk exposure. Key differences between the 2020 crash and those that preceded it – or those that may follow – need to be kept in mind.

Investors who still believe in the potential advantages of Low Vol should, however, use the lessons of 2020 to reflect on the different ways in which these strategies can be approached: active versus passive, the level of volatility reduction targeted, neutrality or flexibility in sector exposures, top-down optimisation versus bottom-up factor-based construction, and so forth.

It is also important for investors not to look at the Low Vol question in isolation but to consider their portfolio’s overall exposure to all factors that have been established as academically significant. Investors may also want to think about the interplay between factor exposures, such as the role of Quality (low fundamental risk) alongside Low Volatility (low statistical risk). Each of the major factors – Value, Momentum, Size, Quality, Low Volatility – can underperform in the short term, sometimes for extended periods. Investors must consider how they handle such events and ensure that lack of institutional tolerance for difficult periods doesn’t undermine a proposed long-term strategy.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.