Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

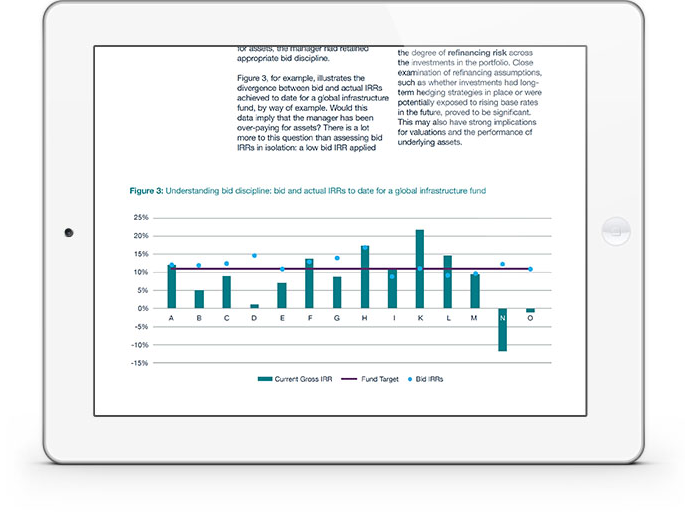

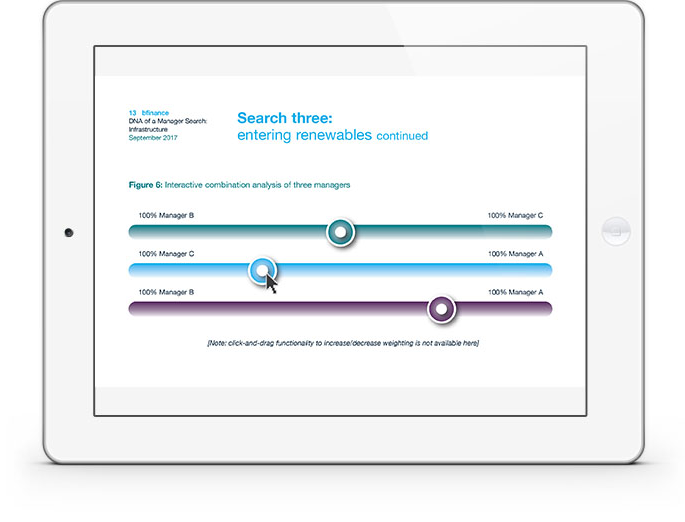

Three searches: “over-priced opportunities”; “combining exposures”; “entering renewables”.

Greater risks: As available returns have compressed, managers are increasingly taking on more risk – and different types of risk –to target performance in line with recent years. Greenfield exposure has increased; the average proportion in classic core has declined; the divide between listed and unlisted infrastructure has started to blur.

Evolving manager universe: the rise of ‘mega funds’ and the proliferation of sector-specific or region-specific players, leading to greater diversity than ever before.

Professionalisation: “In infrastructure, as in private equity, managers have undergone significant professionalisation as adding value has become more critical to deliver returns,” says Anne Feuillen. “A decade ago managers could buy assets, structure them appropriately and that was enough. Today it is more important to see strong operational expertise in-house.”

Sourcing: investors should be cautious when examining managers’ records in this area, with a tendency to over-state the number of genuinely ‘off-market’ or ‘bi-lateral’ deals.

WHY DOWNLOAD?

The financial crisis ushered in a new era of unlisted infrastructure investment. But times have changed.

Three trends - high appetite for illiquid investments, the desire to reduce equity risk exposure after the lessons of 2008 and the subsequent need for income generation in an era of low rates - converged to create a ‘perfect storm’ of demand. Dealflow was healthy, buoyed by a stream of asset disposals by financially stretched corporates and privatisations from fiscally stretched governments.

Yet, if that period of industry expansion might be termed “Infrastructure 2.0,” we are now in a markedly different phase – “Infrastructure 3.0,” perhaps. With investors battling for the most prized (typically core) assets in developed markets, the result has been a steep increase in M&A and a significant drop in returns. Fundraising has also slowed down significantly in 2017 (Preqin), although the volume of dry powder has increased.

For those selecting asset managers the current climate opens up new questions. Is my manager over-paying for assets? Are return expectations too high? Is this fund too large for this strategy now? How can we diversify our infrastructure exposure? Should we be investing more in non-OECD or greenfield assets? Are these deals really ‘infrastructure’ or, given their risk characteristics, more ‘private equity’ in nature?

In a market that has undergone major structural upheaval, expectations for risk factor exposures and returns should reflect new realities. We hope that this publication will give investors deeper practical insight on the obstacles and opportunities presented by today’s challenging investment environment.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.