Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

Is now a good time to invest in private debt?Although the risk/reward equation is still attractive in relative terms, this is not 2012. Most managers “expect” to achieve returns in line with previous years for their newer funds, but the underlying strategies, structures and risks have changed.

New challenges in manager selection: insights on the changes in the fund manager universe, the greater demand among investors for purer senior debt strategies, the increased appetite among European institutions for US private debt and the reduction in headline fees.

Unitranche evolution - why does it matter?Within ten years, unitranche has gone from novel concept to instrument of choice for private debt managers, providing a way of boosting returns without technically adding to the proportion of subordinated debt in portfolios. But investors should be cautious about the increasingly complex unitranche models that have emerged, the greater use of PIK and more.

WHY DOWNLOAD?

We are frequently asked: “is now a good time to invest in private debt?” While the answer may still be “yes,” the risks and rewards in this asset class have changed significantly in the past four years.

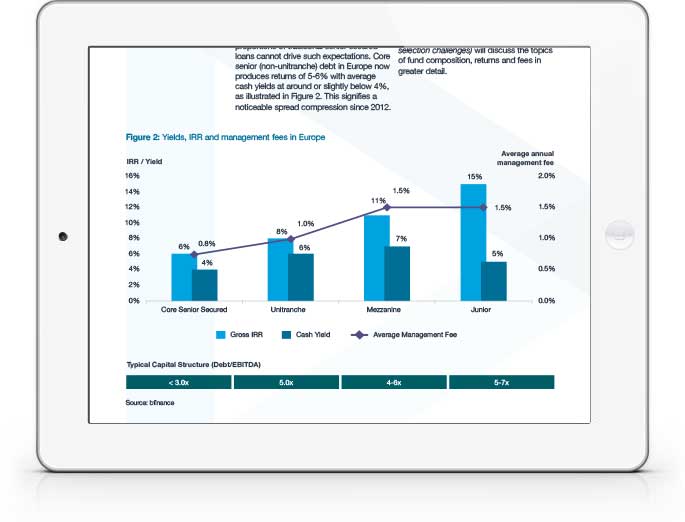

In part, this has been driven by spread compression, particularly in the upper-mid market (>$75 million EBITDA) space. Leverage (Debt-to-EBITDA) on senior direct lending has crept up as managers seek to keep IRR expectations on track, while deal terms for lenders have eroded (page 10). Yet the most significant factor may be the changing composition of senior debt funds.

There has been a minor style drift from subordinated to senior debt, and the senior portion is increasingly dominated by unitranche rather than traditional core senior secured lending. Furthermore, unitranche loans appear to be moving away from their original simple structure with lenders taking on more risk in the capital stack and higher multiples (page 7).

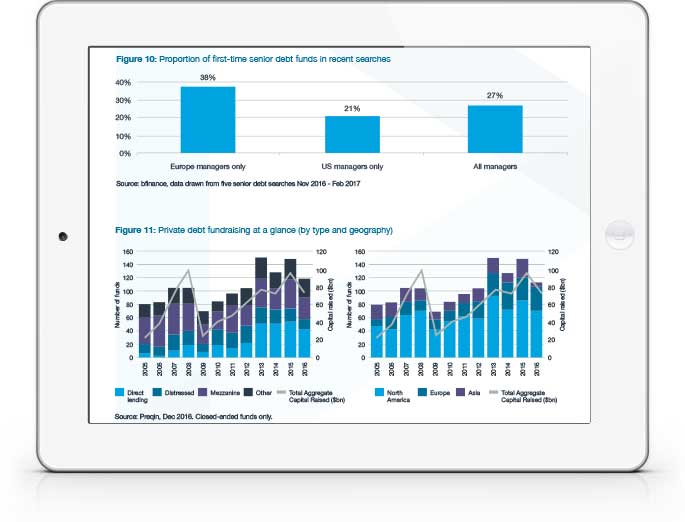

While some institutions are keen to stretch for returns in the current climate, recent bfinance consulting work reveals a growing appetite for purer senior debt funds. We would encourage such investors to focus on the nature of the senior debt as well as, if not more than, the headline proportion (page 15).

In addition, European asset owners are increasingly keen to invest in US private debt. Many have previously steered clear due to the greater leverage at fund level, unfavourable taxes and currency hedging costs involved. Yet asset owners should pay close attention to the many differences in how US and European managers actually generate returns page 14).

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.