Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Chris Stevens

Director, Diversifying Strategies

Following an extended period of ‘low-flation’, many institutional investors entered 2021 with negligible exposure to so-called ‘inflation protection’ strategies such as inflation-linked bonds and commodities. A year later, with inflation climbing above 5% in a number of developed economies, we take a closer look at commodity and CTA performance.

2021 will be remembered as the year when significant (and long-expected) inflation returned to developed market economies—whether it proves to be transitory or otherwise. Inflation measures across major developed markets (excluding Japan) were running at an average of c.5% at year-end and continued to climb higher in January, reaching 7.5% in the US.

Many pension schemes and other asset owners have preferred to rely on ‘inflation-sensitive’ asset classes—equities, real estate and infrastructure—to give some insulation against the value-eroding effects of inflation. These can satisfy in various scenarios, especially coupled with structural factors that can make inflation less damaging to an institutional investor (such as the positive impact of interest rate rises on funding ratios).

The preference has been influenced by the generally weak or poor performance of the more explicit inflation-linked strategies. The Bloomberg Commodity (BCOM) index delivered a 27% return in 2021 but the decade-long picture is still negative and institutional investors’ commodity allocations have been in secular decline. Inflation-linked bonds performed well in 2021, although today’s entry point is notably less attractive.

Now, with inflation data exceeding forecasts, investors must continue to re-evaluate, analyse and stress-test their approaches. Traditional equity and bond markets have experienced a turbulent start to 2022: January saw the MSCI World Index losing 5.3% and the Bloomberg Global Aggregate Index drop by 1.6%. Equity markets have been riding high after three years of double-digit returns, with volatility above historic levels. Public markets’ inflation sensitivity relies in large part on the ability of listed companies to pass on higher prices to their customers. In real assets, the inflation-sensitivity of real-life portfolios can differ considerably depending on the degree of exposure to rising rents/prices.

One group of strategies that drew particularly strong attention in 2021 (and which has continued into 2022) is Managed Futures or Commodity Trading Advisors (CTAs). Trend-following strategies are known for their ‘convex’ diversification profile versus equities (see How to Build a Hedge Fund Allocation). Yet the past few months have also seen commentators stressing their potential inflation sensitivity. Below, we take a closer look at how both commodities and CTAs have been faring.

Commodity markets regain (some) lost ground

The BCOM index (commodities) rose by 8.8% in January, following a 27.1% return in 2021. Although gold—which has typically been seen as offering protection from inflation—lost approximately 4% on a spot price basis during 2021 and other precious metals also saw price declines last year, all of the other sub-indices were up significantly, led by Energy (+52.1%), Softs (+44%) and Industrial Metals (+30.3%).

Yet the index is still around 45% beneath its 2011 high; its decade-long annualised performance sits at minus 2.85% with an equity-like level of volatility. While few market participants are expecting a return to the ‘commodities supercycle’ theme of the 2000s, an ongoing inflationary scenario would likely be highly supportive of positive performance.

Commodity-free CTAs struggling to perform

The CTAs/Managed Futures space is highly diverse, but largely comprises trend-following approaches that are aligned to persistent directional moves in markets. The Societe Generale CTA Index (SG CTA) of the 20 largest CTAs is almost entirely comprised of managers that either have a pure trend-following strategy or include trend-following as a significant component within a diversified set of macro models. The Societe Generale Trend Index (SG Trend), which features ten of the managers in the CTA Index, is a purer peer group for examining trend-following managers.

Over the past decade, CTAs have delivered positive—albeit rather anaemic—returns. The SG CTA index has returned 2.3% p.a. over the ten years to January 2022, while the SG Trend Index provided 3.1% during the same period. Strong diversification, however, has been evident: the Trend index had a correlation of 0.08 to the MSCI World Index over that decade, while the CTA index had a correlation of 0.10. They have also managed to deliver healthy results during some particularly challenging periods: in March 2020, for example, the SG Trend was up 1.8%. Recent performance numbers have been stronger: the SG CTA index returned 2.1% in January while the SG Trend index returned +3.4%, following returns in 2021 of 9.1% and 6.2% respectively. January’s gains for trend-following were driven by long exposure to commodities as well as short positions in fixed income—the ideal positioning for inflation-driven markets.

Although CTAs are one of the few strategies in which institutional investors are likely to have direct exposure to commodities, it is crucial to note that plenty of CTAs do not invest in this sector. The CTA acronym has long been a misnomer, with these strategies also trading the ‘financials’ of equity, bond and currency markets alongside the commodities markets where many of the first CTA firms had their roots. The choice to avoid commodities can be driven by a number of considerations, including the type of vehicle (it is more complex and costly to include commodities in a UCITS structure), investment beliefs or even ESG factors—some clients do not wish to be seen to be speculating on commodities, particularly food prices.

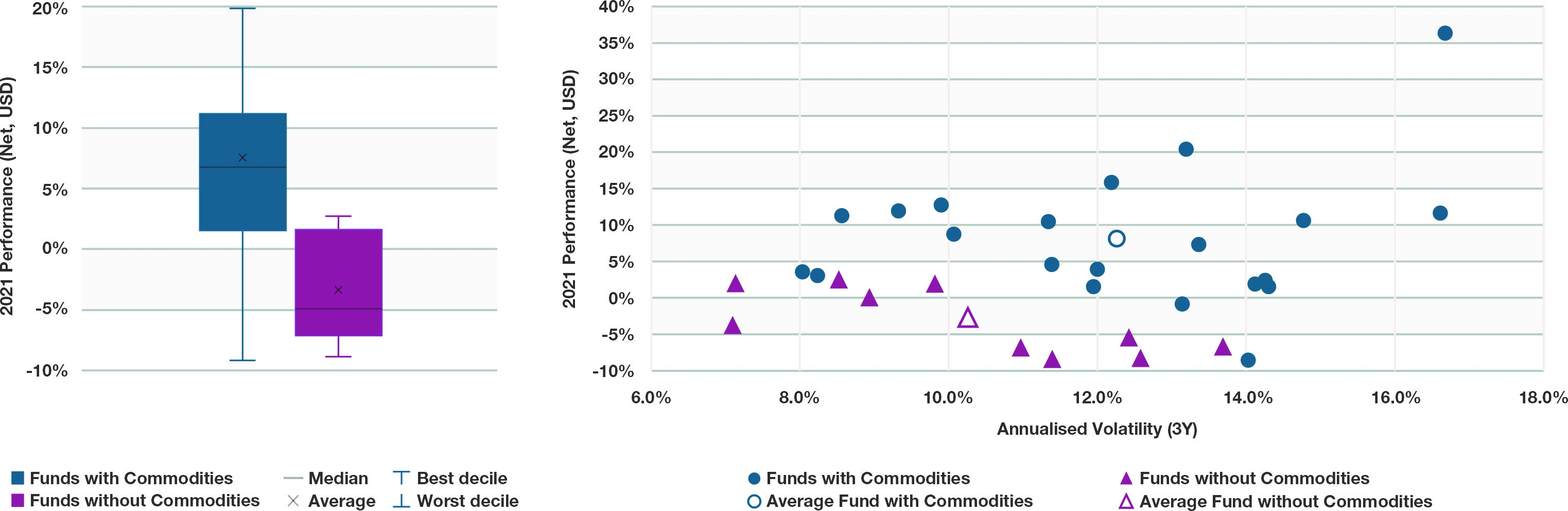

Using a peer group of managers assessed in recent bfinance research on trend-following CTAs, we can examine the performance of trend-following strategies that only trade financials (10 funds) and those that trade both financials and commodities (21 funds).

Performance of CTAs with and without commodities in 2021

Source: Drewry Container Forecaster

It is very clear that the inclusion (or exclusion) of commodities was a major determinant of performance in 2021 as the best quartile fund without commodities performed in line with the top of the worst quartile of funds with commodities. The median performance of CTAs ‘with commodities’ was +6.7% vs. -4.9% for those ‘without commodities’.

Allocation re-evaluation

CTAs remain among the most diversifying of liquid alternative strategies, able to provide positive performance when traditional markets suffer—although this is by no means guaranteed. While they tend to provide a bumpier ride for investors than their Systematic Macro cousins, we expect them to rise up investors’ agendas as we face the drawn-out macroeconomic effects of the pandemic. Investors may also want to revisit the idea of a dedicated commodities allocation, either in a long-only or long/short strategy.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.