English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  French (Canada)

French (Canada)

bfinance insight from:

Toby Goodworth

Managing Director, Head of Risk & Diversifying Strategies

In a rocky round-trip, January saw trend-following and equity-focused strategies soar while February brought sizable losses for many trend-following and short volatility factors. Yet not all Alternative Risk Premia (ARP) managers with exposure to these factors suffered. Instead, this rollercoaster quarter showcased the importance of implementation choices as well as factor selection.

The start of this year brought both the best and worst months on record for macro hedge funds and & CTAs in bfinance’s Macro & Trading composite. The severity of the February losses could perhaps be measured by the number of column inches, with many of the CTAs on our radar putting out articles and commentaries to their networks.

TESTING TIMES

It would be unfair, of course, to judge any strategy (or manager) by how they performed over such a short time period. ARP strategies should be measured by their long-term return generation and portfolio diversification benefits. However, the first quarter does provide a very interesting scenario test for how these strategies fared through a volatile period.

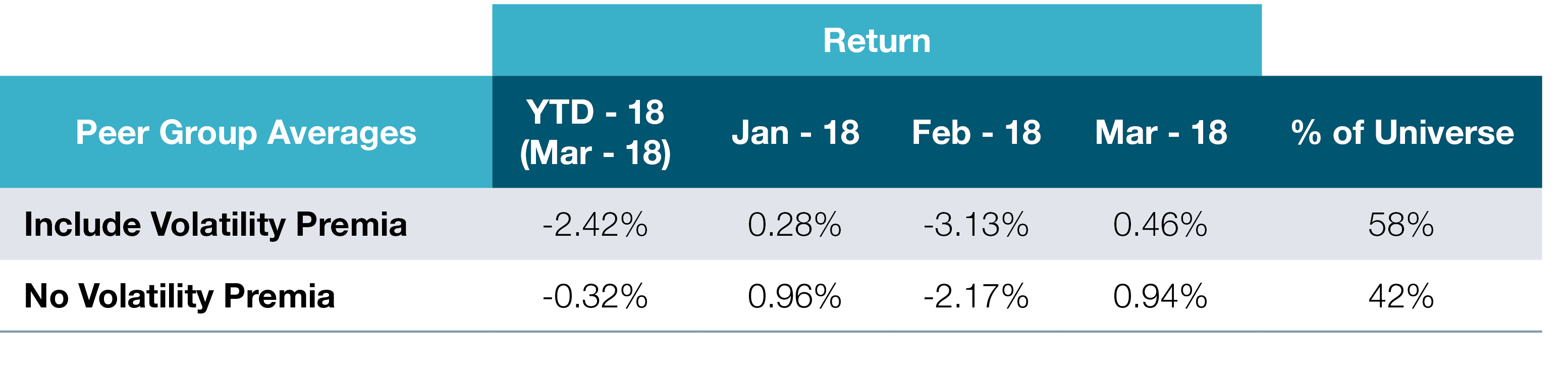

Among the 60-plus ARP strategies that are now available to investors, the vast majority have exposure to trend-following, while just over half (58%) have exposure to volatility premia, most commonly through short volatility strategies – in effect, selling insurance against turbulence. Other volatility premia strategies ‘trade’ volatility as an asset class or across asset classes, usually via VIX futures or variance swaps. Aside from trend following and volatility, there is considerable variation in the other factors used by these managers and, of course, in the choice of asset classes and markets.

Thanks in large part to the widespread use of trend-following, many ARP managers suffered losses in February and performance through Q1 was as one would expect from the sector. Also as one would expect, those managers using volatility premia fared worse than their peers – 44% worse, on average, in the critical month of February according to our data.

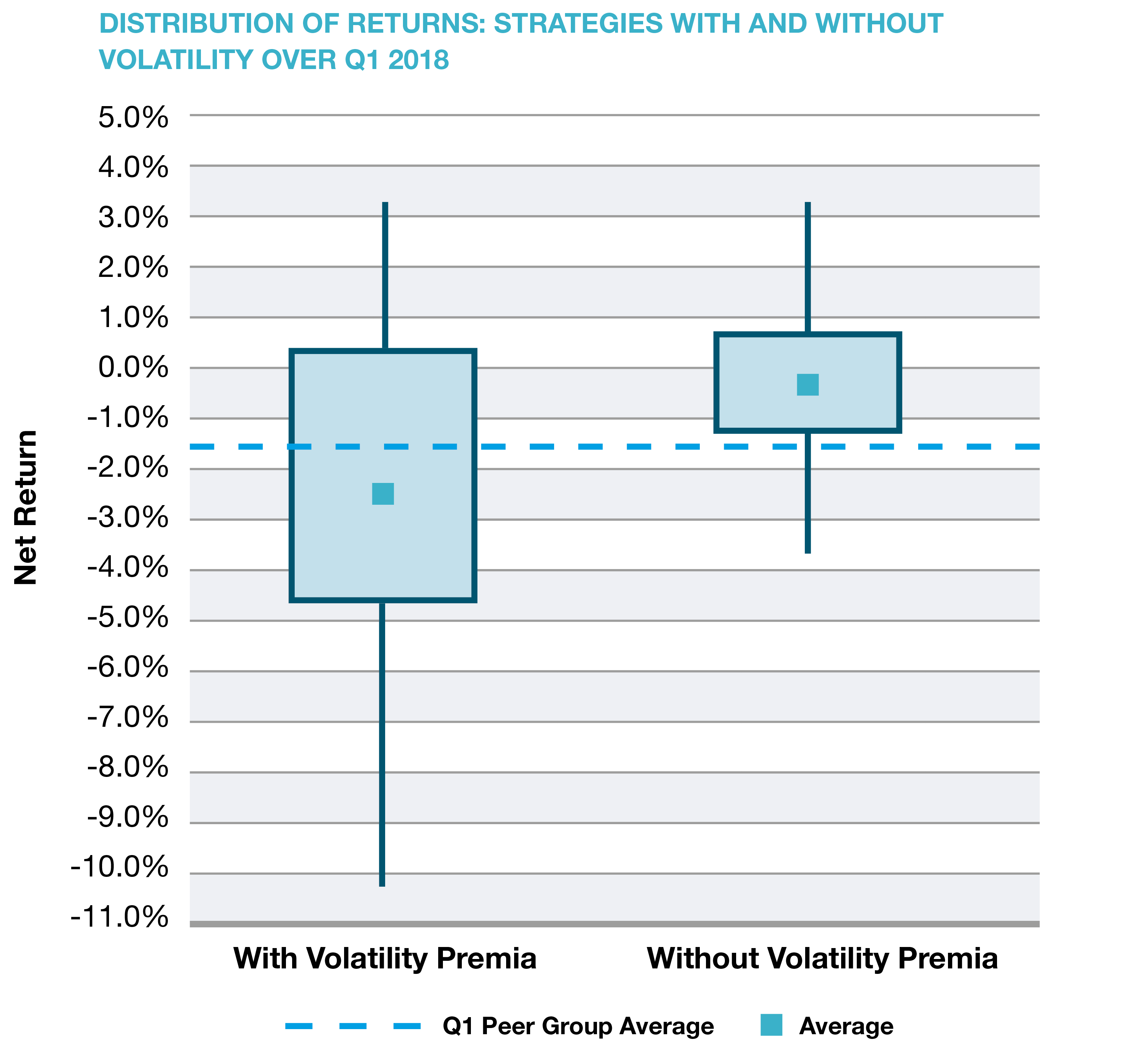

Yet, as the chart below illustrates, a significant minority came through the hardest period almost unscathed despite exposure to trend-following and, in some cases, volatility premia. The results shown below reveal the extent of the performance dispersion.

In addition, while strategies featuring short volatility were among the hardest hit during that month, the inclusion of this factor did not necessarily lead to bottom-quartile performance. Short-volatility has long been a “marmite factor” among ARP investors and managers, as discussed in The Changing World of Alternative Beta (bfinance, September 2016), with participants usually falling in either the ‘love it’ or ‘hate it’ camp. Those that favour short vol have taken February losses in their stride: gradual gains and occasional sharp falls are par for the course with this strategy.

FACTOR SELECTION VS. IMPLEMENTATION

For onlookers that are unfamiliar with the extent of the performance dispersion between rules-based strategies focusing on similar premia, this dispersion could be surprising. The selection of factors is often presumed to be the key decision in both alternative risk premia and its cousin, smart beta. It is certainly the decision that commands the most attention among investor teams and stakeholders.

So, looking beyond the initial choices of factors, asset classes and markets, what were the distinctions that made the difference? They fell into two key categories: portfolio construction and risk controls. For example, certain managers that were sizing positions based on volatility rather than expected shortfall or other tail loss measures suffered as a result in February. This was, in part, due to the asymmetrical return distribution and long left tail exhibited by short vol strategies. Some benefited from more sophisticated implementation, such as options that had been purchased to negate left tail extremes, or tighter risk controls around drawdowns through early February.

The data perhaps underscores the central argument made in How Have Alternative Risk Premia Strategies Performed? (bfinance, August 2017): implementation differences matter and deserve investors’ attention during manager selection.

However, investors should take care before concluding that managers who came out on top during this short period must, by extension, have a superior process. This certainly was not always the case. Factor choices, asset class selection, market choices and simple good fortune always play a major role. Analysis over a longer time period is essential to reach more robust conclusions.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.