English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  French (Canada)

French (Canada)

bfinance insight from:

Niels Bodenheim

Senior Director, Private Markets

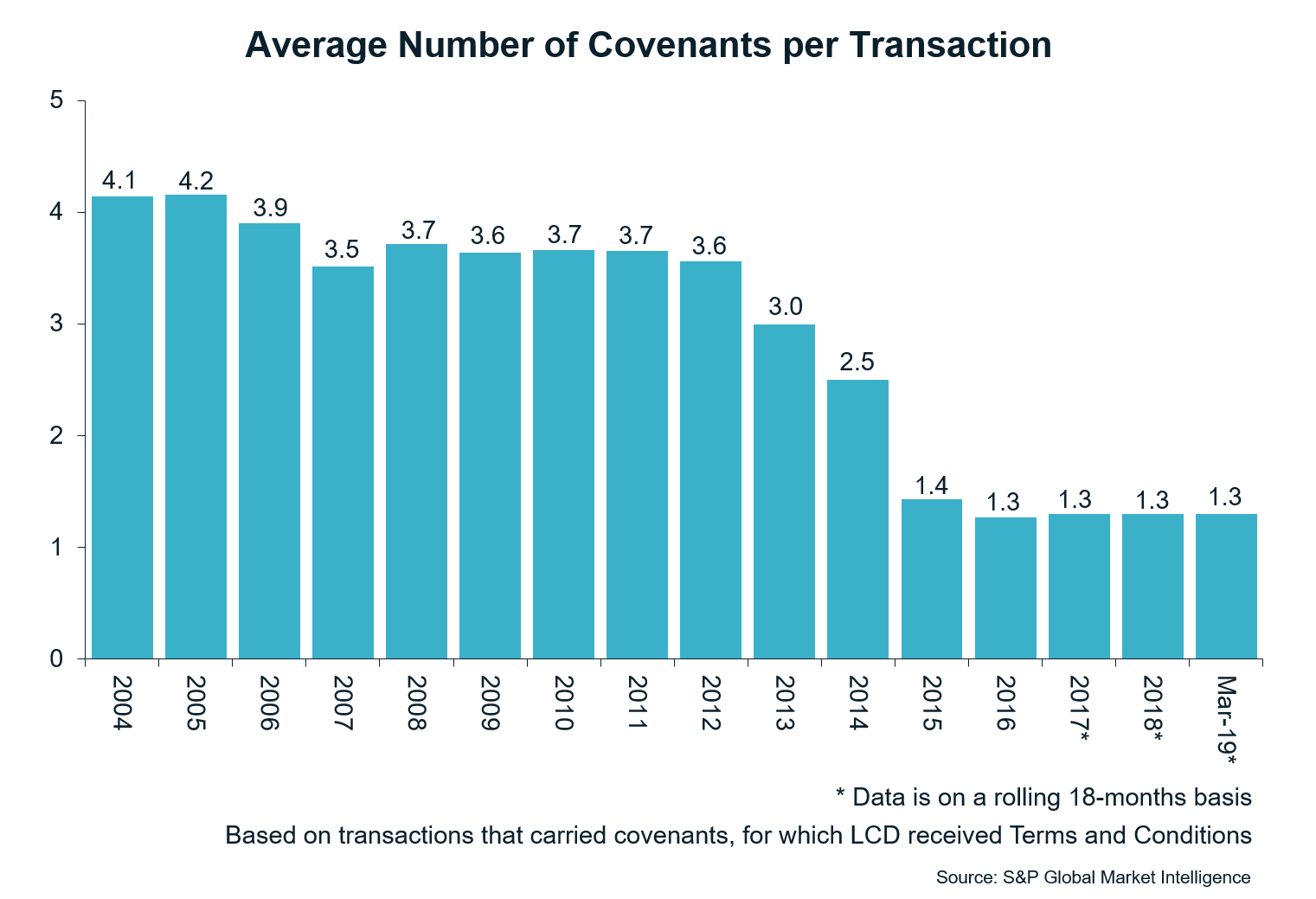

The declining number of covenants in private debt transactions has provoked concern among investors and industry commentators alike. Yet this emphasis on headline covenant numbers can be somewhat misleading. Allocators should hone in on more important, less obvious details: definitions of EBITDA or cashflows, “permitted baskets” and more.

It comes as no surprise that the number of covenants in private debt deals has been declining in both Europe and the US for several years – a trend noted in our 2017 paper Direct Lending: What’s Different Now? Where an investor might previously have expected to have three or four such agreements in place for mid-market sponsored direct lending, it is now relatively common to find only one.

The use of only one covenant is not in itself problematic or risk-elevating. After all, the covenant that remains widely used is by far the most important one, and the one that tends to get triggered first in the event of trouble: the leverage multiple (debt-to-EBITDA). Those for Cashflow Cover, Interest Cover and so forth are less significant. Although simplified terms can represent a shift of power from lender to borrower, with a high volume of capital chasing deals, the simplification is not necessarily to the lender’s disadvantage.

Where trouble really arises is not in the use of only one covenant, but in the calculations that underpin it, the allowances within it, and the contractual details outside of the covenants themselves.

CASHFLOW CONUNDRUM

With the relatively aggressive purchase multiples in today’s private equity transactions, it is crucial to consider the precise nature of the EBITDA figures upon which lending is done, and upon which covenants on leverage multiples are based. The real questions is: are you lending on true cashflows or on potentially inaccurate assumptions?

We are seeing EBITDA adjustments become more aggressive, and more frequent use of implied adjustments in calculations.

It is standard practice to factor in “adjustments” to EBITDA - the changes that are expected by the private equity sponsor. These can include “contractual” adjustments (e.g. a piece of business already signed) or “implied adjustments” (e.g. an assumption about growth in a particular area based on additional resources supplied or synergistic benefits from mergers).

We are seeing these EBITDA adjustments become more aggressive, and more frequent use of implied adjustments in calculations. Private equity houses, M&A advisors, debt advisors and due diligence consultants are becoming more lenient in their approach to adjustments. Different asset managers take different approaches to the EBITDA question.

TOO MUCH HEADROOM?

The amount of “headroom” in leverage multiple covenants has also been on the rise. This important caveat stipulates how much leeway the borrower will receive before the relevant steps outlined in covenants kick in. For example, if a borrower is allowed to go to a 5x leverage multiple with a 30% headroom, the lender would be able to step in at 6.5x. Today, we see transactions with debt entry points starting at 6.5x, but with a 30% headroom bringing us close to historically high purchase multiples of nearly 8.5x.

Yet, as with the number of covenants, the amount of headroom is not the critical point: the most important contributor to increasing risk, as above, is how cashflows are actually being estimated through adjusted EBITDA.

LOOK IN THE BASKETS

Beyond the covenants, it is crucial to examine how lenders are approaching “permitted allowances” or “permitted baskets.” These stipulations cover all manner of details: whether the firm has a right to take out mortgages, whether they may sell receivables, whether sales of stakes in the firm will go to equity or be used to pay down loans, to name just a few. These baskets can materially change the risks to the lender: they can amplify the financial burden or impair the borrower’s ability to repay the loan through the release of cash to other parties.

TAKING THE LONG VIEW

It is worth keeping rising risks in perspective. In strategies such as mid-market Direct Lending, a doubling or even a trebling in default rates from their current very low level and a substantial decrease in recovery rates would be unlikely to deliver catastrophic outcomes for the funds in question. Investors and service providers should remain focused on the most important issue: the overall risk/return profile that these strategies deliver over the long term.

That being said, a more challenging climate will undoubtedly reveal winners and losers. Investors with a careful eye on the detail during manager selection can mitigate their exposure to the risk of soaring defaults.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.