English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Anish Butani

Senior Director, Private Markets

Although infrastructure is renowned as an inflation-sensitive asset class, the reality varies greatly depending on the strategy type and asset-level specifics. Not all ‘inflation-linkage’ is created equal, and not all ‘core’ assets are hardy cockroaches ready to survive the inflationary fallout.

Investment in unlisted infrastructure equity—an asset class that is now USD700 billion in size, according to Preqin—continues apace. Data from Infrastructure Investor indicates that 2021 fundraising surpassed pre-COVID highs, with USD136 billion entering infrastructure funds, reflected in the record manager search levels that we have seen here at bfinance. Industry surveys, like this one from Natixis, continue to show investor intentions in favour of boosting exposure still further. Appetite has also been facilitated by the significantly improved availability of open-ended funds, which have drawn new types of investors to the space.

Among the various attractions of the asset class, inflation protection is increasingly taking centre stage. Close scrutiny of this aspect has, of course, loomed large during recent manager research and due diligence. After more than 20 years of non-inflationary growth in the western world, inflation has staged a serious comeback in 2021 and 2022. More and more economists have moved from ‘team transitory’—shrugging off price spikes as the result of heightened consumer demand or supply chain disruption—to ‘team permanent’. Yet the jury is still out on whether ongoing inflation is likely to be accompanied by strong or weak economic growth (see Figure 2 for detail on ‘benign inflation overshoot’ versus ‘stagflation’) and the severity of the impact that the Ukraine/Russia conflict will have on supply chains and the global economic system.

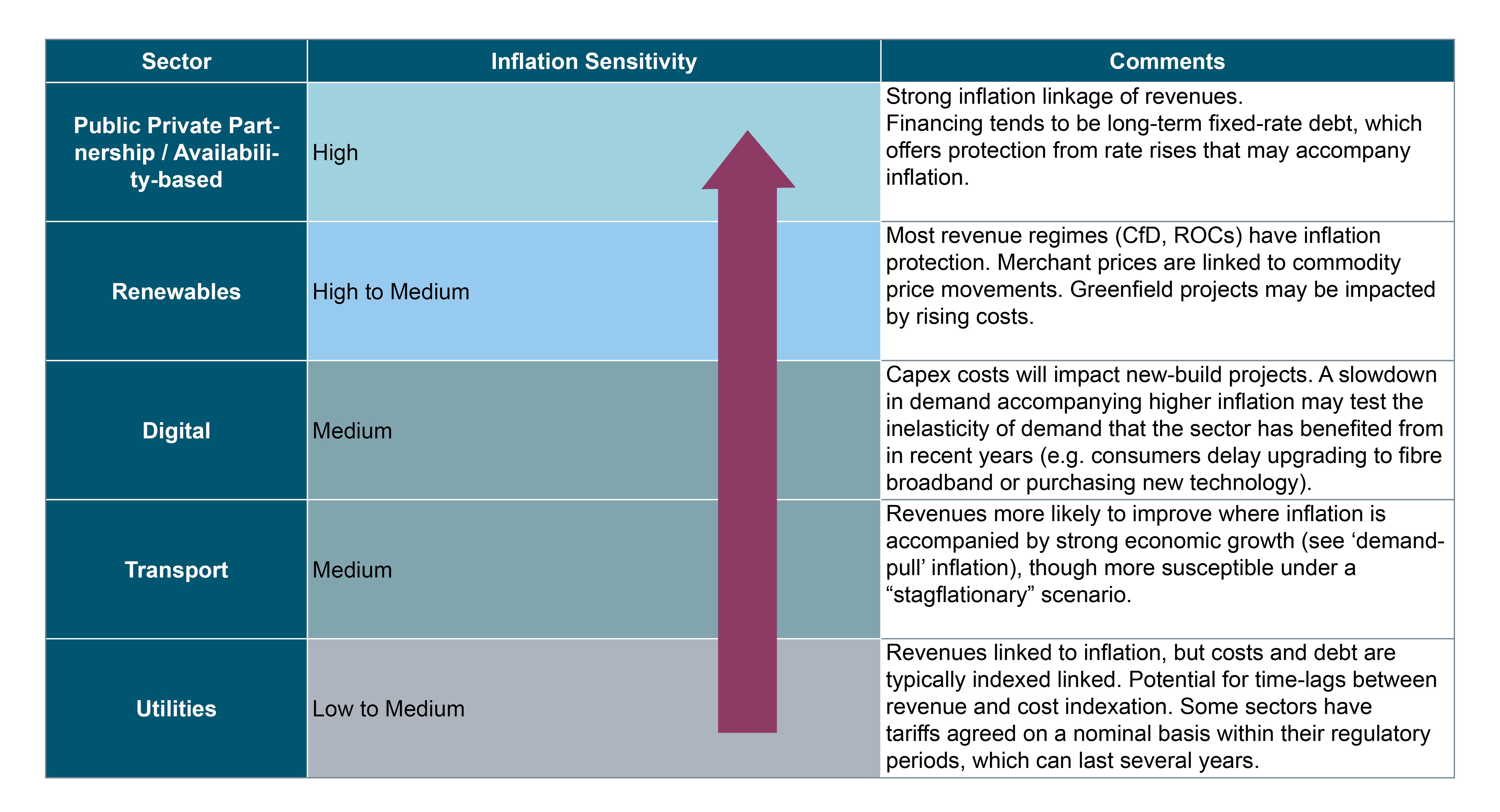

The received wisdom in the investment industry is that infrastructure should provide strong inflation protection, especially in sectors where contracts are subject to annual indexation, where essential service providers have pricing power and where operating costs are limited. Figure 1 summarises inflation linkage across the key infrastructure sub-sectors. However, when evaluating the level of inflation linkage of manager portfolios, what is set out in theory does not always hold true in practice.

Figure 1: Infrastructure sectors ranked by typical inflation sensitivity (a simplified view)

Source: bfinance.

Assessing inflation sensitivity: five factors to consider

Factors 1 and 2: Type of inflation and type of revenue model

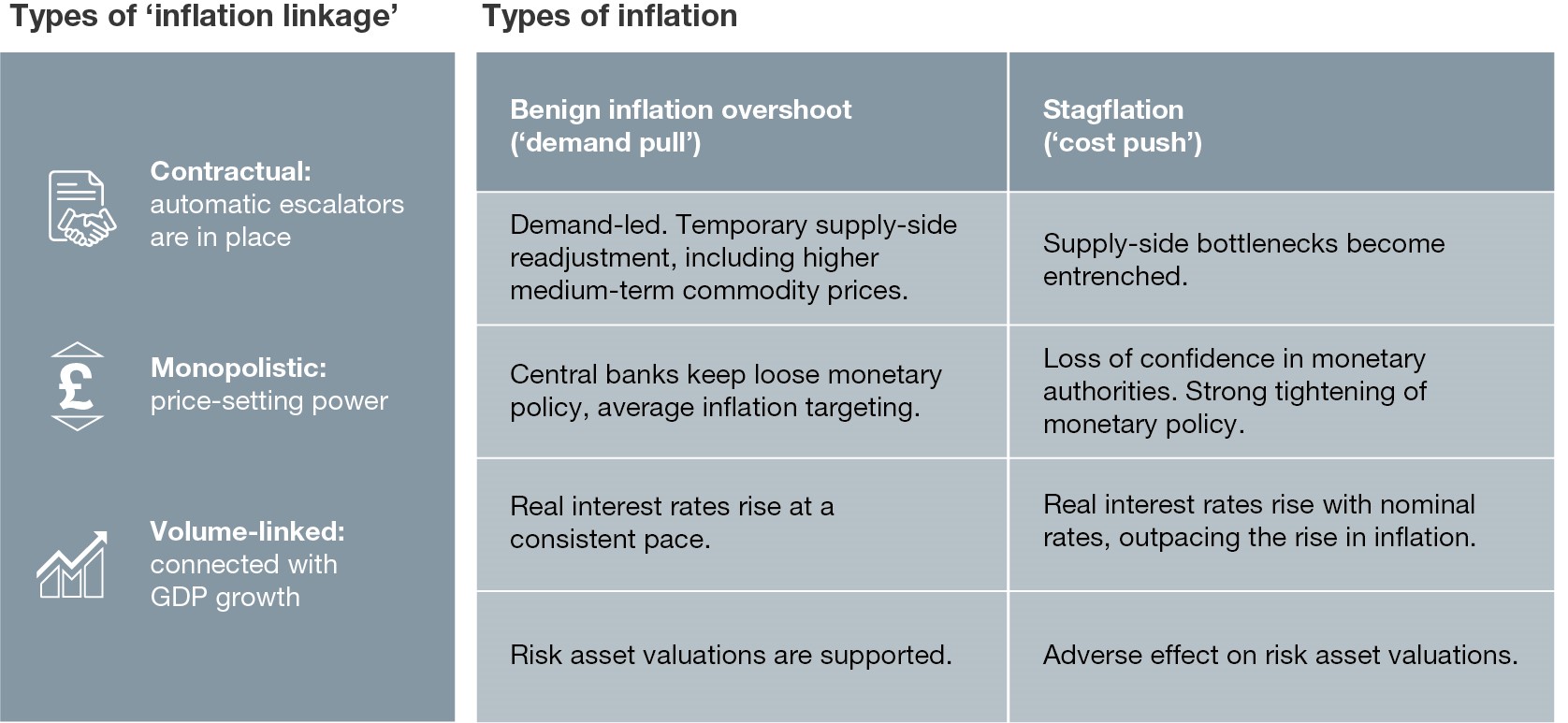

An infrastructure asset’s revenue model may be more or less sensitive to inflation. Yet, importantly, that sensitivity will also depend on the type of inflation that is taking place. For example, infrastructure with a ‘volume linked’ revenue model—a toll road, for instance—will typically make more money in a ‘demand pull’ inflation scenario, where inflation is accompanied by strong economic growth that supports consumer demand. This may break down in a ‘cost push’ inflation scenario where economic growth is weak. Conversely, assets with long-dated, contractual, index-linked revenues should benefit irrespective of inflation type. Investors should make sure that managers are not basing inflation assertions on overly benign inflationary scenarios.

Figure 2: Different types of ‘inflation linkage’ in revenue model (left); different types of inflation (right)

Source: bfinance.

Factor 3: Costs and supply chains

Just as not all revenue drivers are equal, the same is true of costs. From raw materials, construction and labour costs to operating and maintenance, all infrastructure assets require expenses that may surge in inflationary conditions. Railway companies for example, according to S&P, typically spend 4%–8% of their total operating expenditure on energy. Construction-related cost pressures could alter the financial viability of new-build projects versus ‘upgrade’ projects that require less capital expenditure.

As well as rising costs, inflation can also be associated with supply chain difficulties and could lead to heightened counterparty risk. In the past year, for instance, manufacturers of wind turbines have been particularly vulnerable to interrupted supply chains and surging freight costs; projects have been delayed due to the late arrival of components, which in turn has triggered financial penalties for turbine manufacturers.

Factor 4: Financing arrangements

Where inflation leads, interest rate rises (often) follow. Although core assets are often highly levered, they are typically financed with long-term fixed-rate debt and therefore resilient to rising-rate scenarios. That being said, expectations for higher interest rates over the long term can still affect the valuations of those assets. Value-add and opportunistic assets, while generally less highly levered, tend to be financed with shorter-term debt and are therefore often more exposed to interest rate risk.

Factor 5: Discount rate assumptions

With infrastructure investments typically valued under a discounted cash flow approach, interest rates form a key component of discount rates applied to future cash flow projections. Where managers have been prudent in calculating long-term risk-free rates, they will have built an initial buffer into the discount rates, so that rising base rates don’t have an immediate impact on valuations. However, there are inherent incentives to for asset managers to use lower rates than may be prudent—the lower the discount rate, the higher the valuation of the asset. In the case of open-ended infrastructure strategies, performance fees have often been charged on net asset value (NAV) estimates.

Interpreting information at the fund level

Among infrastructure funds, we see extremely wide variation in the proportions of revenues that managers claim should be linked to inflation and the projected impact of inflation on fund level performance. A few illustrative examples from a recent manager research are shown below to illustrate how practitioners are framing their inflation-sensitivity claims.

Figure 3: How managers show the potential impact of inflation on their portfolios – anonymised examples of metrics and explanations

Source: bfinance.

This type of analysis is based on subjective assumptions and should be viewed with caution. As well as scrutinising each of the five factors noted above (1. inflation type used in modelling, 2. revenue model, 3. costs/supply chains, 4. financing arrangements, 5. discount rates), it can be helpful to look at how assets have performed during recent quarters to see the real-time impact of inflation to date.

When seeking inflation sensitivity, avoid assumptions

When it comes to infrastructure and inflation, it is crucial to avoid generalisations. Inflation doesn’t occur in isolation, has different forms and often takes time to ‘wash through’ an economy. Meanwhile, every infrastructure asset and project is structured differently. Core assets will probably be better placed to withstand inflationary dynamics, but there are plenty of variables in play.

Investors should seek rigorous analysis of current and prospective infrastructure strategies in order to gain a more robust understanding of exposure to inflation. In addition, strong diversification—across sectors, business models, investment vehicles and maturities—is generally favourable in periods of uncertainty.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.