English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Mathias Neidert

Managing Director, Head of Public Markets

The long-running hunt for yield rolls on into an increasingly volatile 2020, with yields on safer fixed income now at or close to five-year lows. Risk-aware investors are seeking to diversify the sources of return in their more aggressive fixed income investments, in order to mitigate potential losses without sacrificing much-needed income.

Fixed income sectors receiving interest lately include structured credits, Asian bonds and short-dated high yield bonds.

2019 was a banner year for highly-rated fixed income (US Investment Grade Credit +14.8%, marginally ahead of US High Yield) as well as stocks (Global Equities +27.7%). Investment grade bonds also saw strong active manager performance, with 67% of US IGC managers and 80% of those in Europe beating their respective benchmarks. The firm’s fixed income manager selection activity for much of 2018 and 2019 was dominated by classic benchmark-oriented investment grade strategies.

Yet the year also saw yields on more conservative bonds squeezed to five-year lows, reinforced by the Q1 flight to safety. Hunting for yield remains a necessary priority. Late-2019 saw a pick-up in conversations around more aggressive fixed income segments, as well as illiquid private credit strategies like direct lending, real estate debt and infrastructure debt.

Yet the shape of today’s “yield hunting” is somewhat different. Investors are increasingly uncomfortable with heavy concentration in high yield debt (itself heavily US-concentrated) – a sector where compensation for risk is often debated. Indeed, coronavirus has driven US high yield spreads back to levels not seen since end-2018. Pension funds and other asset owners are exploring ways to diversify the sources of yield within fixed income.

Sectors receiving strong interest lately include:

- Structured credits such as CLOs, which claim to offer three times the spread of a corporate bond in the same rating category (not a statement to be taken at face value, of course).

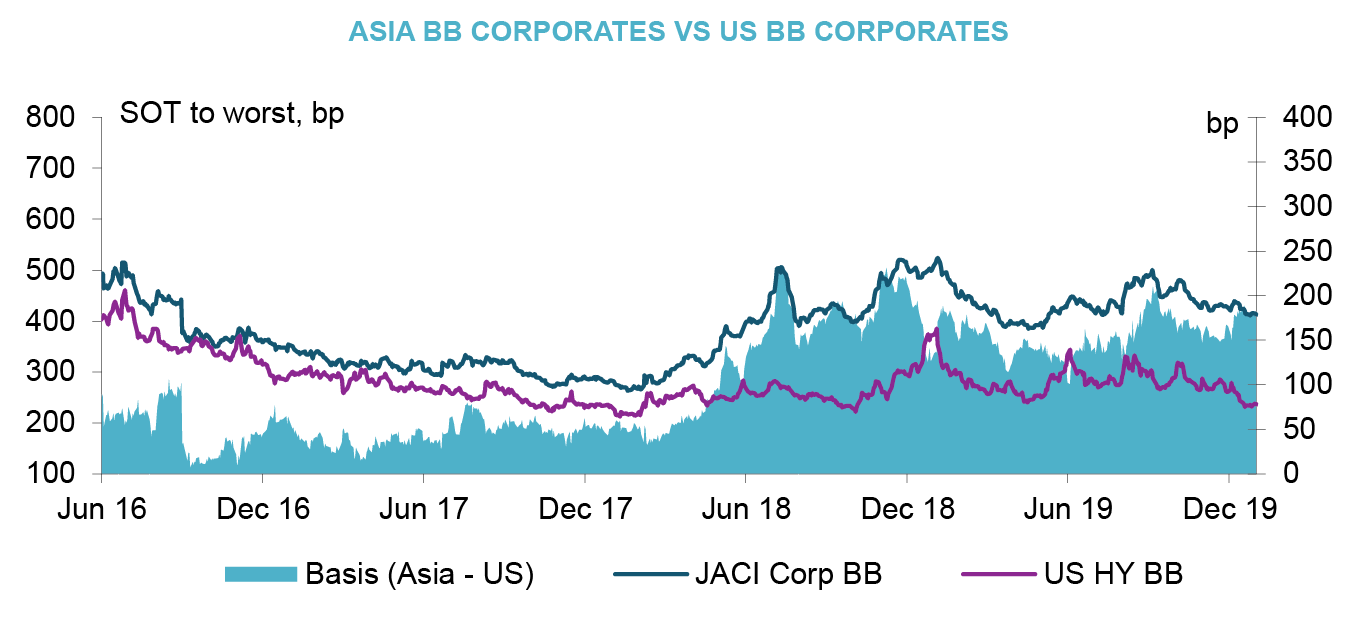

- Asian bonds, including Asian High Yield - a segment that has so far been dominated by local investors. BB bonds here offer a pick-up of nearly 200bps vs US corporate bonds of the same rating: the gap is particularly large now, from a historical perspective.

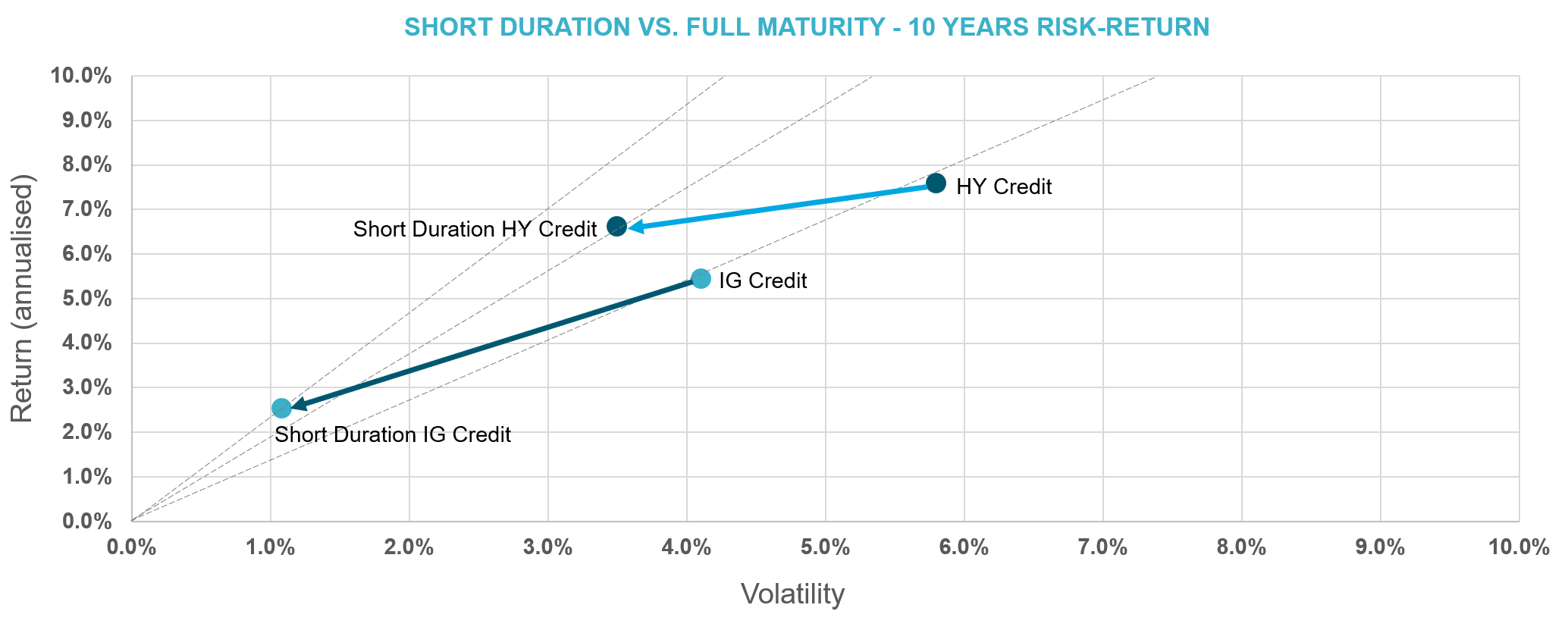

- Short-dated high yield bonds, which offer slightly lower returns than high yield but substantially less volatility, leading to better Sharpe ratios. These securities are less reactive to market fluctuations and changes in interest rates.

Meanwhile, there is still some demand for senior secured loans (syndicated loans), although client appetite for this space peaked in 2015-17. These are currently trading at a higher spread than bonds for the same rating level – an anomaly considering their seniority and security.

Finally, the factor investing theme continues to evolve within fixed income. The credibility of this sector – a late-developer compared to equities, due to the greater data and implementation challenges – has increased substantially in the last couple of years, with more than 65 strategies now available. (Contact

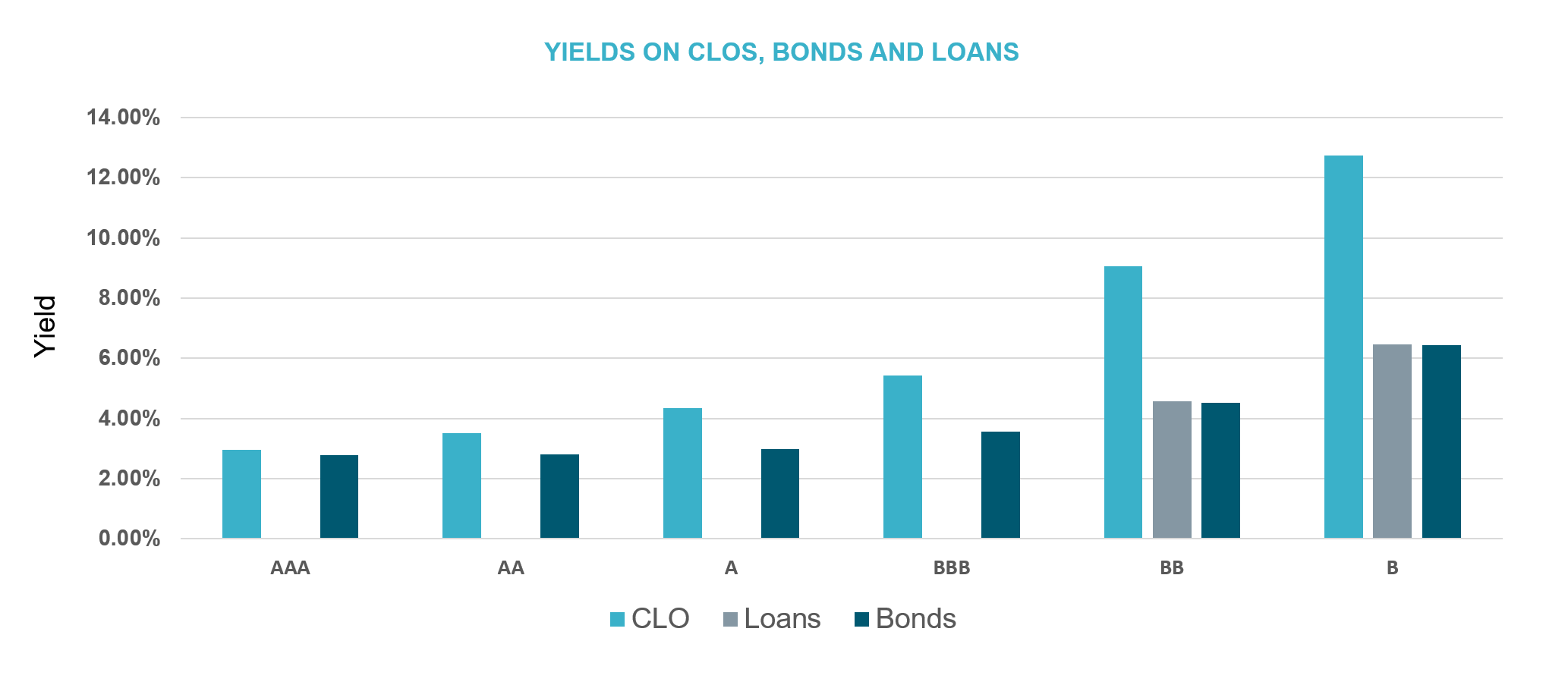

CLOs and structured credit

Marketed as an ‘investment grade’ asset class with a ‘high yield’ return profile, CLOs are still very far from being a staple for mainstream institutional investors. Yet they do offer compelling yields relative to corporate credit and leveraged loans, with spreads up to three times higher versus bonds of the same rating. For the same duration, BBB CLOs yield as much as High Yield Bonds while the A tranches match senior loans. The asset class also offers some diversification from mainstream fixed income: US BBB CLOs have a 0.55 correlation with US High Yield.

Source: JP Morgan

Marketed as an ‘investment grade’ asset class with a ‘high yield’ return profile, CLOs are still very far from being a staple for mainstream institutional investors. Yet they do offer compelling yields relative to corporate credit and leveraged loans, with spreads up to three times higher versus bonds of the same rating. For the same duration, BBB CLOs yield as much as High Yield Bonds while the A tranches match senior loans. The asset class also offers some diversification from mainstream fixed income: US BBB CLOs have a 0.55 correlation with US High Yield.

(Related Reading: MBS and Securitised Credit Sector in Brief - a previous research note which focused primarily on the more conservative side of this asset class.)

Short duration high yields bonds have delivered 40% less volatility than the overall market while giving away only 15% of the return.

Asian credit

Asian High Yield bonds have historically traded at a discount against US bonds of a similar credit rating. This gap has been particularly wide by historical standards over the past 18 months: at the end of December 2019 the spread on BB bonds was 415 bps in Asia vs 236bps in the US – a differential of nearly 200bps. For B-rated bonds, the spread was 761bps in Asia and 418bps in US. The recent rise in US spreads has narrowed the BB gap to around 100bps, but this is still considerably wider than the ten-year average (20bps).

Source: JP Morgan

Meanwhile, fundamentals have been improving: high yield issuers in Asia have been deleveraging significantly over the last few years (3.7x in H1 2019 versus 4.8x in 2016), while interest coverage has also been improving.

This market, which remains predominantly in the hands of local entities, is still generally overlooked by international investors, contributing to the persistence of a premium. Approximately 80% of issuance goes to Asian buyers, with the remainder going to the US and Europe. About one fifth is purchased by end-investors (insurance, pension) while the bulk is held by asset managers.

Risks need to be handled with care. In terms of composition, approximately 40% of Asian high yield issuers are in the Chinese real estate sector (vs 9% of the broad Asian bond index), while China issuers in total make up 54% of the high yield market. It’s critical that the asset class should be staffed by an Asian specialist.

Short-duration high yield

Short-duration bonds provide lower price volatility and less sensitivity to interest rate changes than conventional high yield. Historically, short duration HY bonds have experienced only 60% of the drawdown of the HY market more broadly, often with quicker time-to-recovery. The low volatility is, in part, the result of price inertia stemming from the lack of liquidity when bonds come closer to maturity.

Source: bfinance, Bloomberg. Indices: Barclays US Corp IG, Barclays US Corp 1-3yr, ICE BofAML US Cash Pay High Yield, ICE BofAML 1-3 Year US Cash Pay High Yield

While reduced duration is also associated with reduced volatility in the investment grade space, the return sacrifice is much less marked in high yield (as illustrated by the chart). Over the past ten years, short duration high yield bonds have delivered 40% less volatility than the overall market while giving away only c.15% of the return. Yet in investment grade, short-duration bonds reduced volatility by 70% but at the cost of c.50% less return.

Currently the spread on 1-3yr HY bonds is 4.13%, 95bps higher than on HY bonds with maturities of 3-5 years. However, spreads are fuelled by CCC-rated bonds: a prudent investment strategy would position a short-duration portfolio primarily in the B-BB segment, with select BBB bonds to reduce the risk profile without substantially cutting returns, for overall yields of around 3-6%.

Conclusion: beyond the hunt for yield

While investors are exploring a wider range of fixed income sub-sectors, there is minimal desire to increase risk. Instead, the focus lies on more intelligent use of the existing risk budget to diversify the sources of yield and improve resilience. The turmoil of 2020 has, if anything, reinforced the importance of a well-diversified risk profile.

Want more information? Contact

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.