English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Anna Morrison

Managing Director, Private Markets

Kathryn Saklatvala

Senior Director, Head of Investment Content

GP Staking – a Private Equity strategy characterised by investments in alternative asset managers and an unusual yield-generative profile – is currently drawing outsized coverage in industry press. Funds dedicated to this sector are also targeting an outsized capital raise: we note fifteen vehicles now seeking more than US$30 billion, following US$17 billion of fundraising through 2022-3.

Momentum is evidently being supported by industry surveys: The Private Equity International LP Perspectives 2024 Study, for example, revealed that 49% of respondents have either invested in GP Stakes funds or intend to do so, up from 36% the prior year.

Yet this specialist niche also presents some distinctive questions for prospective investors. Does the recent decline in fundraising across private markets create challenges for those seeking to pitch an industry growth story for GP Stakes, or should a more difficult period be viewed as a source of opportunity? Will stakes be used to develop and grow businesses or temporarily plug cashflow shortages? Are commonly expressed concerns about exits in this sector “overblown” (as described by a Houlihan Lokey MD in this May 2024 article) or substantive?

Below, bfinance’s Anna Morrison discusses the GP Staking landscape and draws insights from recent fund manager research.

Q: Firstly, for those of us unfamiliar with ‘GP Stakes’ investing, alternative investment managers look like the types of firms that Private Equity generally avoids: very talent-heavy, light on IP/inventory/real assets, a sector with quite low barriers to entry, and so on. What is specifically attractive or different about this type of PE investing?

Absolutely, when you take an equity stake in an alternative investment manager you’re typically not expecting to get those very large multiples that you could be looking for in some other sectors (though it’s worth remembering that strong multiples are feasible, particularly where the company has high recurring revenues). And, with minority stakes being the ‘norm,’ investors in GP Stakes are not in a position to press for major changes in these businesses.

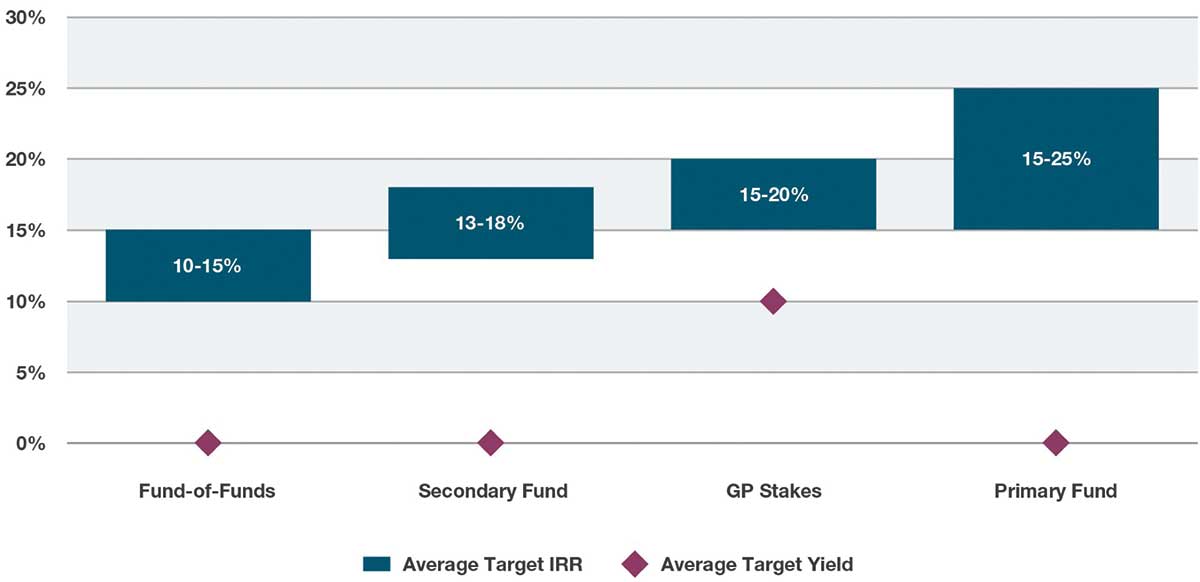

However, GP stakes investors can obtain something that is very unusual in the private equity world, as illustrated in the chart below: strong yields, typically around 8-12%, or broadly in line with senior secured private credit. These are explicitly contracted for and backed by the firms’ management fee revenues. In other words, GP Stakes investing is not a high-growth play: it’s a yield play with a potential growth upside (those involved in the sector often describe that yield component as “downside protection”). This provides a rather unique—and diversifying—return profile within a private equity portfolio. Investors can also think about the way in which those yields result in a softer J-curve – a characteristic also offered by secondaries funds (albeit for a different reason).

Yield in focus: GP Stakes funds versus other Private Equity sectors

Source: bfinance, based on 2023-2024 manager research

Meanwhile, although these should not be thought of as high-growth investments per se, GP Stakes do represent a way for investors to tap into a growth story: the expansion of private market investment management as an industry. This has been a major theme of the ‘post-GFC’ era, and one to which asset owners have themselves contributed via steadily rising allocations to private markets. Indeed, major asset owner surveys continue to confirm that these allocations are still rising, although the pace of those increases may have softened (a point mirrored by the recent slowdown in fundraising).

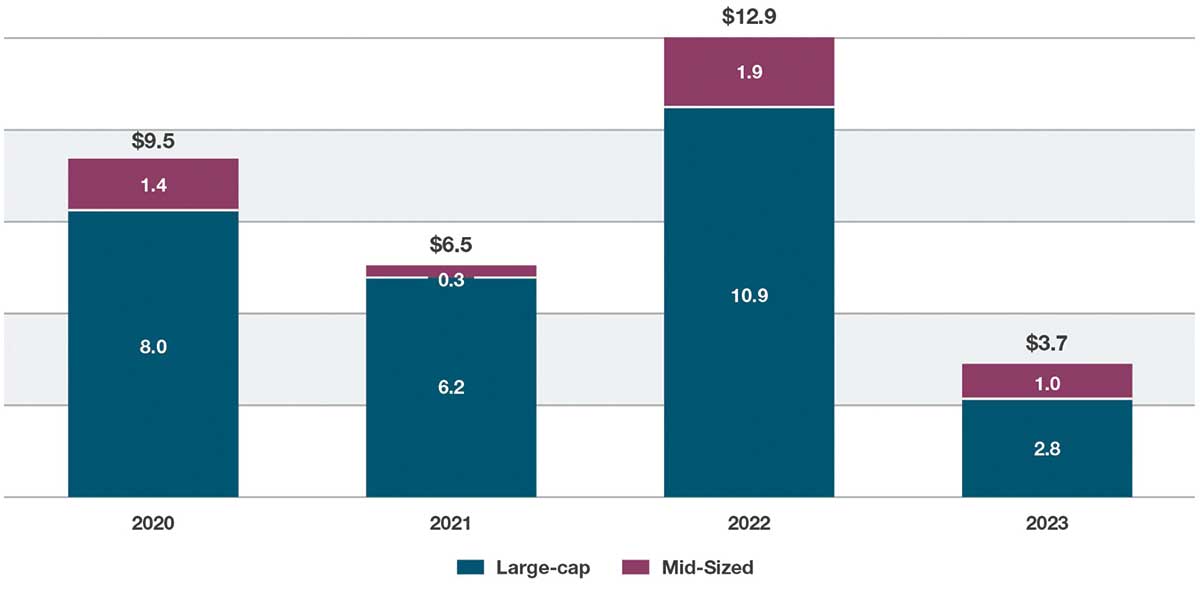

It’s also helpful that there are not too many managers targeting this sector: it is something of a specialist niche. Dedicated GP Stakes strategies dominate deal activity, although non-dedicated funds do sometimes invest in GP Stakes (see Permira’s investment in AltamarCAM in 2023, for example). As such, competition for deals is less heated than we’ve seen in certain mainstream private equity sectors where a lot of dry powder has been (and remains to be) deployed. Specifically, a relatively modest US$33 billion has been raised by 15 dedicated GP Staking funds over the past four years combined (see chart below) – an average of US$8 billion per year. 2023 represented less than US$4 billion of that figure as a weaker Private Equity fundraising environment encouraged a flight to familiarity.

Specialist sector: Capital raised by 15 dedicated GP Staking funds 2020-2023

Source: Investcorp, bfinance, data from 15 dedicated GP Stakes funds

Q: For quite a few years, the ‘GP Stakes’ investment case involved a private markets sector in rapid expansion mode, with fundraising (as you mention) increasing dramatically during the 2010s. But fundraising has now markedly slowed down. We see various firms are under pressure – raising less than they expected and taking longer to raise funds. Does this make GP Stakes investing less attractive?

This is an interesting point. But, in my view, the recent pressures for private markets managers may in fact create an exceptional opportunity for GP Stakes investors, as long as they have the ability to select well-positioned managers and underwrite them through ongoing market cycles.

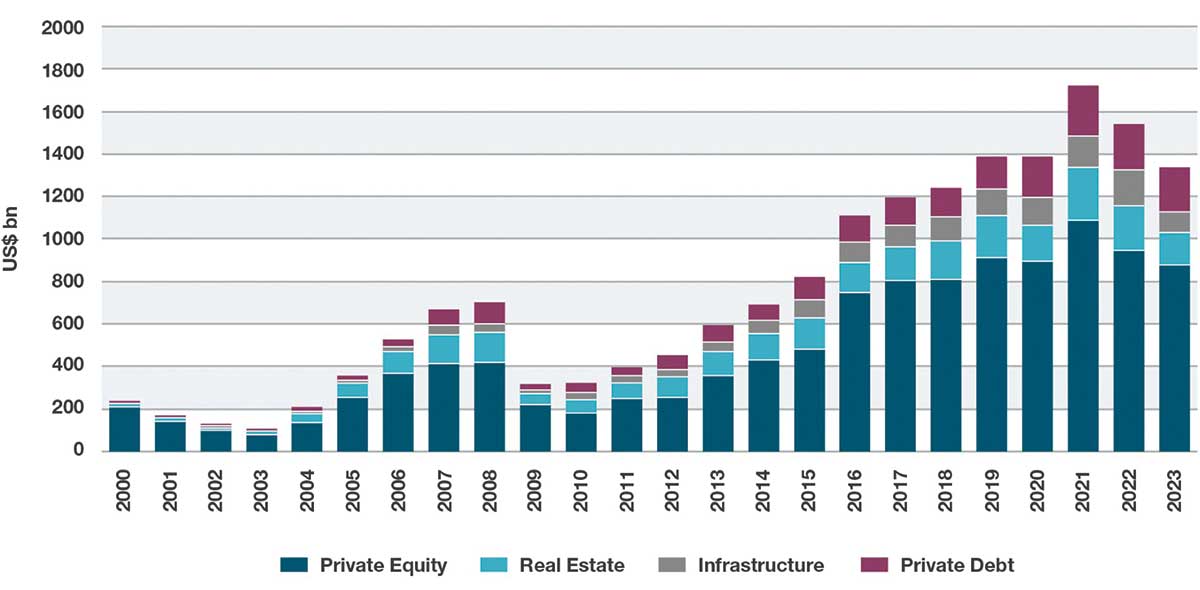

The decline in fundraising (below) has put firms in the industry under some strain, depending on their circumstances. This is particularly true for smaller and mid-sized firms (GP Stakes investors typically target mid-sized managers). And of course we were already seeing stresses on asset managers’ cashflows, even before fundraising softened, due to a general decline/deferral in exits over the past few years.

The recent pressures for private markets managers may in fact create an exceptional opportunity for GP Stakes investorsA number of alternative investment managers are finding these conditions challenging: we anticipate some upheaval, corporate change and consolidation. The winners, however, will be able to boost market share and ultimately benefit from the investment industry’s long-term structural shift in favour of private markets. A cash injection from a GP Stake can give firepower that contributes to success: the capital can help the GP to retain its talent, develop new fundraising channels (very important as the industry’s client base evolves), and make the necessary GP commitments in their own funds.

Capital raised by closed-end Private Markets funds 2000-2023

Source: Preqin

On principle, market participants know that the best time to invest in a sector is probably not when it’s at peak frothiness, when a rising tide might lift all boats for a little while; investors can often get better terms when companies are in greater need of cash. But selectivity is of huge importance.

Q: As discussed, there is evidently demand for capital injections among private market asset managers – not just stemming from the decline in fundraising, as you noted, but also from the decline/change in ‘exit’ activity over the past few years. How can GP Stakes investors be confident that they’re getting a great investment opportunity – not just temporarily plugging a cashflow problem?

We’ve absolutely seen a lot of different ways in which private equity firms have maintained good cashflows to meet spending requirements, despite those sorts of difficulties. We’ve seen a huge surge in GP-led secondaries (as discussed in this Secondaries Sector-in-Brief report from 2023), which support liquidity. As part of this story, we then saw a very significant rise in the use of dedicated continuation funds (one form of GP secondary transaction) – essentially enabling an asset manager to hold onto an asset for longer. More recently we have seen an increase in NAV financing, whereby a private market asset manager can take out an additional line of borrowing backed by the value of the assets in their vehicles.

One interesting aspect to think about is the way in which the new investment will be used by the GPOne interesting aspect to think about is the way in which the investments will be used. Our recent analysis has indicated that, while managers’ strategies differ greatly, a very sizeable proportion of GP Stake capital is often used to provide the GP’s own investment in its fund (private markets funds typically require a minimum % commitment from the asset manager themselves to support alignment of interest).

The side effect is that only a modest amount of the capital raised is being directed towards spending that will enhance capabilities, coverage, team, or other ‘operational improvements.’ This is not, in and of itself, a red flag: using a capital injection to pay for GP commitments allows the firm to launch new vehicles, or raise a larger vehicle than they might otherwise have been able to deliver, supporting strong ongoing management fee revenues. Yet the GP Stakes investor—who, after all, will hold only a minority stake, which places them in a relatively passive position—must have conviction that the asset manager has a strong trajectory of development in key areas.

Q: One concern that investors have historically raised regarding GP Stakes is the perceived challenge of obtaining exits. How has this subject evolved recently?

It’s definitely very important to think about exits here. If you think back to an earlier wave of GP Stakes investing in hedge funds through 2004-7, we certainly saw the impact of difficulties exiting such stakes after the financial crisis hit the hedge fund sector.

One important feature of the newer vehicles in this sector is that they are often adopting a somewhat more conventional (exit-oriented) mindset than their predecessors who commonly had a ‘perpetual’ approach. In other words, the GP Stakes funds raised a few years back would not have been setting expectations around closes and the timeframes of exits. The newer funds are different: some (more aggressive) strategies have an approach that is quite close to typical private equity; others lie somewhere in-between the two (somewhat perpetually-oriented but with additional—as yet untested—provisions intended to offer better liquidity to investors).

We’ve seen a good list of exits recently from stakes acquired in the 2010s, but the number of transactions is generally quite low. Stakes can be sold to another Private Equity investor, though (as discussed) the group of funds focused on this space is relatively contained. There are ‘strategic’ buyers, such as asset managers looking to purchase alternative investment managers to expand their own capabilities. IPOs are a possibility, though they’re often unappealing to firms of this type. Management buy-backs have become somewhat trickier now that debt is more expensive. The minority status of a GP Stakes investor affects the degree of influence that they can exercise when it comes to exit.

Exiting is not, however, a challenge confined to the world of GP Stakes: this is an issue affecting much of the private equity sector these days.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.