English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Chris Stevens

Senior Director, Diversifying Strategies

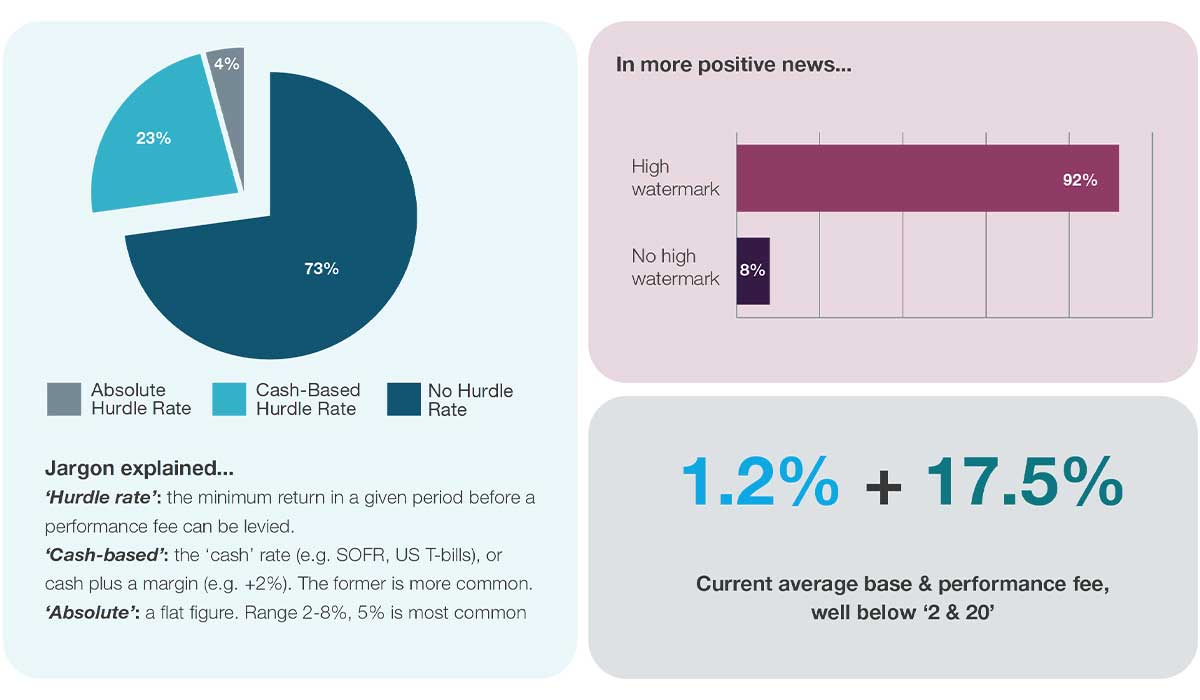

Although two years have now passed since the Federal Reserve started rapidly hiking interest rates, the likelihood that your hedge fund manager will have a ‘hurdle rate’ for their performance fees has not changed. Only a quarter of hedge funds, by our count, have such a threshold in place and the practice does not yet show signs of becoming more widespread, even though the risk-free rate has now exceeded 4% for well over a year.

Investors are honing in on the hurdle rate debate. We’ve even seen cases where hedge fund managers have lost out on mandates specifically because of unwillingness to introduce hurdle rates. This, in our view, is likely to become an increasingly common stance among investors as the months pass. Yet, according to bfinance manager search data, only 27% of hedge funds currently use a hurdle rate and this figure does not appear to have increased by any statistically significant margin.

Only 27% of hedge funds have a hurdle rate

Source: bfinance, 231 fee proposals reviewed

Since most hurdle rates are cash-based, managers that do use them have seen the threshold for earning performance fees rising materially along with interest rates. As such, what used to be an essentially academic distinction in net returns for the two types of fee structure during the ‘ZIRP’ era has now become a very meaningful difference. An investor who deployed $50 million to a hedge fund that delivered 6% gross over a year (a $3 million return) with average fees of 1.2%+17.5% would be paying over $1 million in fees that year with no hurdle versus around $670k in fees with a 4% hurdle. The former sees the manager taking home around 34% of the return; the latter 22% (quite close to the “one-to-five principle” espoused by investors like AP1’s Majdi Chammas).

Managers’ lack of movement on this subject is mirrored on the private markets side, where hurdle rates—while far more commonplace than in the hedge fund sphere—have similarly remained static since 2022. It’s also worth remembering that certain asset classes (such as private credit) saw hurdle rates fall during the ‘ZIRP’ era, leaving asset managers in an even more advantageous position now that rates have risen.

So, one might ask: what is going on? A rapid change could not have been expected, of course. New fee structures require changes to offering documents and other legal matters. Initially there was some doubt about whether rates would even remain elevated for the foreseeable future, with a narrative of ‘transitory inflation’ proving quite popular among economic commentators. (Similarly, perhaps, few in 2008 would have predicted that rates for the next 12 years would average just 0.5%, after averaging 4% for the pre-GFC decade!) Yet why has the picture still not changed?

We typically see three styles of argument given by managers for not using a hurdle rate. But how valid are these justifications?

- "It is a low beta strategy” / “our returns are entirely alpha” / “there isn’t an appropriate hurdle rate for us given our strategy.”

- "Our fees are already low” / “we have a high watermark.”

- "This fee profile has been in place since inception” / “The fees are appropriate to a full range of market environments.”

This argument is problematic on both a philosophical and a practical level. Philosophically, the risk-free rate does matter and should matter. Investors need to justify—for their stakeholders, for their trustees, for their underlying members, for their own professionalism—how they’re spending fees. The fact that assets could alternatively be parked in extremely low-risk securities or cash is always relevant.

It is quite hard to come up with a mainstream hedge fund strategy which does not in some way benefit from higher rates.

The second, more practical objection to this point is the fact is that better risk-free rates do directly benefit hedge fund portfolios in many cases. Most hedge fund strategies are implemented in such a way that they typically have a large part of their portfolios invested in cash instruments. Managed futures strategies, for instance, typically put up just 10-20% of their portfolio as margin to the futures positions, with the rest of the portfolio in ‘unencumbered cash’ – invested in T-bills or other short-term instruments that earn interest. Equity long/short strategies are similarly cash-rich, with the sale of short positions funding long positions and the rest of the portfolio sitting in cash.

Even for strategies that typically hold less cash, such as merger arbitrage, the arbitrage spreads that they seek to capture will increase with rising rates. In fact, it is quite hard to come up with a mainstream hedge fund strategy which does not in some way benefit from higher rates. This makes the lack of cash hurdles (at a minimum) across so much of the industry even harder to justify.

Interestingly, we actually find that the managers that use hurdle rates also tend to be more investor-friendly in other parts of their fee structure. For hedge funds with a hurdle rate, we observe the average base fee at 1.02%. For hedge funds without a hurdle rate, the average base fee is more than 25bps higher (1.28%). Average performance fees for both groups are similar, at 17.5% and 17.6% respectively. In other words, investors in funds that lack hurdle rates are not, we would conclude, seeing the disadvantage being offset by lower fees.

High watermarks are, on a positive note, very prevalent across the sector: 92% of hedge funds use them. The 8% that do not use high watermarks do appear somewhat more likely to have a hurdle rate in place (42% versus the average 27%), but it is still a minority practice.

In practice, we have seen significant disparity in the extent to which different hedge funds have been subjected to fee pressure.

In practice, we have seen significant disparity in the extent to which different hedge funds have been subjected to fee pressure. On one side of the spectrum we find managers that have had to become more aligned and in tune with investors’ wishes in order to maintain fundraising. On the other side we find a cohort that has been so popular among investors that they’ve been able to maintain very manager-favourable terms.

In reality, fee structures and sizes certainly do evolve with changing market environments and fundraising conditions. Indeed, we saw a visible decline in average hedge fund fees in the decade following the Global Financial Crisis due in large part to the disappointment that many investors encountered at that time. The world has now shifted again, and fees may well shift with it.

There may even be a psychological subtext at play here, especially for industry personnel whose careers pre-date the GFC. It is true that hedge fund terms did shift meaningfully in investors’ favour after 2008—an adjustment which was not seen, or at least certainly not to the same extent, in private markets. In addition, zero or near-zero interest rates did make it harder to deliver returns (and thus earn performance fees). Rightly or wrongly, some senior hedge fund figures will see the return of a world with 4%-plus interest rates as an opportunity to reverse those tipped scales a little, for the time being at least.

Bearing in mind the volume of investor interest and concern on the subject of hurdle rates, we would now encourage hedge funds to consider instituting a threshold if they have not already done so. Performance fees of 15-20% are still high relative to other asset classes and this fee is supposed to be fair compensation for skill-based alpha generation. Returns under the risk-free rate should not qualify, in our view at least, for this treatment. Over time, we expect investors to increasingly resist paying ‘money for nothing’ – and a refusal to change with the times could ultimately leave some managers in dire straits.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.