English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Toby Goodworth

Managing Director, Head of Risk & Diversifying Strategies

Investors' costs have never been more vigilantly scrutinised than they are today. New bfinance data published in investment Management Fees: New Savings, New Challenges (May 2017) reveals falling fees in several sectors, especially where providers have been under pressure from cheaper competitors or the investment landscape has evolved.

Fund of Hedge Funds have suffered the most significant reductions, with fund manager fees falling by 20% globally and nearly 30% in Europe. The median quoted fee has dropped from 100bps to 80 since the previous bfinance fee study in January 2015. In Europe, where investors fell out of love with the sector more severely than their counterparts elsewhere, the average is now down to 69bps.

On top of the management fees illustrated here, we currently see underlying hedge fund fees averaging 1.4%+18%. The range is considerable, from under 1+10% on the low end to above 3%+30% at the top.

FoHFs have sought to regain investors' favour following the post-GFC rout.

This challenge has been made more complicated by the evolution of Alternative Risk Premia products and the growing popularity of various multi asset or diversified growth strategies.

The past couple of years have also seen the emergence of a new breed of player in the FoHF space: Funds-of-Sub-Advisors. These are being offered by larger asset managers with the ability and infrastructure to run managed account platforms. The providers establish arrangements with relevant hedge fund managers such that the latter share trading instructions which the provider then implements themselves, offering one flat fee to the investor (read Sector in Brief: Funds of Sub-Advisors).

Such products can be seen to represent another interesting response to demands for lower pricing, although there is a lack of transparency on how the economics are shared between the provider and the manager partners.

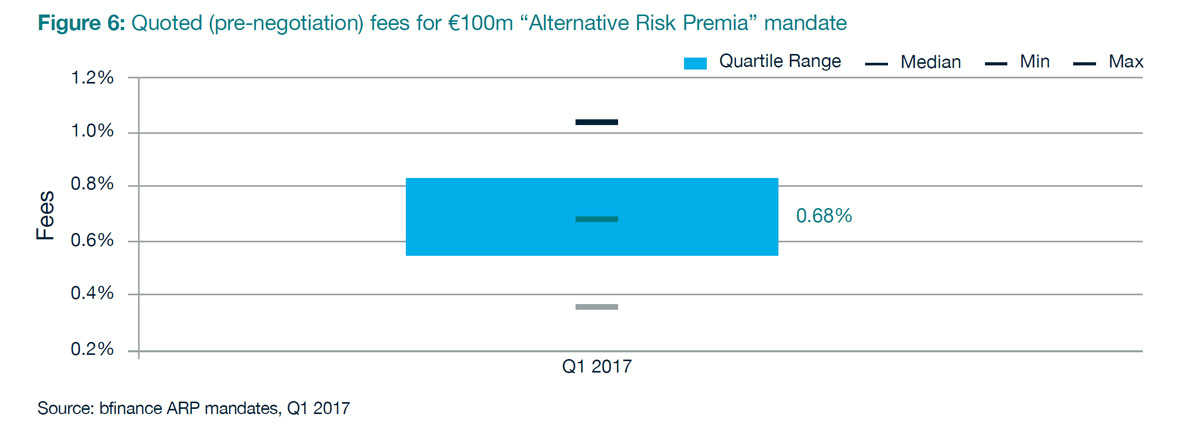

Meanwhile, for comparison, we have also observed a modest reduction in fees within the increasingly popular Alternative Risk Premia (or “Alternative Beta”) sector.

While the November 2016 bfinance white paper on this asset class (The Changing World of Alternative Beta) showed fees with a range of 30-150bps and a median of 74-80, the most recent proprietary data from Q1 2017 (Figure 6) indicates a new range of 35-103bps and a median of 68.

Much of this reduction can be attributed to the involvement of new providers, who are offering what tends to be quite competitive pricing as well as early bird discounts of up to 50%. Over 2016 the number of ARP providers increased by more than 30%, producing significant sample variation. At the same time, a handful of more established managers have either reduced their fees or closed their doors to new investors. That being said, we would be hesitant about calling a trend just yet.

Amid these intriguing competitive market dynamics, one thing is clear: cost is a key battle ground, and one where FoHF managers are evidently prepared to fight.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.