English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

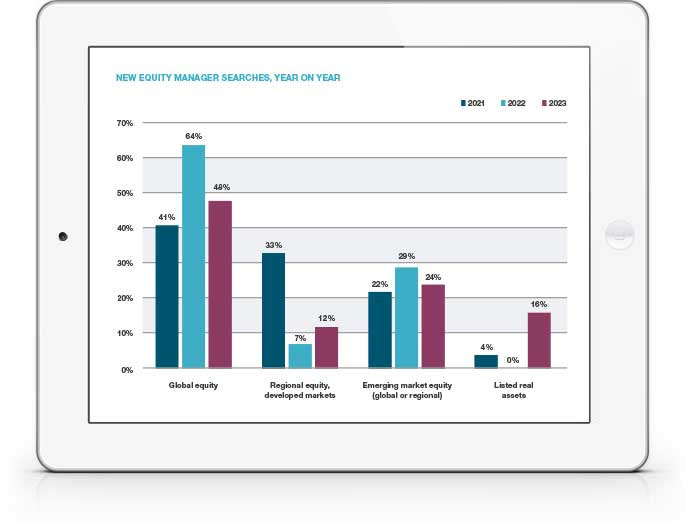

Asset manager performance through to the end of 2023 provided some interesting takeaways for investors, with many equity managers struggling to handle the runaway ‘Magnificent Seven’ and US Investment Grade Credit managers hit by the off-benchmark exposures that often help them to beat their benchmark. Meanwhile, more directional hedge funds strategies (e.g. Equity Long/Short) rode resurgent equity markets while their more ‘diversifying’ counterparts such as Global Macro and CTAs—the stars of 2022—delivered muted results.

Among bfinance clients, deployment towards private market asset classes was a little muted versus the previous year, with subdued appetite for real estate manager searches only picking up a little at year end. More surprisingly, new infrastructure mandates have also decreased despite healthy returns data. That being said, demand for corporate private debt has proven strong and there was a particularly large increase in mandates for ‘natural capital’ (timberland, nature-based solutions and more) from investors seeking real asset exposure and, in many cases, carbon offsetting. The recent Endowment and Foundation Investment Survey suggests widespread intentions for increasing private market exposure over the next 18 months, due in part to current underweight positions (e.g. 52% underweight private equity).

Although demand for ‘diversifying strategies’ (liquid alternatives) represented just 10% of all new manager searches in the year to end-2023, underlying this figure was a significant rebound in hedge fund search activity with managed futures proving particularly appealing. Currency overlays were also in higher demand in a changing macroeconomic picture.

Overall risk sentiment improved towards the end of Q4, thanks in large part to the actions of the FOMC and the Fed: the bfinance Risk Aversion Index, which considers a range of relevant variables, indicated a modest but notable decrease. Equities, Listed Real Assets (REITs and Listed Infrastructure) and Fixed Income all enjoyed a positive run and multi-asset managers—always mindful of FOMO—boosted their equity allocations towards year end. Yet the shadow of uncertainty looms large and the search for ‘all-weather’ resilience continues in investment portfolio design.

WHY DOWNLOAD?

Each quarter, bfinance publishes information on investor activity, key market trends and manager performance. A quarterly snapshot of the key developments within equity, fixed income and alternative investments, including analysis of which asset manager groups performed well and which didn't.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.