English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

The rise, fall and rise of active FX management: Volatile conditions and co-ordinated ultra-low interest rates undermined certain well established currency risk premia following the 2008 financial crisis. A closer look at carry, momentum, value and volatility 1995-2023.

Understanding active and passive currency hedging: Reviewing standalone active currency strategies, active FX overlays, dynamic FX hedging and passive hedging: conceptual differences, price points, instruments, drivers of return.

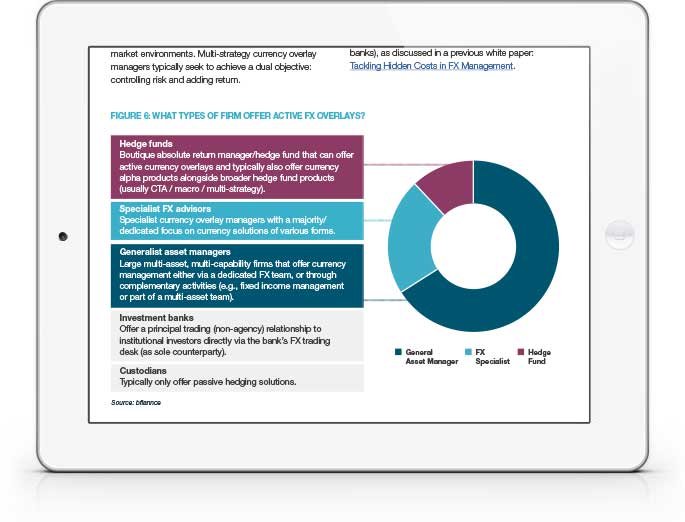

Implementing an active overlay: More than 50 firms are able to deliver active FX overlays. How can investors select the right parameters for their overlay, identify potential partners and assess their suitability? The highly customised nature of overlays makes past performance assessment complex; not all managers are able to present suitably granular attribution.

WHY DOWNLOAD?

The approach to FX hedging is one of the most important overall strategic investment decisions for any institution that wishes to invest a significant proportion of the portfolio outside of its base currency. Decisions around whether to hedge, how much to hedge and how actively to adjust those hedges are challenging, not least because a strategically sensible long-term approach may not produce visible benefits in all time periods.

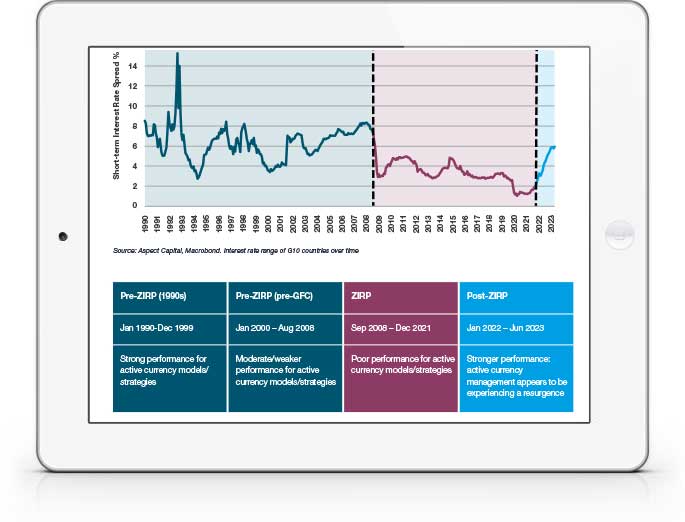

In this respect, we now sit at an interesting juncture. Active currency managers struggled to generate desirable returns for much of the post-GFC decade, due in part to a lack of variation between the (rock bottom) interest rate policies of different developed markets. The 2022-3 phase, however, has seen the G10 countries diverging in terms of their growth rates, inflation rates and interest rate policies. This, in turn, has ushered in a period of improved performance from currency managers of various shades.

Once again, we see investors able to control or meaningfully reduce portfolio-level risk through active FX management, and potentially add an uncorrelated driver of returns to portfolios. As such, many are now re-evaluating strategic hedge ratios—fully hedged, fully unhedged, or somewhere in-between—and reconsidering whether those hedges should be implemented passively or actively. For practical application, this report features an overview of the current universe of active FX overlay providers (asset managers, banks and others) and issues to watch out for during manager selection.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.