English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)

bfinance insight from:

Kathryn Saklatvala

Senior Director, Head of Investment Content

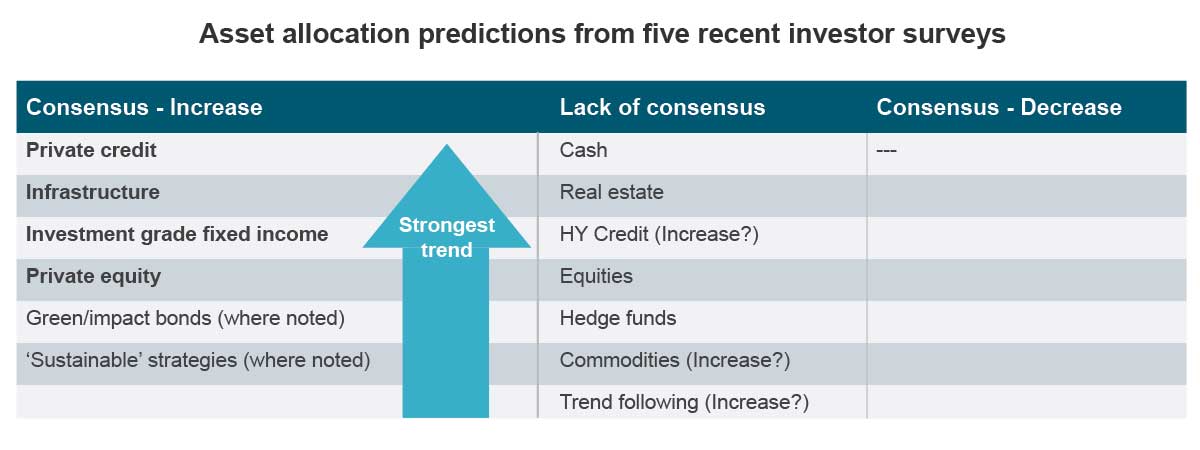

Credible asset owner surveys can be a useful source of insight for both investors and the asset managers/advisers that serve them. Their headline findings often tend to focus on expected changes to asset allocation, with researchers seeking to call out trends. Interestingly, while the latest studies reveal areas of agreement (such as rising allocations to Private Credit, Infrastructure and Investment Grade Bonds), they showcase a notable lack of consensus on trends for Cash, Real Estate and Equity exposures.

Below, we review the five surveys from late 2023 and early 2024 that we believe provide the some of the best barometers—so far—on investors’ asset allocation expectations.

All five cover a wide variety of subjects and are run by entities with broad asset class coverage themselves, since we find that both thematic studies (e.g. labelled ‘Private Markets’) and surveys from firms with narrow specialism tend to produce a skew towards the area of focus/specialism.

Four of them cover a diverse asset owner base including pension funds, endowments, foundations, insurers and more: the EQuilibrium Global Institutional Investor Survey from Nuveen (with CoreData), the CIO Sentiment Survey from Top1000Funds and Casey Quirk, Mercer’s latest Large Asset Owner Barometer and Natixis’ 2024 Institutional Outlook Survey. The fifth, GSAM’s Global Insurance Survey, focuses purely on the insurer segment.

Investors are not at ‘peak private markets’ yet

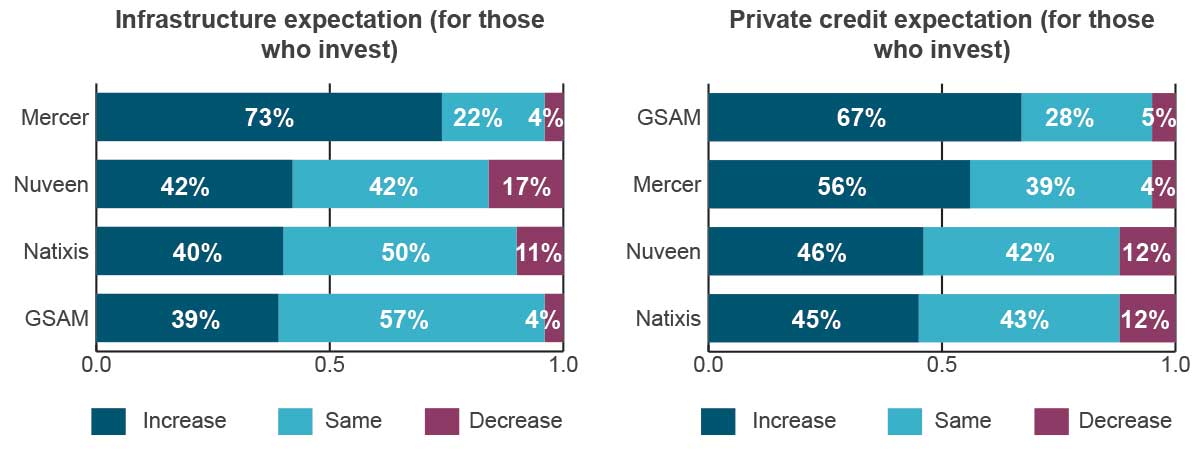

It’s certainly possible that we have reached (or, more accurately, passed) the period of peak private markets fundraising: many have commented on the declining inflows that are affecting the industry in a myriad of ways (e.g. Open-end Infrastructure Withstands Investor Cooldown). However, we do not appear to have reached peak allocations. All of these studies predict increasing exposure to Private Credit and Infrastructure, with an evident positive trend also visible in Private Equity (5/5 surveys show an overall expected increase in all three sectors).

Some—but not all—studies show a ‘do not invest’ category. Percentages have been recalculated to exclude this category where applicable, to allow for comparison. Studies varied in terms of time frame for the expectation (12-24 months).

That being said, several reports observe that the multi-year pro-illiquid trend appears to be proceeding at a gentler pace. “There is a softening compared to last year’s surge, where 72% of respondents planned on increasing their private markets allocations [versus 55% this year],” the Nuveen authors explain. “Asset owner demand for alternatives has cooled slightly,” the Top1000Funds/Casey Quirk report similarly notes, “but remains above demand for other asset classes, with particular interest in real assets and private credit.” Here, the authors pointed to concerns in private equity (“particularly valuation mark downs and questions about the IPO market”) and private credit, which has been supported by a wave of de-banking (“questions about whether the risk parameters are compelling enough to offset the large amount of money flowing into this space”).

Positive trend to Investment Grade Bonds

Although the overall trend on fixed income is hard to call—with different studies drawing different conclusions—there does appear to be reasonable consensus on a continuation of rising allocations to Investment Grade Fixed Income. Natixis’ survey, for example, has 47% of investors anticipating a rise (16% decreasing); GSAM calculates 37% increasing Investment Grade Corporate Bonds (9% decreasing); Nuveen indicates a more sizeable 72% figure increasing Investment Grade Corporate Bond exposure with 61% increasing Investment Grade Government Bonds.

Appetite for Investment Grade Fixed Income appetite (corporate, government or both) is also suggested by strong signals that investors are planning to increase duration in their portfolios (more highly rated bonds have longer average duration than their lower-rated counterparts). For example, 50% of Nuveen’s respondent base indicated that they’ll increase duration in 2024 and only 19% expect to decrease, whereas the previous year’s survey had a far less clear-cut result (39% increasing duration versus 28% decreasing). The GSAM survey, now in its 13th year, highlighted that the proportion of respondents planning to increase duration (42%) was at its highest level ever recorded. “Last year marked a fixed income renaissance as insurers renewed their interest in the asset class,” states the GSAM survey.

No ‘ESG backlash’ in allocation intentions

“Despite headlines around an ESG backlash, large asset owners are set to increase their allocations to sustainable investment strategies significantly,” say the authors of the Mercer report. Half of their respondents (admittedly one of the groups among the five studies cited here) intend to increase their allocations to sustainability strategies and, importantly, no respondents signalled a decrease (29% remaining the same, 11% not invested). This study also shows a positive trend on climate matters at strategic level: 55% have set climate transition studies (70% of those with >$20 billion in assets) and a further 37% intend to do so within the next 24 months.

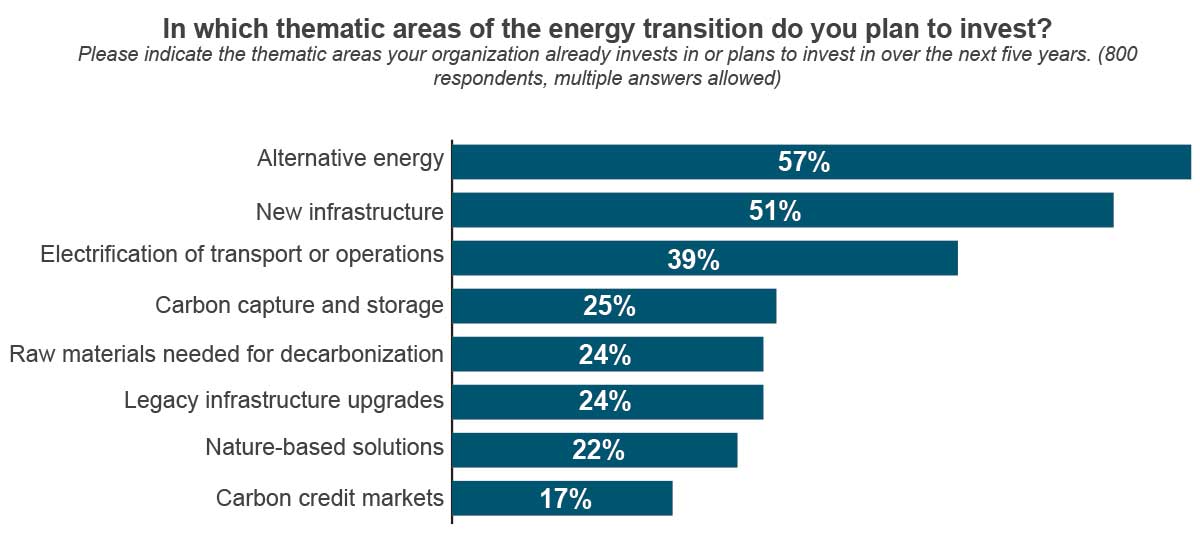

Most of the studies did not specifically ask about Green or Impact Bond allocations, but one that did—GSAM’s insurer study—noted a relatively strong positive trend (25% increasing, 3% decreasing). Nuveen’s study, meanwhile, asked investors: “in which thematic areas of the energy transition do you plan to invest?”

Source: Equilibrium Global Institutional Investor Survey, Nuveen (CoreData)

Mixed signals on cash, equities, real estate

In previous years, we have often seen some consistency on asset classes where investors expect to decrease allocations. For example, the 2010s saw migration from low-yielding Fixed Income, often to fund greater exposure to illiquid strategies that could deliver stable yields/income. Similarly, cuts to Real Estate allocations were very evident during the peak of the COVID-19 pandemic.

This year, however, there is a remarkable lack of consensus. Most agree that Cash allocations are at significantly higher levels than usual, but some predict decreases (including GSAM) while others do not. Nuveen notes a predicted overall increase in Cash allocations, even though 55% of respondents are already holding more cash than they were two years ago and “ready to take advantage of opportunities when they emerge.”

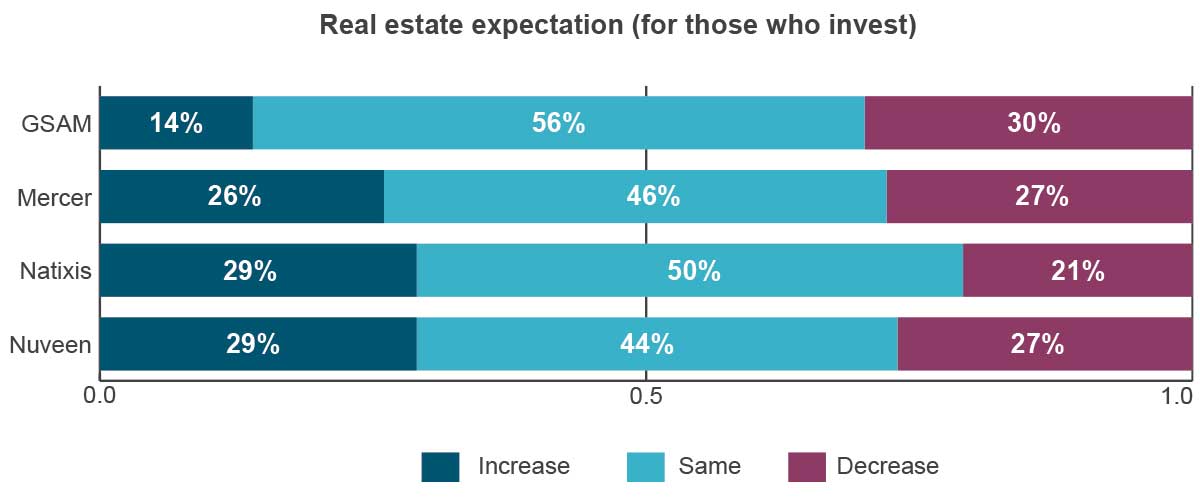

Real Estate responses, meanwhile, present an interesting set of contra-indicating signals. Very substantial groups of respondents to various surveys are either decreasing or increasing allocations in this space, but neither side presents a clear-cut majority. GSAM and Top1000Funds/Casey Quirk show the balance in favour of decreasing allocations; Mercer and Nuveen show the two groups broadly equal; Natixis has the increasing cohort outnumbering the ‘decreasing’ group.

Some—but not all—studies show a ‘do not invest’ category. Percentages have been recalculated to exclude this category where applicable, to allow for comparison. Studies varied in terms of time frame for the expectation (12-24 months).

For Equities, the picture is also mixed. Natixis’ study finds equity “increasers” marginally outnumbering “decreasers” (and a more clear-cut increase for Emerging Market Equity allocations). Nuveen and Mercer, on the other hand, appear to have the “decreasers” in the majority (with a particularly visible decline in UK equity allocations). The Mercer authors opined that some – “but not all” – of the equity reduction trend is driven by pension funds de-risking now that higher interest rates have improved their funding ratios.

Interestingly, the analysis from Top1000Funds and Casey Quirk predicts increasing allocations to ‘Passive Equity’ and decreasing allocations to ‘Active Equity’ (a conclusion that, it should be noted, is contradicted by other studies). This shift, according to the authors, is primarily driven by “concerns about over-valuation” – though they do not explore why an investor who is worried about rich valuations would be more likely to favour a passive approach.

Interested in investor sentiment?

The biennial bfinance Global Asset Owner Survey is taking place later this year. Asset allocation strategy will be on the radar but so will costs, governance, valuations, views on external asset managers’ outcomes, impact, macro risks and any other issues that are high on the priority list for our investor clients and contacts. If you would like to recommend a question for inclusion in this study, or for use in one of our ad hoc Asset Owner Surveys (which take place on an ongoing basis, as illustrated below), please do not hesitate to contact us:

A selection of ad hoc surveys:

- Asset Owner Survey: Investors’ Costs and Fees

- Endowment & Foundation Investment Survey

- Available now on a confidential/exclusive basis only: ESG Costs in Asset Management (please do enquire if you would like to see results and did not participate).

- ESG Asset Owner Survey

- Insurer Investment Survey

- Wealth Manager Investment Survey

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.