English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)

On April 22nd, more than 300 investors around the globe joined the bfinance research team (virtually) for a session dissecting manager performance through the crisis so far.

Twenty key takeaways are listed below. The full 45-minute session can be accessed here.

Equities

1. Extremely wide performance dispersion among active global equity managers, with a 42% gulf between best and worst in Q1.

2. Quality-focused global equity managers beat their benchmark by an average of 7.6%, further evidencing their ability to materially outperform in falling markets. The connection between quality and sustainability meant those managers with an ESG focus also fared well.

3. Value factors had a significant negative impact on relative returns, with value-focused equity managers underperforming benchmarks and their peers of different styles in all regions. Both value and growth managers have generally struggled in market downturns.

4. Emerging markets equity managers found it unusually difficult to beat the index. Quality was the only main factor delivering positive attribution and, with relatively few managers having a pure quality focus, the majority of managers underperformed.

5. Japanese equity managers struggled to beat their benchmark, with the prevalence of a value style and relatively high allocations to mid and small-cap stocks proving a headwind.

FIGURE 1: RELATIVE PERFORMANCE OF ACTIVE GLOBAL EQUITY MANAGERS BY STYLE, VERSUS MSCI WORLD INDEX (STYLE CLASSIFICATIONS ASSIGNED BY BFINANCE)

Fixed income

6. Investment grade credit managers were ill-prepared for the market correction. 2019 bfinance manager research showed IGC funds overweight BBB and with an additional 10% typically invested in high yield. Many who’d missed out on the 2019 rally due to conservatism had re-risked to catch up with peers. As such, only 32% of IGC managers in Europe beat the benchmark in Q1, as did 40% of US IGC managers (Figure 2).

Click Here to read “Will Fallen Angels Reveal Fixed Income’s Saints and Sinners?”

7. Conservative positioning in credit paid off … eventually. The initial sell-off hit higher-rated credit equally hard, due to investors selling more liquid assets (typically higher quality), but AAAs rebounded at month-end.

8. Two thirds of high yield managers outperformed benchmarks – unlike their IGC counterparts, most were conservatively positioned, and in particular underweight energy. Interestingly, the worst-affected group weren’t focused on value credit but on smaller (mid-market) issuers; larger deals benefited disproportionately from the record $7.1bn that flowed into US High Yield in late March (ETFs prove highly influential, yet again).

9. Absolute return bond funds lost 7.4% on average in Q1, similar to the amount lost by the IGC market, and better than the average active managers in other segments. These strategies are often promoted for capital protection. There was wide performance disparity (deciles -1% and -15%). A big source of success/failure was hedging: CDS are a poor hedge instrument in times of liquidity stress, while CDX and iTraxx remained tradeable; the best hedge was equity put options.

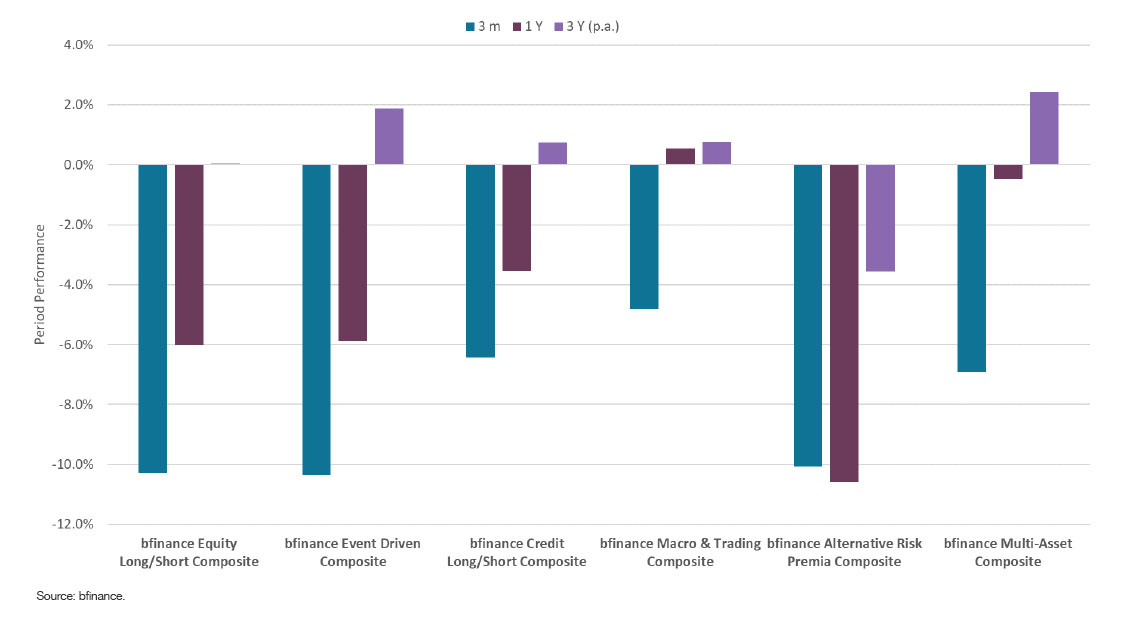

Liquid alternatives

10. In hedge funds and other liquid alternatives, outright positive monthly returns for Q1 were few and far between, except for explicit long volatility / tail risk protection strategies which largely did their job. Elsewhere, a “win” in March involved limiting losses to low single digits or better.

11. Pure trend-following was a bright spot: average returns for CTAs were 2-3% in March, with some higher vol strategies up close to 10%. Diversified CTAs and Systematic Macro gave flat-to-slight-negative returns, on average. Gains were mainly from fixed income, currencies and short positions on oil.

12. Other hedge fund results: the average Event Driven manager was down 12%, average Merger Arb fund down 9% thanks in large part to indiscriminate (and often dramatic) spread-widening, average Long/Short Equity manager down 9.5%, average Relative Value manager down 6.5%.

13. Alternative risk premia suffered its worst ever quarter, losing 6% on average with particular pain from Equity Value. “Academic” risk premia did better than “Practitioner” premia, while strategies incorporating Trend-following premia did substantially better than their peers.

14. Multi-Asset managers had a relatively robust quarter on average, with the GARS cohort acquitting themselves nicely (keeping March losses to low single digits).

FIGURE 3: PERFORMANCE OF BFINANCE LIQUID ALTERNATIVE COMPOSITES TO END-Q1

Private markets

15. It’s too early to gauge the impact of COVID-19 on private markets. Private asset classes can provide some resilience to GDP and inflation shocks, in part through lagged write-downs, but they can’t escape them. June and September valuations will be more indicative.

16. It is very likely that the next two years will be strong vintages for investing in Private Markets, but…

17. Expect serious challenges for cashflows and performance of assets acquired in 2017-19: disciplined managers will have been more prudent in deployment of capital during this period (focus on good quality markets and assets, less leverage, good terms).

18. True diversity within private markets will come into focus. All four private markets sub-sectors (private equity, private debt, real estate, infrastructure) include a wide range of strategy types and risk profiles – making more than 25 distinct categories in total – which will respond differently.

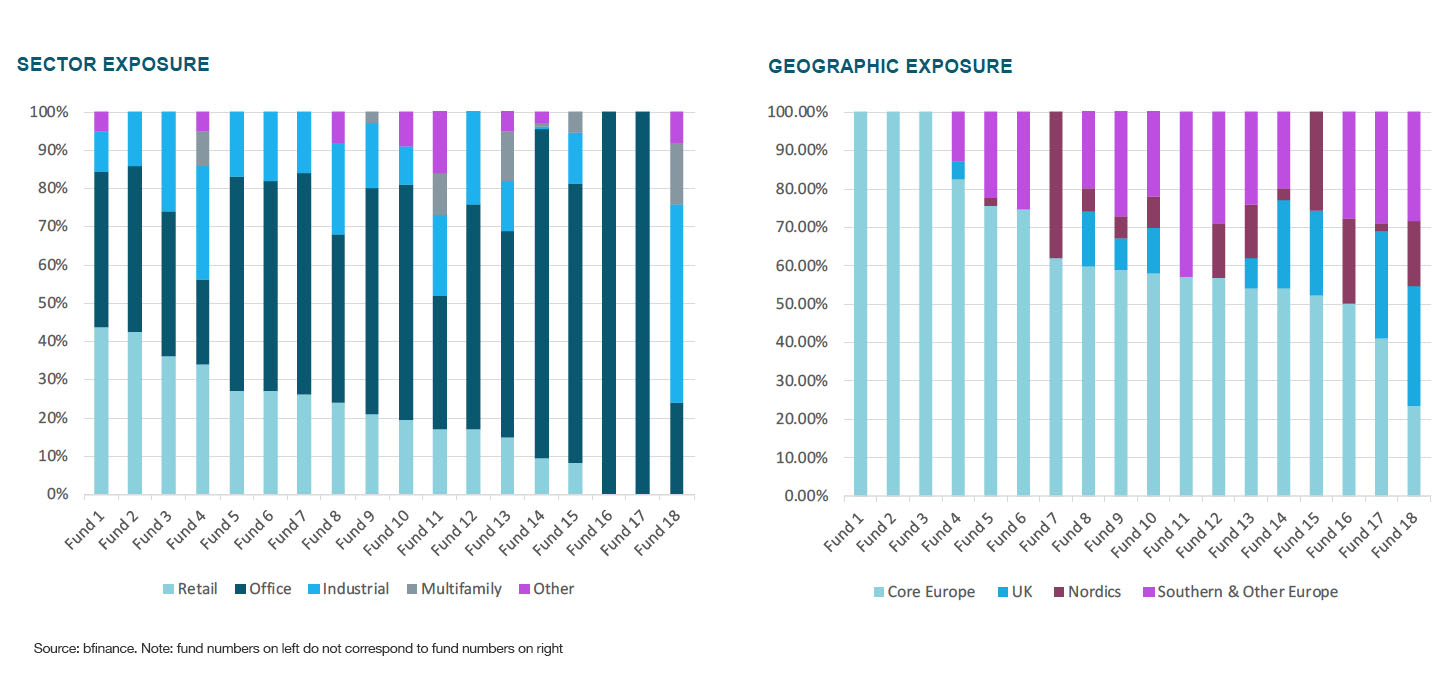

19. The crisis will also highlight the very substantial differences between managers in nominally similar private markets strategies (see Figure 4 for an example, with European Core Real Estate fund positioning at end-2019).

FIGURE 4: EUROPEAN CORE REAL ESTATE FUNDS AT END-2019, BY SECTOR AND GEOGRAPHY

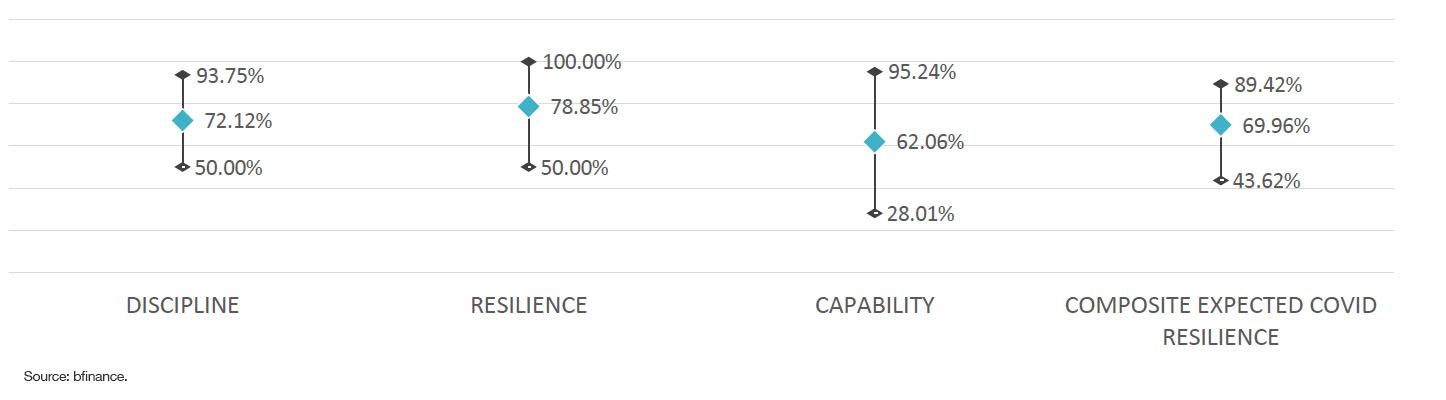

20. Which private markets managers are more resilient, disciplined and capable than others? Figure 5 shows the wide dispersion on “soft” factors among just 26 private debt managers assessed in a recent bfinance manager search (all 26 had already passed initial quantitative and qualitative screens, from a wider group of 106). We already observe private markets managers that scored weaker on “process” (part of “discipline”) showing up with increasing numbers of problematic positions. Coming months will show whether managers with higher scores for “capability” manage to reduce the number of problem positions that turn into losses.

FIGURE 5: EXPECTED COVID RESILIENCE FOR PRIVATE CREDIT MANAGERS

To contact any of the team with questions and comments, email

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.