English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)

bfinance insight from:

Chris Stevens

Director, Diversifying Strategies

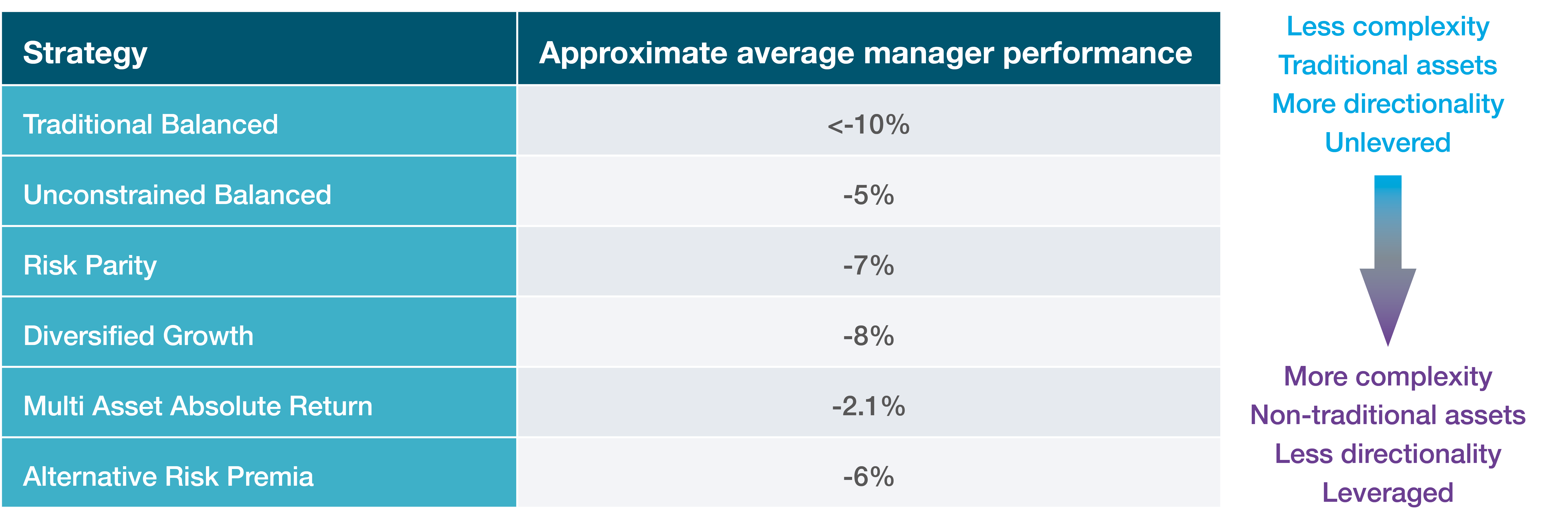

Institutions have increasingly turned to multi-asset strategies – now a diverse menu – for the promise of diversification and a more “all-weather” return profile. While most asset managers in this space lost money during an extremely testing first quarter, average declines were relatively modest and certain strategies delivered impressive capital preservation.

During a dismal period for anything that looked like a risky asset, it is unsurprising that the Multi-Asset sector (an extremely heterogeneous group, as illustrated by a previous article on the Seven Shades of Multi Asset) delivered negative performance – on average – in Q1.

Yet many of the losses shown in Figure 1 could be seen as rather modest in a quarter where the MSCI World lost more than a fifth of its value, Investment Grade Credit fell by 7%, almost all commodities were down, most Hedge Funds lost money and Absolute Return Fixed Income managers – often sought explicitly for their resilience – lost 7% as well. Indeed, with the exception of cash and high-quality government bonds, huge risk-off moves left few places to hide at the asset class level. There were also notable bright spots: the sometimes-maligned GARS cohort, for instance, provided impressive resilience with a remarkable average loss of barely over 2% in March.

FIGURE 1: AVERAGE RETURNS FOR MANAGERS IN MARCH 2020, BY MULTI-ASSET SUB-SECTOR

Source: bfinance. For an explanation of the categories, see the primer in this article.

Importantly, the quarter has illustrated the real diversity within the Multi Asset space, both between the categories shown in Figure 1 and within those groups. Manager dispersion was unusually wide in Q1. In many cases, a key driver of relative performance was the speed at which different managers measure risk, and therefore rebalance portfolios, given the extremely rapid increase in volatility across all asset classes. This particular crisis has been remarkable not just for the extent of market declines but the speed of those declines: in previous bear markets, it has taken an average of eight months for global stocks to lose 20%; in March it took just 16 days.

Understanding the numbers

In the long-only ‘Traditional Balanced’ space, losses have been driven almost entirely by the breakdown of the strategic allocation between equities and bonds. For reference, a global 60/40 portfolio (60% MSCI World / 40% JPM Global Government), delivered a return of c.-12% over the quarter, losing close to 8% in March. Almost any move away from this benchmark would generally have hurt managers’ returns: small cap underperformed large cap, non-US underperformed US, credit spreads widened, commodities fell heavily. It was a quarter that punished anyone who dared to diversify away from US large cap growth names (principally Tech) as their principal risk exposure.

Within what we call the ‘Unconstrained Balanced’ category (long-only, mainly invested in traditional asset classes, not anchored to a strategic benchmark), the managers that we see as bellwethers for the space fared relatively well. We observe that some of the most well-known managers had adopted a conservative, rather sceptical stance towards the post-GFC economic and market expansion which has now ended abruptly. This conservatism was generally beneficial in March, with managers' losses averaging c.5% and some firms even posting positive performance for the month as a result of options-based protective positions.

Results were broadly as expected from the ‘Diversified Growth’ sector; for a portfolio of growth assets there was little to no help from nominal asset class diversification and losses for the peer group were concentrated around the -8% mark for March. For those managers that lacked bond exposure or other protective positions, losses were typically worse than this average (low double digits).

Sometimes derided as levered bond portfolios, Risk Parity strategies broadly fared better than capital-allocation-based approaches due to their more impactful exposure to interest rates, although this was not enough to fully offset negative performance from equity, commodity exposure and credit (where used). Risk Parity strategies saw an interesting level of dispersion for a category which most would assume had greater homogeneity than some others shown here. At a c.10% target level of volatility, average performance for the quarter was c.-9% but with a range of -5% to -20%. Losses averaged c.7% for March. The better performers were those than had moved away from a classic implementation of the Risk Parity construct, preferring a higher level of dynamism in their processes through, for example, trend-following-based tactical overlays. The relative speed with which strategies measure risk (and therefore rebalance portfolios) will also have been a key driver: those that use shorter lookback windows and/or are more reactive would have cut exposures during the weeks of heaviest losses for risk assets.

The Absolute Return Multi-Asset sector fared best of all – largely to be expected, given that these strategies explicitly aim to avoid relying heavily on being long risk assets to drive returns. Nonetheless given the level of market turbulence across all asset classes, the sector delivered a decent level of capital preservation with an average performance for March of -2.1%. Since these strategies typically have a focus on relative value trades with low market directional risk, their performance is even more impressive when we consider that Relative Value hedge funds were down c.-6.5% on average according to HFRI data.

The Multi Asset pantheon also includes Alternative Risk Premia and certain hedge fund strategies, discussed at greater length in the recent Liquid Alternatives research update. ARP managers experienced their worst ever quarter, losing – on average – 6% in March, while most multi asset hedge fund strategies experienced losses average similar to those seen in the rest of the Multi Asset arena and performance dispersion was similarly wide, if not wider (particularly extremes were observed in Global Macro). In general, anyone with strong exposure to explicit long volatility strategies (pure trend-following) did well relative to peers.

Investors give mixed feedback

These intra-strategy and inter-strategy differences go some way to explaining the highly varied feedback from 260 investors (predominantly pension funds) who responded to a bfinance snap poll on March 20th: half of those that use multi-asset managers indicated that they were “somewhat satisfied” with their performance so far in Q1, with 35% “not satisfied” and 7% “very satisfied.” Of course, it should be noted that this survey preceded the market rebound at month-end.

SO FAR IN Q1, HOW DO YOU RATE THE PERFORMANCE OF MULTI ASSET STRATEGIES IN YOUR PORTFOLIO?

Source: bfinance, poll of 260 investors conducted on March 19-20th 2020

Overall, once results are digested, we believe that the performance during the first phase of the COVID-19 crisis will support ongoing investor demand for Multi Asset strategies – particularly the Absolute Return contingent. Rising appetite for this space has been a notable feature of investor activity through recent years.

Most importantly, that activity will be informed and influenced by richer information on performance, risk management, operations and processes as a result of this crisis. Investors, asset managers and consultants must now utilise contemporaneous empirical results to improve our understanding, rather than relying on previously assumed knowledge or past experience.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.