English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Kunal Chavda

Director, Public Markets

With large volumes of BBB credits either undergoing or set to undergo downgrades which knock them off the investment grade plinth, many investment grade bond managers are expecting “fallen angels” to be the main driver of performance through this downturn.

The post-GFC period has seen a massive expansion in the volume of BBB credit issuance. At the end of 2007, only 35% of the US corporate bond market was rated BBB, along with 18% of the European corporate bond market. At the end of 2019, those figures had risen to 50% and 49% respectively.

The increasing dominance of the BBB tranche is hardly surprising in a climate of low rates and shrinking spreads. Many corporates took advantage of the environment, seeing the opportunity to increase debt issuance while holding onto the coveted investment grade rating – albeit at the lower end of the spectrum. This has included a raft of share buy-backs, generally viewed to be the least value-accretive use of debt. Indeed, there are question marks hanging over whether all of them should have remained in this category as long as they did: ratings agencies have already been criticised for overly generous courtesy periods extended to companies that had, for example, taken on excessive levels of debt for the purpose of carrying out acquisitions.

Manager positioning

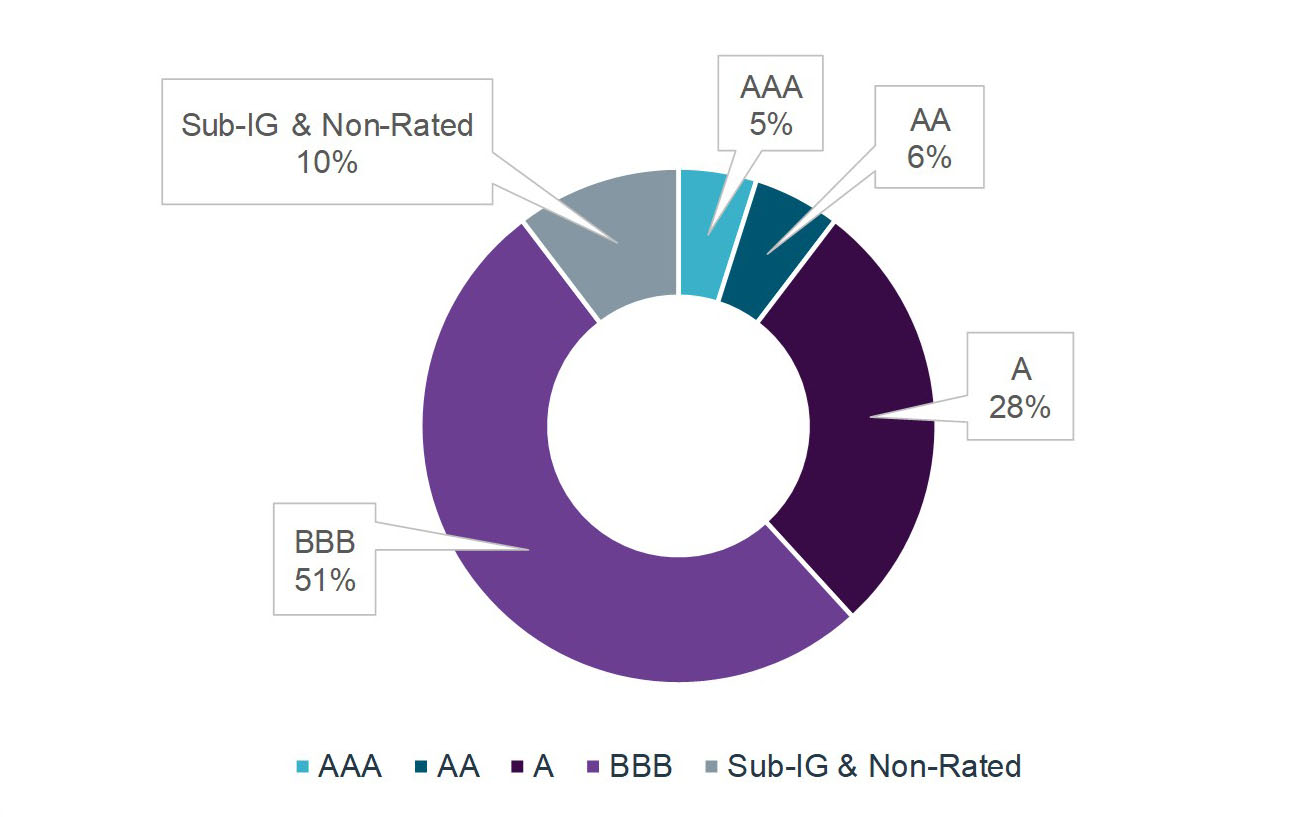

It is also unsurprising that investment grade credit (IGC) managers, like the IG market at large, substantially increased their credit risk exposure over the yield-starved decade that followed the GFC. In manager searches in 2019, bfinance found the average exposure of active investment grade credit managers to BBB-tier debt to be 51%, a little above benchmark. In addition, managers typically had an additional 10% invested in sub-investment grade and non-rated debt.

FIGURE 1: INVESTMENT GRADE CREDIT MANAGER PORTFOLIOS BY CREDIT RISK EXPOSURE, 2019

Source: bfinance, based on 76 fixed income managers assessed in 2019 for clients seeking Investment Grade Credit (excl. Absolute Return).

This 2019 average masks a broad range of approaches, with some managers holding as little as 35% in BBB credits while others had exposures of around 70%. In addition to the differences among benchmark-relative IGC managers, it’s also worth noting the substantial use of this segment by Absolute Return managers, who have embraced higher exposures to BBB credits from time to time.

So far, although reporting and analysis are still underway, it appears that active investment grade credit managers have tended to underperform their benchmarks (which have dropped by 6% in Europe and 4% in the US), with credit risk as a key factor.

Braced for impact

Downgrades from BBB to High Yield have already begun, with $100 billion in the US corporate bond market over March (though it should be noted that just over a third of this figure is represented by Ford). The worst-hit sectors are those most immediately affected by COVID-19 and the oil supply dispute: energy, entertainment and leisure, autos and consumer discretionary.

Anecdotally, asset managers are expecting 25-50% of all BBB debt to suffer some sort of negative watch move or downgrade

Ratings agencies are widely expected to react rapidly in downgrading troubled issuers, although preserving credibility on this point has been challenging: after 2008, they were criticised for being too gentle; in the 2015 oil crisis they were judged for being too harsh in downgrading energy-related firms indiscriminately. Anecdotally, asset managers are expecting a large portion of all BBB debt to suffer some sort of negative watch move or downgrade (e.g. BBB+ to BBB, or BBB to BBB-).

For fixed income managers, the hit lies not only in the decline in price that would usually precede a downgrade, but in the liquidity crunch as sellers rush to the same exits. Much depends on the capacity of the high yield market to swallow those downgrades: Europe is considerably more vulnerable in this respect, with a HY market four times smaller than its US counterpart while the BBB proportion is only 2.5 times smaller. (To put this in perspective, if 5% of European BBB paper were downgraded, the EU HY market would grow by 20%). That capacity will be highly influenced by whether the downgrades are accompanied by positive or negative flows to high yield bond funds. Current signs are positive: while late February and early March saw severe outflows, we subsequently witnessed record inflows (+$7.1 billion for the week ending April 1st, equivalent to more than 4% of all HY assets under management).

Avoiding forced selling, where possible, will help IGC investors to limit the damage

Avoiding forced selling, where possible, will help investment grade credit investors to limit the damage. Some market participants have more flexibility to wait than others. Passive funds are typically forced sellers, although some index providers delayed quarterly rebalancing until the end of April. Insurers with strict restrictions on holding only high-quality bond have to sell downgraded credits within short timeframes.

Active managers have more leeway than most around holding downgraded bonds, in part due to the tolerance for holding a certain portion of sub-investment grade debt, typically capped around the 5-10% mark. That allocation is used to retain downgraded positions which the manager wishes to hold to maturity, cultivate “rising stars” who are expected to move towards IG status, or – in this scenario – capitalise on fallen angel opportunities that trade at a discounted price. We have seen many managers clearing out their sub-investment grade exposures in March, where liquidity has permitted, in order to make room for the anticipated downgrades. Yet active managers will face difficulties if the sub-investment grade portion exceeds the tolerance level. If such limits are hard-coded into the fund prospectus or IMA, they could be become forced sellers or write to investors and the regulator about breaching parameters for a period of time due to inability to sell.

Re-underwriting the investment case

Managing risks of downgrade in the BBB space is evidently of crucial importance now. Recent manager research indicates major differences between different firms in this area, with some implementing a highly systematic, structured approach while others take a more informal path.

This isn't the environment to be sitting on the fence. You have to have an opinion, and you have to back it with data.

More rigorous approaches include updating the quantitative and qualitative analysis of all covered issuers, with specific focus on those currently rated BBB, to reassess the probability of downgrade or default – effectively re-underwriting the investment case for all positions. This should be based on specific companies, not just sectors: even within more and less vulnerable industries, firms have balance sheets of varying strengths. Such analysis gives managers the ability to give a data-based judgement, at any point in time, on how much of the portfolio is “at risk.” Some managers, on the other hand, are merely sending out the message that they wouldn’t hold anything which they believed to be at risk of downgrade – a message which, unfortunately, sounds increasingly flimsy at a period in time when such a large proportion of the universe is vulnerable. While a degree of sanguinity is helpful, this isn’t the environment to be sitting on the fence: you have to have an opinion, and you have to back it with data.

Robust demonstrable analysis is not only important to investment outcomes. It is also of great importance to communicating with investors, who are keen to understand how their managers are viewing their risks and whether the investment case still holds. Many asset managers talk of “partnership” with their investors, especially before closing the sale: promises of knowledge sharing and informational exchange are increasingly central to client acquisition. Yet today is an acid test, showcasing which managers are really communicating effectively with their investors.

Expectation mismatch?

In our recent poll of 260 asset owners globally (March 20th, 2020), a majority of investors using investment grade credit reported that they were “somewhat satisfied” or “very satisfied” with how their investment grade credit portfolios had performed during the downturn so far, while 35% claimed that they were “not satisfied.” Are these differences purely a result of manager performance dispersion – which is significant? Or, more fundamentally, have asset owners been caught unawares by the amount of credit risk within their IGC portfolios?

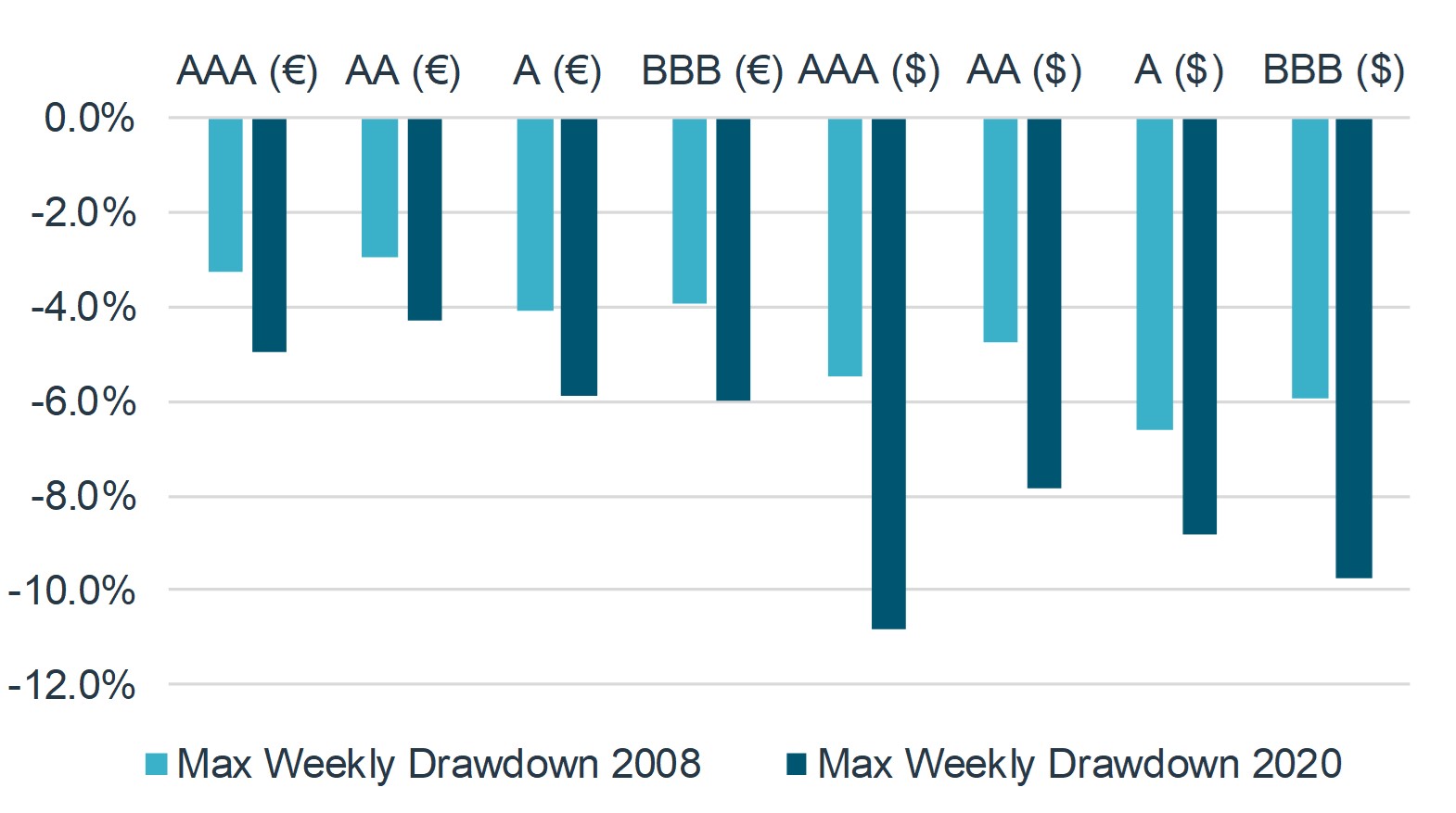

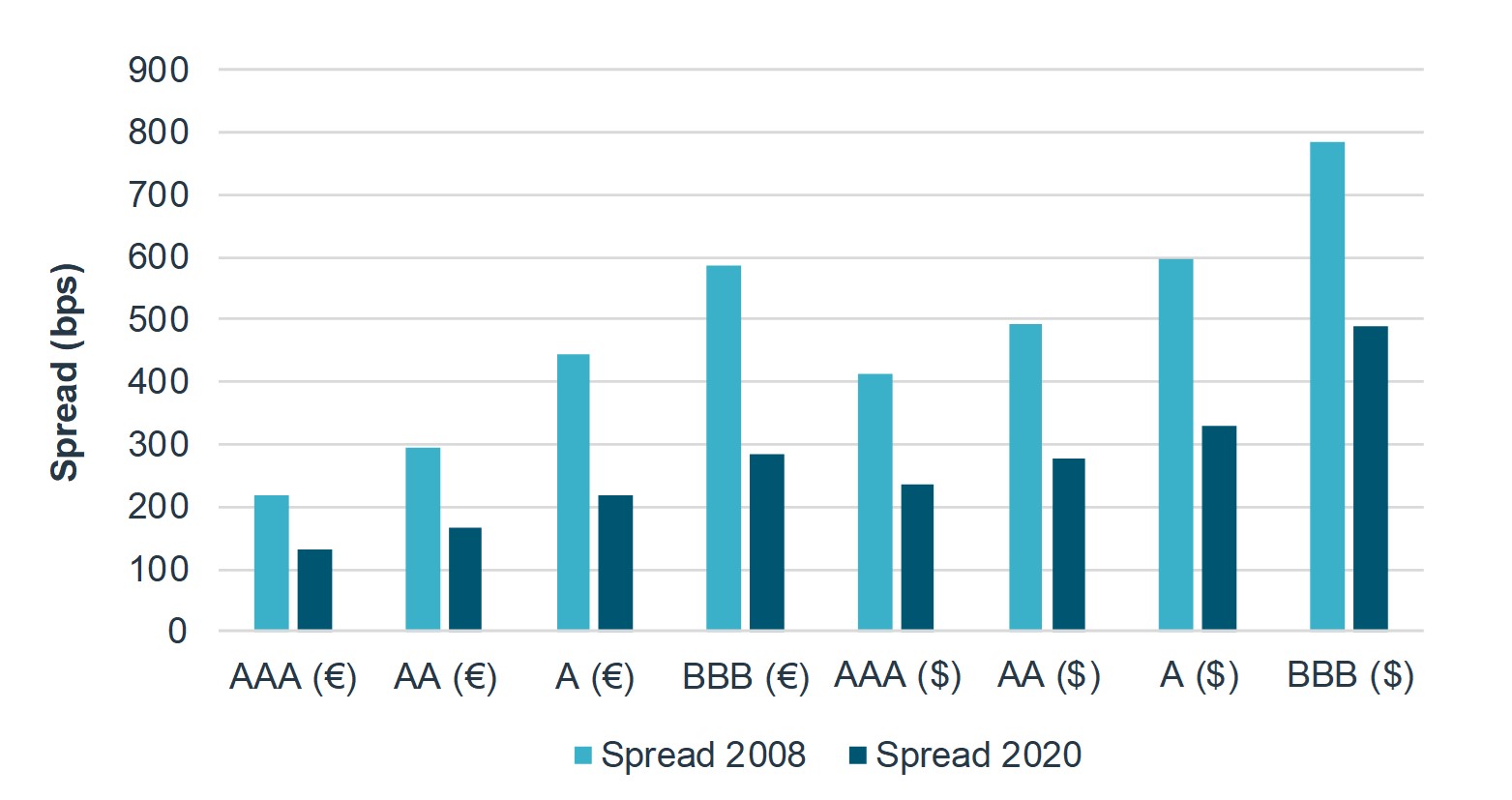

It is, perhaps, worth casting an eye back to the last major financial crisis for a comparison on how investment grade credit performed during these two severe (albeit very different) downturns. Maximum weekly drawdowns in 2020 have been considerably more severe than in 2008, across the entire investment grade spectrum. In 2008, the maximum credit spread on US BBB was just shy of 800bps; in 2020 so far the maximum spread is less than 500bps.

FIGURE 2: MAXIMUM WEEKLY DRAWDOWN, 2008 VS. 2020

Source: Bank of America Merrill Lynch

FIGURE 3: MAXIMUM CREDIT SPREAD, 2008 VS. 2020

Source: Bank of America Merrill Lynch

There are plenty of reasons why performance during 2008 was different. Firstly, the initial liquidity impact has been much more severe in this crisis, representing a major contributor to the drawdowns seen to date, while the liquidity crunch in 2008 took several months to play out. Central bank action has been more swift and globally co-ordinated than it was in 2008, and has been rapidly followed by significant fiscal support measures from governments: this could help to normalise liquidity more quickly than was the case during the “GFC,” although the indefinite lockdowns imposed by many governments makes the future highly uncertain. This action includes extending asset purchase programmes into corporate bond markets (e.g. investment grade corporate bond ETFs and short-dated IG credit), which could help – at least in part – to address the liquidity challenge, provide an added cushion to bonds at risk of downgrade, and give interesting opportunities for active managers.

The rules around those programmes are now somewhat clearer, after a couple of weeks of activity and last week’s announcement on the subject by the Federal Reserve. While the Fed initially committed to only purchase investment grade corporate bonds through the so-called Secondary Market Corporate Credit Facility (SMCCF), they extended it on April 9th to purchase sub-investment grade bonds that were downgraded after 22nd March, so long as they are rated BB-/Ba3 at the time of purchase. This provides an extraordinary and unprecedented cushion to Fallen Angels. At the time of writing, no equivalent scheme to buy sub-investment grade debt has been indicated by the European Central Bank.

Hunting ground

One thing is certain: in an environment of forced selling, reduced liquidity, widespread downgrades and uncertainty, there should be plenty of scope for active managers to create value, both by holding securities when others can’t and by taking advantage – where liquidity permits– of buying opportunities. Fallen angels can be a liability; once downgraded, however, they also represent a window to purchase high quality paper at discounted prices. Even within the most challenged sectors there are companies that are relatively well placed to survive and thrive.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.