English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Robert Doyle

Senior Director, Public Markets

In the landscape of ‘global’ active equity strategies, the pendulum has—slowly but surely—swung toward strategies that span both developed and emerging markets. Yet how credible are these broader global offerings as a means of providing GEM (global emerging markets) exposure? In this article, we address five questions that are frequently asked by investors when considering ‘go anywhere’ strategies for global equity implementation.

Ten years ago, 42% of available ‘global’ active equity strategies were benchmarked against the MSCI ACWI or another ‘all countries’ index. Yet 56% of all new launches since that time fall into this bracket, while 40% are benchmarked against the MSCI World or a similar ‘developed markets only’ index and the remaining 4% have no benchmark. As a result, today’s split of EM-inclusive global equity strategies versus those that only cover developed markets is around 50:50.

Below, we examine five investor ‘FAQs’ relating to global equity strategies that offer EM exposure, often colloquially referred to as ‘ACWI strategies’ after one of their favoured benchmarks. For example, do they just focus on the largest EM stocks in the most liquid markets, as is sometimes assumed? How much EM exposure do they provide? Do managers tactically allocate between DM and EM? Are benchmarks being used appropriately? For answers, we look at portfolio holdings across a highly representative universe of close to 600 active global equity strategies that feature EM stocks. First, however, we briefly consider the drivers behind this tectonic shift in the equity strategy landscape.

The rise of EM-inclusive global equity strategies

The trend to incorporate EM stocks within active global equity portfolios is a result of several forces, spanning both supply (the asset manager provider) and demand (the investor buyer).

The most clear-cut factors lie on the supply side: this is, first and foremost, a story of asset managers and their changing capabilities. Crucially, an increasingly long list of global asset managers have launched or expanded their emerging markets product offerings. This opens the door to using those same EM resources and research capabilities within other appropriate types of strategy, with global ‘all country’ strategies a likely beneficiary. Meanwhile, the improved liquidity in emerging markets allows for managers to make larger trades without significant price impact, meaning that EM positions can be applied across multiple strategies and larger asset bases without compromising outcomes.

Asset managers’ research philosophies are changing too. Company research is increasingly being conducted on a global industry basis, with analysts looking across both developed and emerging markets. Indeed, we might argue that (in certain areas) analysts should now cross borders in order to understand their areas of coverage fully; an analyst of the semiconductor industry, for example, must have a strong understanding of market leader TSMC (Taiwan Semiconductor Manufacturing Company) in order to assess the prospects of its DM-listed competitors. With markets and economies becoming increasingly interconnected, a country’s company of listing is not always a useful guide to its economic exposure. The ‘go-anywhere’ argument is an intuitively enticing one as well: in theory, flexibility and agnosticism across a very broad opportunity set should represent a potential advantage for active managers. Although, as we find time and again in active management, opportunity does not necessarily equal outperformance.

While asset managers have been developing, there has also been evolution on the ‘demand’ side: investor constituencies have changed considerably over the past decade. There has long been a place for both developed market and EM-inclusive ‘global’ strategies, with investors bringing different preferences to bear in terms of governance/oversight requirements, geographical allocations and portfolio construction philosophy (as discussed further below). Yet it’s also worth noting that the rise of defined contribution pension plans featuring member choice and the expansion of private wealth management have brought additional clients for EM-inclusive global equity fund offerings.

Five investor ‘FAQs’

#1: “Which benchmark should we use? Do all EM-inclusive global equity strategies use an all-country benchmark like MSCI ACWI?”

EM-inclusive global strategies are often referred to as ‘ACWI strategies’ after the MSCI All Country World Index. That being said, throughout our search activity, we find many instances of managers setting forth their performance against chosen benchmarks that do not fit their geographical profile, such as developed markets strategies using the MSCI ACWI or EM-inclusive strategies using the MSCI World. These inconsistences will be headwinds and tailwinds for relative performance at different times; investors will likely be aware of the underperformance of the MSCI ACWI versus the MSCI World over the past decade (illustrated in the table shown here), largely due to the relative outperformance of developed markets vs emerging markets.

When assessing prospective global equity managers, investors should pay close attention to the benchmarks used to make sure that they’re appropriate to the strategy—especially where there may be an optical performance advantage in play. In practice, all participants in this sector are typically comfortable being measured against both developed market and all-country benchmarks.

Figure 1: Annualised index performance*: MSCI World vs. MSCI ACWI

Source: MSCI. USD total return to 30 September 2023.*Indices are not directly investable.

#2: “How much EM exposure will we get from an active ACWI-type strategy?”

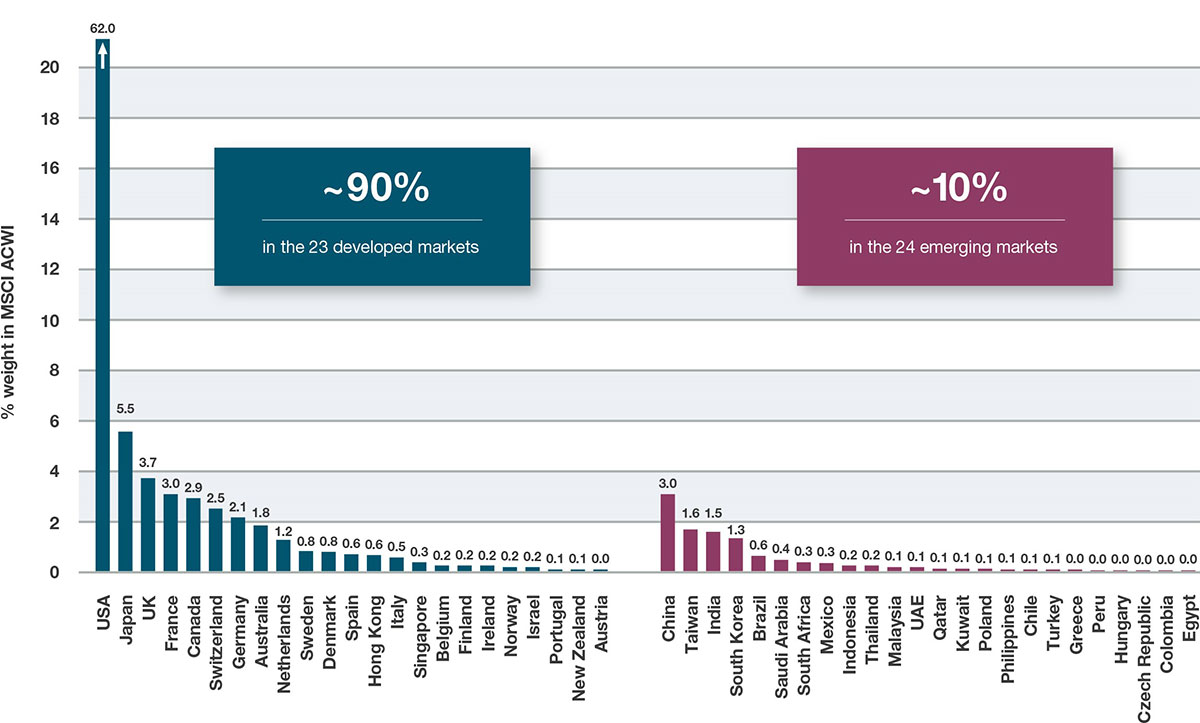

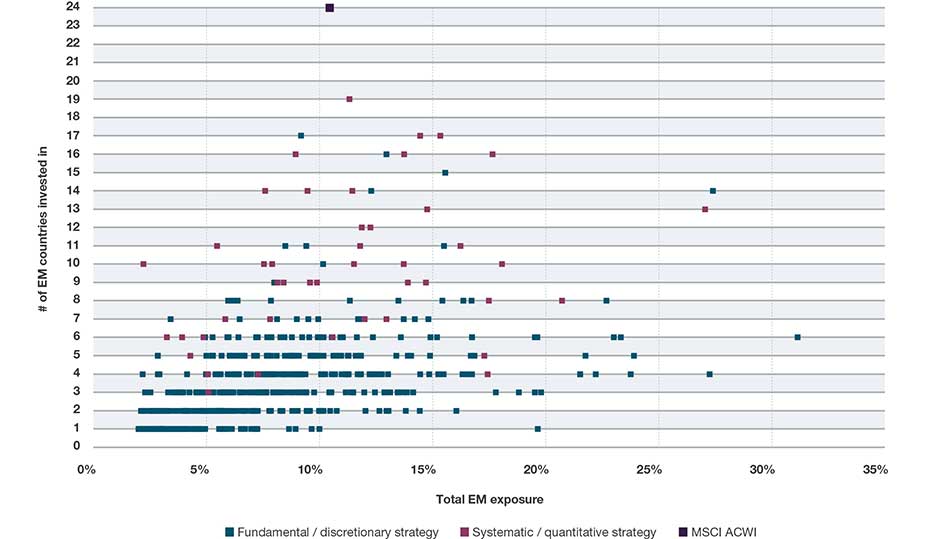

The MSCI ACWI has shown an allocation of approximately 8-12% to emerging markets over the past decade, with the current distribution of geographical weightings shown below, in Figure 2. We find that active global equity strategies with an EM-inclusive remit currently allocate a median of 7% to emerging markets–a not-insignificant underweight versus the index level of 10.5%, in other words. Only 25% of ACWI strategies currently hold an overweight position in emerging markets compared to the MSCI ACWI and just 3% allocate more than 20% of their portfolio. This conclusion is broadly consistent when viewed at different times over the last five years. The underlying picture is a diverse one, as shown in Figure 3.

The breadth of country exposure—indicated in the y axis on this chart—is also an interesting subject, and one to which to which we will return in question four.

Figure 2: MSCI ACWI, by country weighting

Source: MSCI ACWI, at September 30 2023

Figure 3: Global active equity strategies with an all-country remit, EM exposure vs. number of EM countries held

Source: eVestment. Data as at 30 September 2023. Approximately 600 strategies shown: each data point represents one active global equity portfolio.

#3: “Are ACWI strategies just focused on the largest EM companies?”

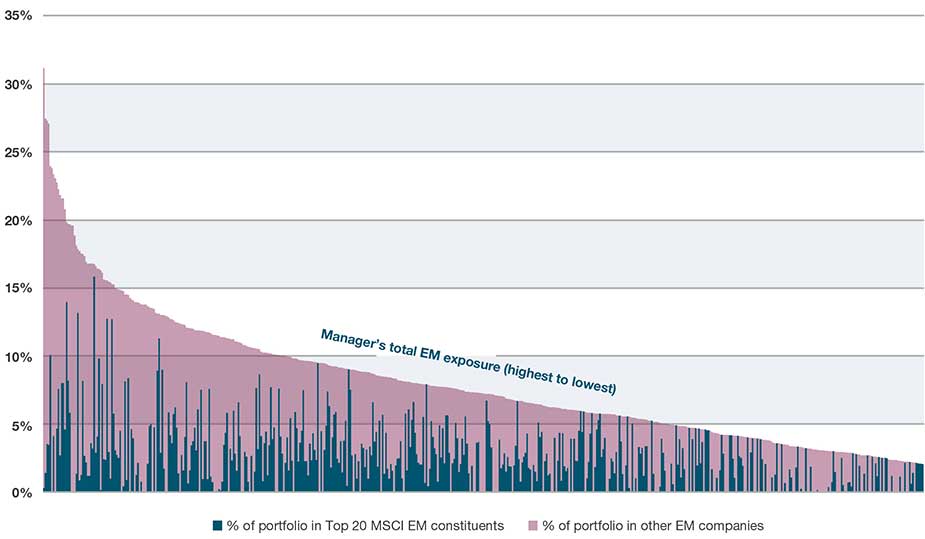

While ACWI strategies do (on average) show significant allocations to the largest EM companies, analysis indicates that many managers do look beyond the big stocks. Typically, and statistically, managers with a larger overall allocation to emerging markets are less likely to be wholly or largely reliant on the top twenty EM stocks than those managers who invest a smaller proportion of the portfolio. That being said, there are a number of funds with smaller EM allocations who do make considerable use of small and mid-cap stocks.

Figure 4: Global active equity strategies with an all-country remit, exposure to Top 20 EM stocks vs. other EM companies

Source: eVestment. Data as at 30 September 2023. Approximately 600 strategies shown: each stacked column represents one strategy

#4: “Do ACWI strategies only invest in a handful of large EM countries?”

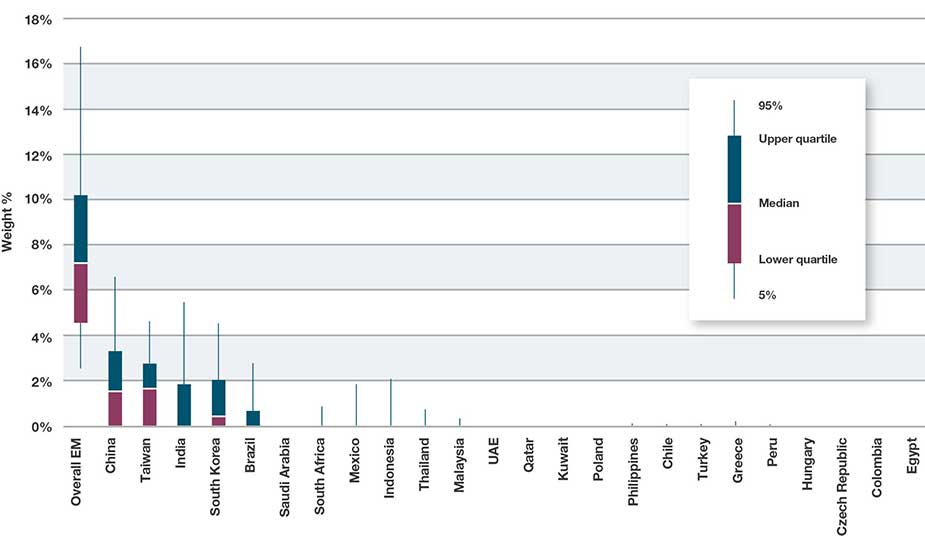

Although ACWI strategies, theoretically, have the freedom to invest in all 24 emerging markets, data reveals that they tend to concentrate their allocations in a small number of these countries. Our data indicates that the median manager within this group was invested in just three emerging markets. As shown in Figure 3 above, systematic strategies tend to allocate to a larger number of EM countries than their fundamental counterparts.

Perhaps unsurprisingly, there is also a strong bias towards the larger emerging economies: these provide a more extensive and diverse range of investment opportunities; a focus on these biggest countries may satisfy the needs of their clients from a commercial standpoint. Yet even some of the largest markets are frequently absent from these portfolios: 30% of the EM-inclusive global equity strategies assessed here have no Taiwan exposure, 35% don’t use China, 45% have no South Korean stocks, 54% nothing in India.

Figure 5: Global active equity strategies with an all-country remit, exposure to specific EM countries

Source: eVestment. Data as at 30 September 2023.

#5: “Do ACWI managers tactically adjust their overall exposure to emerging markets vs. developed markets?”

While there is a small group of managers that base their portfolio construction around top-down region/country views, the overwhelming majority of strategies rely on bottom-up stock selection. The purported rationale of all-country strategies is to provide managers with flexibility to invest in the most compelling opportunities irrespective of listing country. If we consider the previous example of the semiconductor industry, for example, a decision to invest in TSMC rather than Dutch-listed ASML is extremely unlikely to be driven by a view on Taiwan versus the Netherlands, Asia versus Europe or the Taiwan dollar versus the Euro. That being said, aspects such as currency and domestic politics may play a role in whether to ultimately invest in a country.

Conclusion: portfolio construction in focus

There is no one-size-fits all answer to the question of whether to use ACWI strategies in portfolios. These can be treated as ‘one-stop-shop’ allocations or they can form part of broader portfolios alongside other equity strategy types, in a variety of combinations. Designs tend to be specific to each investor and sit within the context of the overall approach to geographical, style and manager diversification. There is, of course, a risk of overlapping positions: the same EM companies, for example, may crop up in both an ACWI strategy and a dedicated EM strategy.

In light of the data shown above, investors may also wish to bear the diversity of active manager approaches in mind when determining the appropriate strategy. As shown, different active ACWI managers offer dramatically different profiles in terms of the depth and breadth of their EM coverage. The answers to portfolio construction are not solely found in benchmark-driven modelling: it is important to assess specific strategy and manager complementarity with care.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.