English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

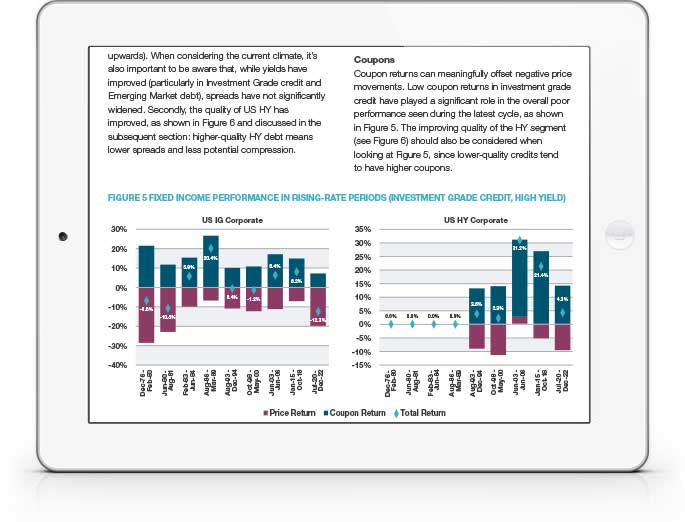

Fixed income performance in periods of rising rates: While USTs and US Investment Grade often generate flat to negative performance during rising-rate periods, a number of fixed income sub-sectors have provided moderate-to-strongly-positive returns. Yet the factors supporting performance are changing over time: investors should keep a close eye on the magnitude of coupons, potential for spread compression and the changing duration profile of the relevant markets.

Investment grade vs. high yield during recessions: A risk-off stance in fixed income is broadly beneficial during recessions, minimising exposure to defaults. However, High Yield performance is not far behind Investment Grade, with the HY market typically recovering significantly earlier than the real economy.

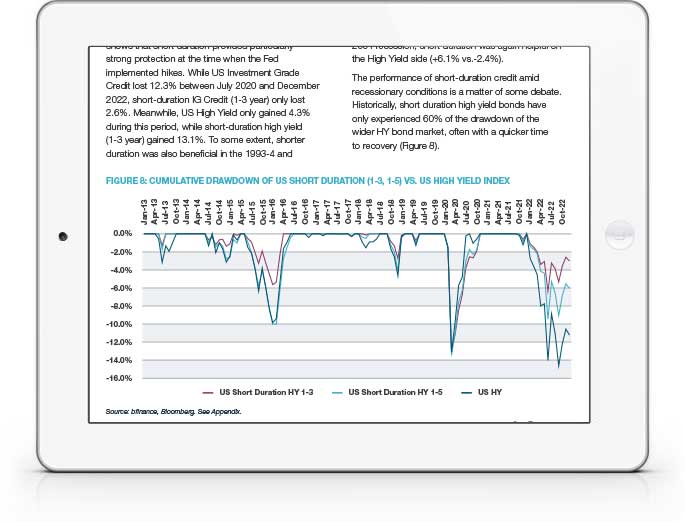

Short-duration assets and volatility: Short duration bonds often outperform during rising rate periods, show resilience in recessionary conditions and—overall—produce lower volatility and better risk-adjusted returns. However, bad debt may crowd the short-duration high yield market at times of credit stress.

WHY DOWNLOAD?

Investors are reassessing how to position fixed income portfolios after a period of historic, diversification-defying disappointment. The year 2022 marked the first time since the 1970s that an extended equity market drawdown was accompanied by negative performance in the US Aggregate bond index. Meanwhile, both the LDI crisis of 2022 and the banking crisis of 2023 have highlighted the damage that can be inflicted on balance sheets (and financial systems) when theoretically low risk fixed income assets lose value.

For fixed income investors, the current macroeconomic environment presents uncomfortable ‘Catch-22’ choices, with policymakers walking a thin line between combatting inflation and averting (or at least mitigating) the recessions that often follow rate rises. Market participants face a slew of competing concerns. Rising rates will hurt the asset class, or so runs the received wisdom, but substantial allocations are beneficial during recessions. Rising rates favour lower-quality credits but recessions supposedly favour higher-quality (and generally longer maturity) credits.

This report interrogates ‘received wisdom’ surrounding fixed income and its performance through periods of rising interest rates, recessions, or both. Here we look at three popular beliefs, test those assumptions against the historical data in the US (as the source of the richest available information) and consider the current context.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.