English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Chris Stevens

Director

Equity long/short strategies are ahead of the curve on ESG and carbon emissions versus their hedge fund counterparts in other strategies–thanks largely to the groundwork laid by the long-only equity investment industry and its data suppliers. Yet investors that are explicitly seeking ESG-aware or climate-aware approaches in the long/short space may still be unsatisfied with the selection on offer. In addition, the recent focus on CO2 emissions has provoked debates around the treatment of long/short strategies within investors’ carbon calculations.

In 2021, we highlighted the growing number of calls for hedge funds—historically one of the more ESG-resistant sectors of the asset management industry—to focus on the subject (From Laggards to Leaders). Indeed, around two thirds of investors claimed their hedge fund managers offered either ‘Low’ or ‘No’ ESG integration in bfinance’s ESG Asset Owner Survey, published in that same year. Meanwhile, more than 50% of managers in BNP Paribas’ Hedge Funds and ESG report in 2020 indicated that their investment strategies make ESG integration “irrelevant”, “immaterial”, or “impossible to quantify”.

Some notable progress has been made. Equity long/short strategies in particular, which range from long-biased approaches to equity market neutral funds, have benefited from the extensive research, data and practices forged in the long-only space. We have also seen the emergence of a small number of long/short equity strategies that specifically use ESG data as their primary trading signal.

The equity long/short sector has had an awkward and tense relationship with the ESG agenda

The equity long/short sector has had an awkward and tense relationship with the ESG agenda. Shorting has been a topic of repeated debate along various lines, including general questions of whether shorting is too ‘short term’ an approach to be a sustainable investment technique, alongside more empirical questions around its impact on companies’ cost of capital or management behaviour. For investors with strict exclusion lists (established for long-only portfolios), the question of whether covering a short (i.e. purchasing the stock) violates the policy has also been a hotly debated topic. More recently, shorting has been in the crosshairs of the ESG debate again—this time with carbon calculations in focus.

Today, investors—pension funds, endowments and others—are keen to explore whether they might now be able to find more sophisticated ESG-integrated approaches in the equity long/short space. In addition, many asset owners have recently introduced goals relating to carbon emissions and are seeking to understand how various asset classes can contribute to the reporting, and the long-term reductions, that are required.

Unfortunately, investors with more ambitious ESG goals can still find the equity long/short sector quite challenging. Many managers remain reluctant to make ESG an integral part of their investment processes. Smaller managers in particular continue to cite challenges and are struggling to cope with increased reporting requirements from clients. Below, we look at a number of key areas and consider how equity long/short managers stack up.

MOST EQUITY LONG/SHORT MANAGERS ARE NOW PRI SIGNATORIES

Although signing up to the Principles for Responsible Investment does not necessarily signpost a credible ESG investment approach, it can be viewed as a positive sign of senior management commitment. Indeed, many firms treat signing up to PRI as one of the early steps on their ESG journey.

According to data from Kepler Partners, complemented by proprietary research from bfinance, 77% of managers in the UCITS part of this sector are PRI signatories. The figures will certainly be lower for the non-UCITS constituency given the pro-ESG orientation of European institutional clients which make up the majority of UCITS investors.

If we look towards the long-biased (or variable net) end of the equity long/short spectrum, 75% of UCITS funds—comprising around 90% of assets under management—are managed by PRI signatories.

Even more positive, we find that 83% of ‘equity market neutral’ (EMN) UCITS strategies are managed by PRI signatories. That might come as a surprise to readers: EMN funds may appear less compatible with ESG practices than their heavily long-biased counterparts, given their distance from the long-only origins of ESG investing.

NEARLY ONE THIRD OF UCITS EQUITY LONG/SHORT FUNDS ARE ‘ARTICLE 8’ OR ‘ARTICLE 9’

Among long-biased long/short strategies, 23% of UCITS funds are classified as Article 8 under the European Sustainable Financial Disclosure Regulation (‘promote environmental or social characteristics’) while a small handful (3%) are Article 9 funds (‘have sustainable investment as their objective’). In the EMN space, 44% of UCITS funds have the Article 8 tag while just 2% are marked Article 9. When looking at these two groups together, some 32% of UCITS equity long/short funds have either an Article 8 or an Article 9 designation.

These SFDR labels have, of course, been problematic. Many strategies have changed their designations, as discussed in this article: One Year On, Have Sustainability Disclosure Regulations Brought Clarity or Confusion?. Investors should not confuse Article 9 funds with ‘impact’ strategies or assume that an Article 8 fund will be robust from an ESG perspective. Nonetheless these are quite significant figures–although we may see a redesignation wave as the regulations become clearer.

CARBON REPORTING IS NOW STANDARD. BUT WHAT IS THE RIGHT APPROACH?

Equity long/short strategies now typically provide carbon reporting for long positions and short positions. The reporting is relatively comprehensive in terms of stock coverage, in part because the types of companies used in these strategies (liquid, highly tradeable) are highly likely to be reporting carbon data to third-party suppliers. That being said, this reporting tends to be wholly reliant on external data, is essentially backward-looking and is very unlikely to give consideration towards scope 3 emissions (see Carbon Cuts or Climate Impact?).

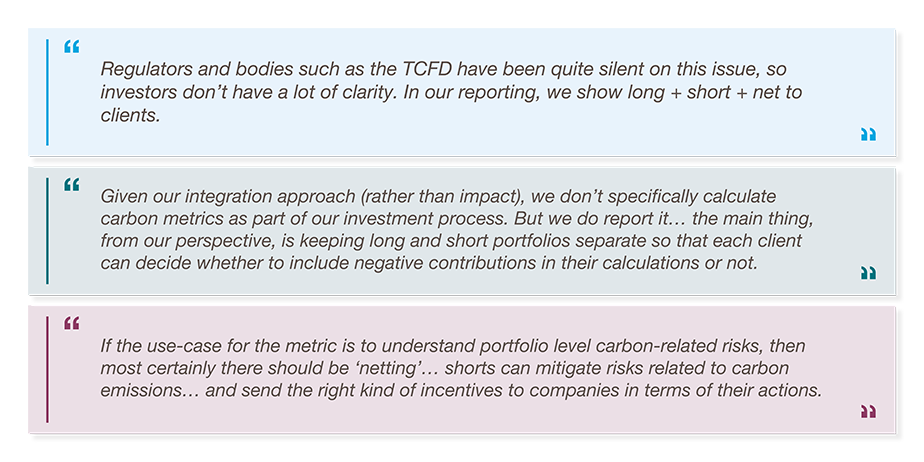

2022 saw a flurry of industry debate on the topic of ‘netting’ in carbon accounting, from a much-reported-on MSCI whitepaper (ESG Reporting in Long-Short Portfolios) to the pages of the Financial Times where the CIO of Harvard’s endowment wrote in favour of short-sellers as ‘agents of decarbonisation’ – disagreeing openly with an article penned by Man Group’s Jason Mitchell on the topic. At present, there is a lack of clear and internationally consistent regulatory guidance, or industry consensus, on this subject.

Granted, shorting a high CO2 emitter does not remove carbon from the atmosphere. Yet, by the same logic, buying the liquid stock of a high CO2 emitter does not add carbon to the atmosphere, challenging the very basis of carbon accounting in portfolios. It would make sense for a symmetry in treatment between longs and shorts, but we cannot say the same with regards to the notion that a single 'net’ figure will be useful for investors. Netting—counting shorts against long positions—should not be used to give hedge funds an easy ride on decarbonisation, nor to directly compare two funds without additional context (there are many ways to get to a low ‘net’ number). We expect that clients will increasingly value the transparency of separate data for the long and short sides of a portfolio, rendering the debate around a net figure less relevant.

What do managers say?

CONCLUSION: POSITIVE STEPS

As the demand for sustainable investing rises and investors continue to focus on climate/carbon, we expect equity long/short managers to continue making progress on this subject. It is crucial to remind ourselves that carbon reporting is still in its infancy in general, and this asset class brings additional complications. With over $1.1 trillion of assets (and even more on a leveraged basis), the equity long/short sector has significant potential to influence the global decarbonisation agenda, as well as sustainable practices more broadly, and so any positive moves should be welcomed. Investors should prioritise identifying managers with an investment philosophy that aligns with their own on this subject, rather than one whose current approach ticks certain boxes (e.g. PRI, Article ‘X’) or which has a single attractive portfolio metric (e.g. low net carbon intensity).

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.