English (Global)

English (Global)  Français (France)

Français (France)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Jill Compton

Senior Director Client Consulting, UK & Ireland

Sarita Gosrani

Director of ESG and Responsible Investment

Thanks to recent guidance from the Charity Commission for England and Wales, UK charities became the latest cohort of institutional investors to receive official endorsement for considering ESG factors such as climate, human rights, sustainability and community impact within their investment processes. Yet a robust, professional approach is crucial: charities, notwithstanding their typically high reliance on external managers and advisors, must rigorously re-evaluate their policies and provider relationships.

Official approval for ESG integration in the form of legal and/or regulatory statements, or the lack of it, can be of critical importance to institutional investors. In the US, for example, the subject of ESG investment by employee retirement plans has been a political football for years. In September 2023, a landmark ruling from U.S. District Judge Matthew Kacsmaryk blocked efforts by 25 Republican states to obstruct a Biden administration ruling that permitted employee retirement plans to consider ESG issues alongside all-important financial returns—a ruling that itself overturned a Trump move to eliminate ESG considerations from pension plans’ scope. Indeed, the new UK Charity Commission guidance released in August 2023 was itself spurred by a high-profile court case (Butler-Sloss), wherein charity trustees—in the absence of clear approval—sought and obtained the backing of the High Court to invest with their environmental mission in mind.

Without explicit, consistent and ideally apolitical top-down support, institutional investors may rightly be nervous about the subject, not least because of the potential for negative public scrutiny. In the UK, for example, 2023 has seen high-profile charities such as the National Trust come under fire from influential newspaper journalists that appear keen to attribute negative investment performance to ‘green’ investment agendas. Depending on prevailing market forces (and energy prices in particular), ESG-branded portfolios—particularly those of the more exclusionary variety—may well undergo extended periods of both over- and under-performance versus counterparts, leaving organisations vulnerable to short-term critique.

The new rules appear to provide reassurance to UK charity investors for incorporating ESG, climate-oriented or impact investment considerations.

The new rules appear to provide reassurance to UK charity investors for incorporating ESG, climate-oriented or impact investment considerations. Indeed, the move could even place reluctant actors under pressure to do more in this space. The wording provides explicit approval for the consideration of factors such as climate, human rights, sustainability and community impact – whether these are integrated in order to manage investment risk or to advance interests related to the charity’s ethical mission (or both). Moreover, the rules also enable trustees to consider both positive and negative ESG-related impacts of their investment decisions.

Yet the guidance is far from a ‘carte blanche’ for ESG – and nor should it be. The language reiterates the duties of trustees with respect to investment matters including ESG and reminds readers that, while they can rely on investment advisers or investment managers for guidance, they remain responsible for the quality of advice received and for managing conflicts of interest.

Already-high ESG penetration among non-profit investors

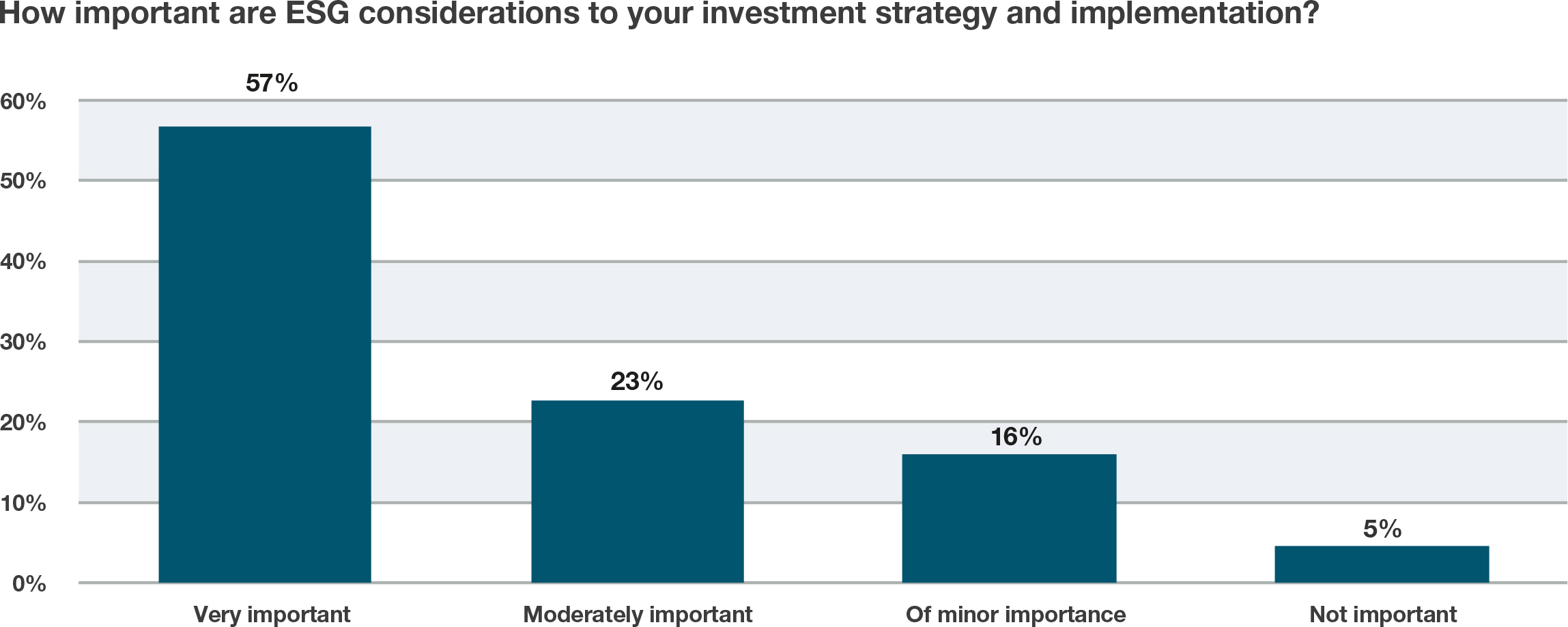

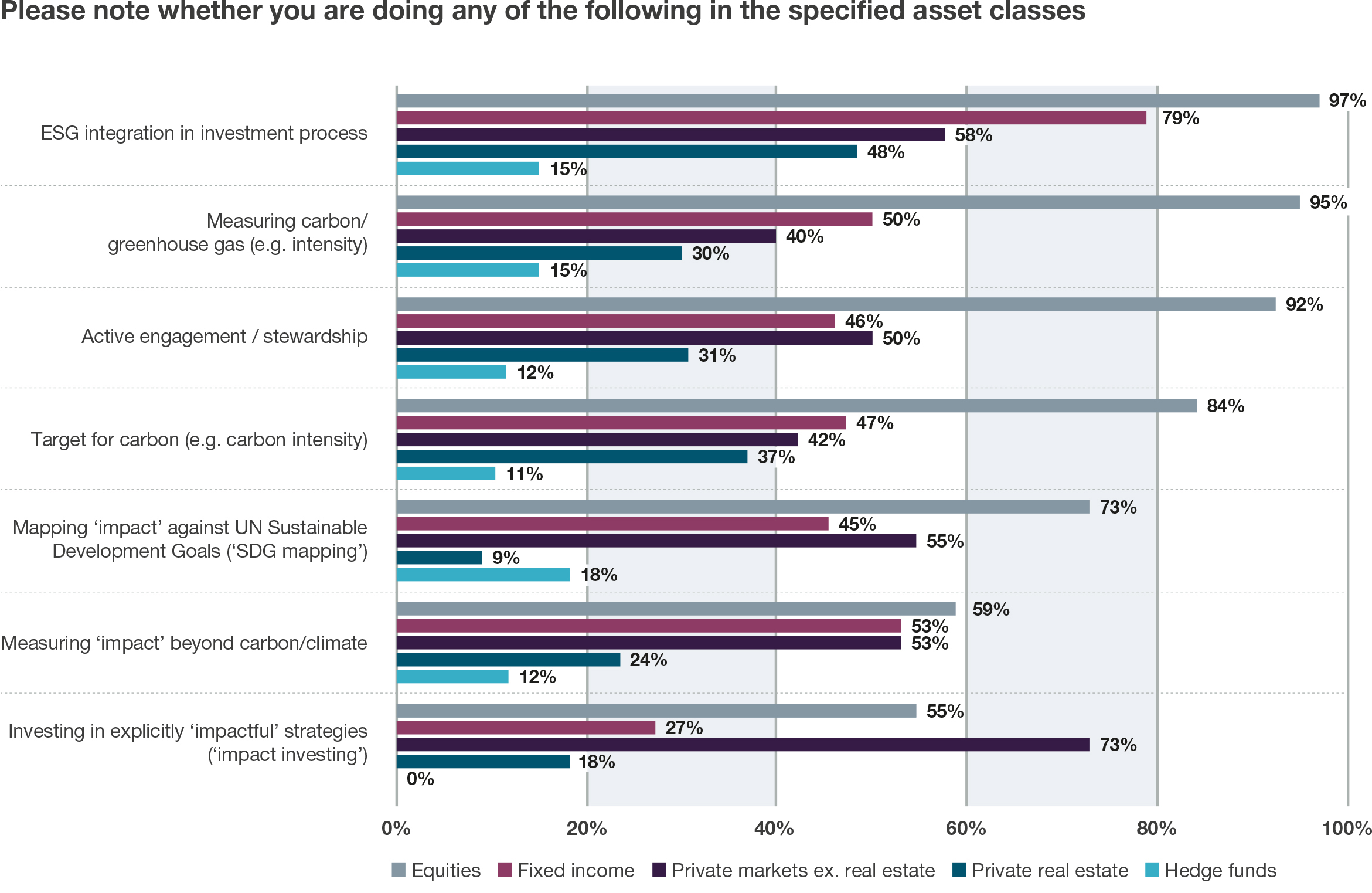

ESG investing is already well advanced within the non-profit investor sector globally. According to new (soon-to-be-published) bfinance research, 57% of non-profit investors (Endowments, Foundations and Charities) globally believe ESG considerations to be ‘very important’ to their investment strategy and implementation, while a further 23% consider them ‘moderately important’. Significant proportions of non-profit investors are engaging in ESG integration and newer practices such as carbon reporting and impact measurement – not just in equities, where data is more developed, but across other asset classes as well.

Source: bfinance Endowment & Foundation Investment Survey (61 respondents in October 2023)

Overall, the figures are broadly in line with, or slightly behind, those seen among pension fund counterparts. Yet the average investor size in this community is considerably smaller – a factor that, across all investor segments, typically correlates with lower resources and less activity across these fields.

Pursuing professionalism; reevaluating relationships

With ESG investment activities and the accompanying debates likely to remain in the limelight, it is more important than ever for charity trustees to pursue high standards, not just with respect to ESG but across all investment affairs. While there are plenty of examples of strong investment governance and practice in the UK charity sector, it is also—we must recognise and acknowledge—quite common to see instances where the approach is somewhat less robust.

For example, when it comes to investment policies (or standalone ESG policies), the substance relating to ESG or sustainable investment matters often lacks clarity and detail compared to what we would view as ‘best practice’ examples from the institutional sector. We also see many cases where charities have not thoroughly re-evaluated their external asset manager(s) or other service providers against prospective competitors for a decade or longer.

We see many cases where charities have not thoroughly re-evaluated their external asset manager(s) … for a decade or longer.

There are many reasons why external manager and advisory relationships should be monitored and reviewed regularly. The asset management sector is constantly evolving, and the developments in ESG capability are only one axis of change. We have also seen significant changes in portfolio design, the use of non-traditional asset classes or techniques, asset management fees (which have decreased in many cases), and strategic/administrative/other support (as with OCIO type offerings).

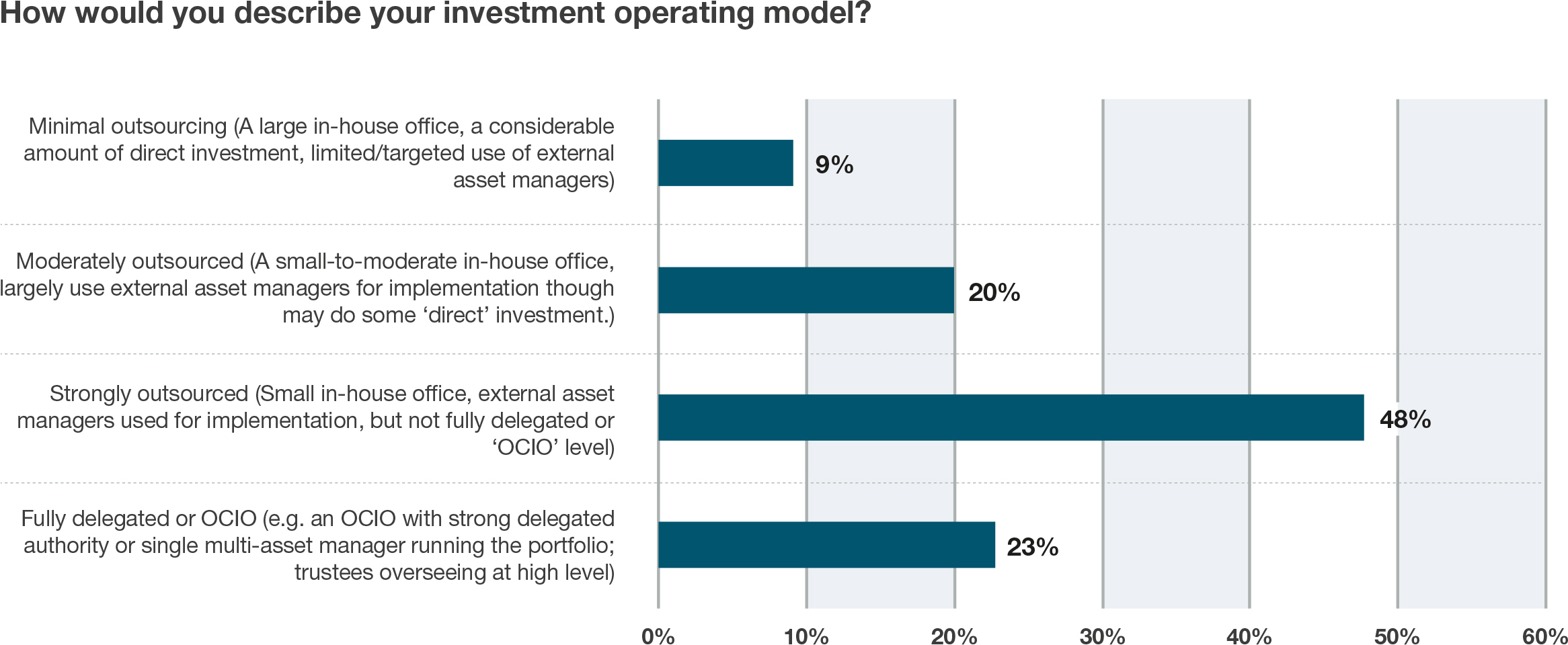

Significantly, the non-profit sector features a very high degree of investment outsourcing: nearly three quarters of investors in the aforementioned study describe themselves as having either a “strongly outsourced” or “fully delegated/OCIO” investment operating model. Heavy outsourcing of the investment function does not preclude strong and effective governance—indeed, it arguably makes it even more important—but it can leave the end-investor somewhat over-reliant on a narrow group of providers.

Source: bfinance Endowment & Foundation Investment Survey (conducted in October 2023)

Good governance and oversight of the external asset manager(s) or OCIO requires more than simply monitoring performance against a market benchmark and checking the numbers during periodic trustee meetings. It requires a proper understanding of how the appointed parties are delivering in terms of returns, risk, price, ESG/impact, service, and reporting, including whether alternative competing providers would likely be superior in some or all of these aspects. Some comparisons can be made through oversight, especially where the monitoring approach is of high quality; for others, the picture may only become visible through a competitive retendering of the mandate(s).

Next steps

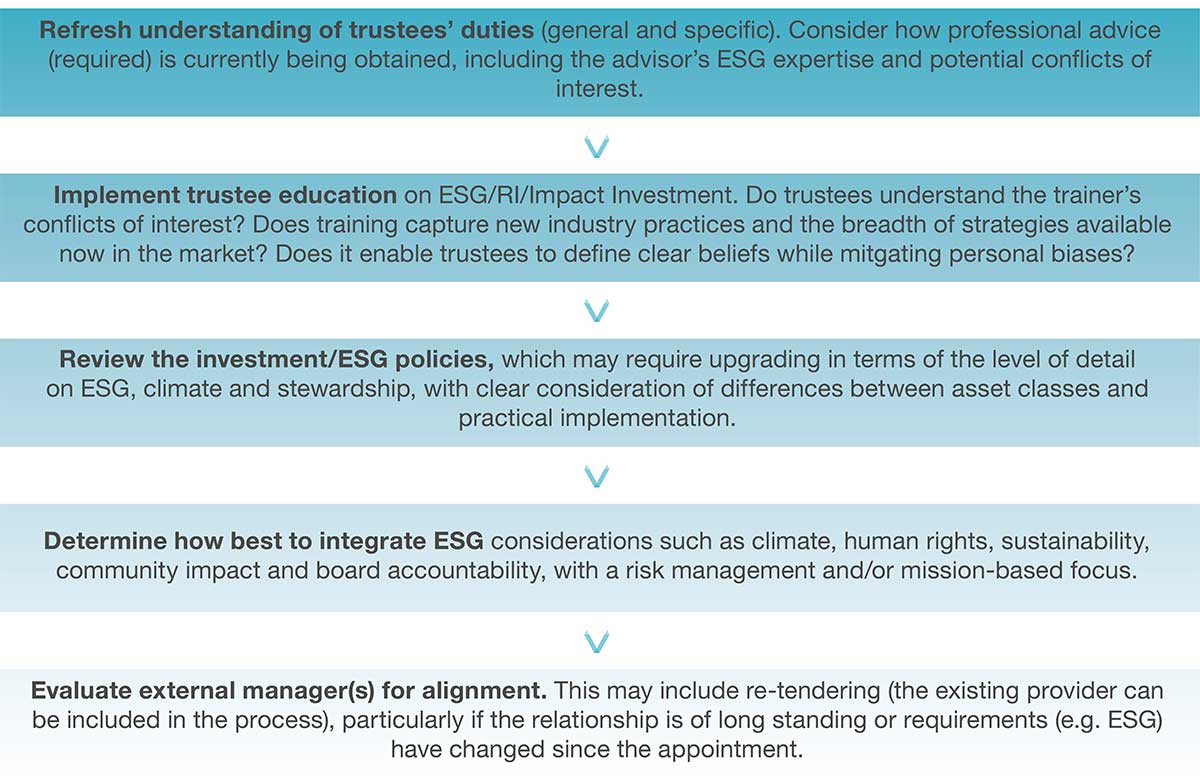

Trustees may consider taking a number of measures on the back of recent guidance.

Overall, the new UK Charity Commission guidance is to be welcomed. By providing some clarity it serves as a beacon, calling charities to consider the role of ESG in their own investment practices and offering reassurance for those that are already active in this space. Yet it also serves as a ‘call to action’ for trustees that may wish to re-evaluate the quality and suitability of their investment approach, both from an ESG perspective and more broadly.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.