English (Global)

English (Global)  Français (France)

Français (France)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

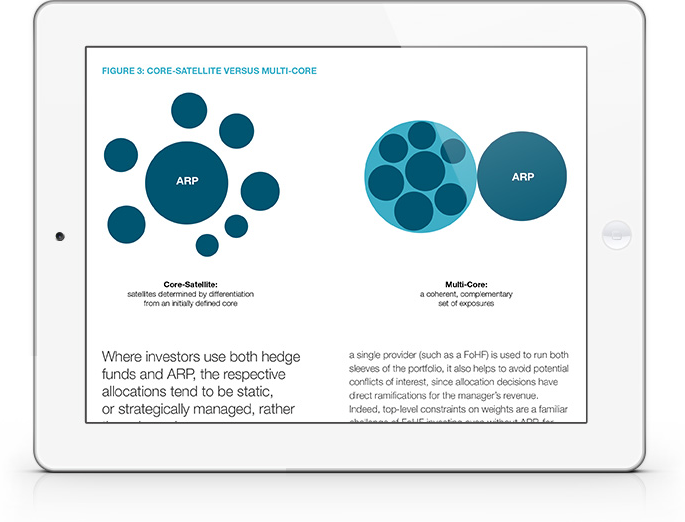

Complementing or competing? ARP and hedge funds make natural – but somewhat uneasy – bedfellows. Do they fit best in a core-satellite or multi-core methodology? And what are multi-managers who use both doing in practice?

The cost imperative. Moving 30% of a hedge fund portfolio to ARP would (conservatively) reduce overall management fees by 50bps and performance fees by 30bps. Yet investors concerned with cost should also note significant shifts in ARP and FoHF fees.

ARP access points: Investors seeking to blend ARP and hedge funds can access ARP in three distinct ways, each of which brings advantages and disadvantages.

WHY DOWNLOAD?

Just as in the world of coffee blends, ARP+HF mixtures are influenced by three motives: cost reduction, customisation and consistency.

While a proportion of cheaper coffee beans can cut expenses without excessively compromising on flavour, a spoonful of Alternative Risk Premia can make that cup of hedge funds more economically palatable. Roasters seek “signature blends” with a unique taste profile, while investors seek specific diversification characteristics that complement their particular portfolio exposures.

At bfinance, we observe an increasing number of our asset owner clients combining these two strategies, either at the level of the investor or the level of the asset manager with a 16+ firms now providing a blended product. Yet getting the right recipe is not straightforward. While some portfolios are impressive, we also observe incoherent combinations that produce excessive overlaps in exposures, alignment.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.