English (Global)

English (Global)  Français (France)

Français (France)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Pravir Sharma

Senior Associate, Diversifying Strategies

Toby Goodworth

Managing Director, Head of Liquid Markets

Last year saw Alternative Risk Premia (ARP) strategies recoup a substantial proportion of the losses endured during 2020—an annus horribilis during which the bfinance ARP manager composite lost more than 10%. With managers seeking to reaffirm their credibility, many have made significant changes in order to improve their responsiveness and resilience.

On paper, today’s increasingly uncertain climate for both traditional risk assets and core fixed income should have been highly supportive of allocations to Alternative Risk Premia. After all, this is an asset class with a five-year equity beta of 0.17 and a five-year beta to bonds (Barclays Global Aggregate) of 0.23.

The sector, however, has yet to emerge from the reputational damage caused by dismal performance in 2020. bfinance recently released data on manager search activity during 2021 that illustrates this collapse in investor demand. We have also seen five funds close down (or merge with other ARP strategies run by the same firm) in 2021, following eight closures in 2020—a 25% total reduction in the number of strategies in this category. Many investors have retained conviction that such strategies represent a diversifying asset class—and “a reasonably priced way of accessing investment ideas that are hard to access otherwise,” in the words of one Senior Investment Officer—but others have reduced or re-tooled their exposures.

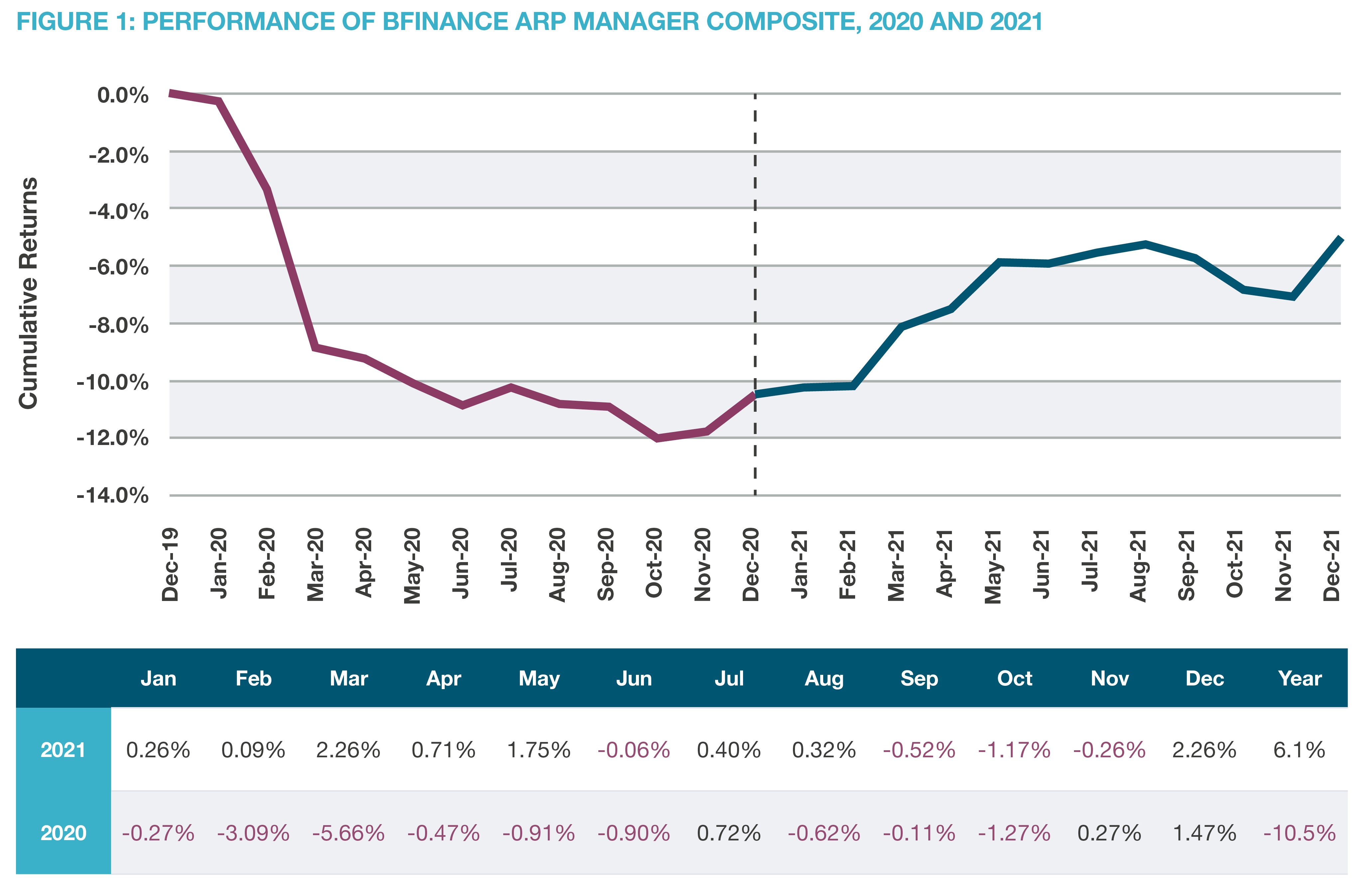

Source: bfinance. An equally weighted net-of-fees composite of ARP managers tracked by bfinance. This is a proprietary composite for reference purposes only; it is not necessarily investible and is subject to change. Strategies that no longer exist / report data are not removed from the composite, to reduce survivorship bias.

Importantly, asset managers have implemented notable changes to their pre-existing models and processes, making use of the new data that emerged throughout the COVID-19 crisis. In some cases, those changes have been modest: evolutionary adjustments and the inclusion of new research projects are always to be expected with quantitative strategies. In other cases, however, the alterations have been more significant. Models have been added and removed; signal parameters have been redefined; negatively-skewed premia (and their treatment in portfolio construction) have been re-examined; and the metrics used to determine risk allocations have been augmented or altered in an effort to improve diversification.

A common theme has been to boost the responsiveness and dynamism of these strategies. ARP strategies have typically used slower-moving trading signals to make themselves more scalable, but the market gyrations that accompanied the pandemic and subsequent macroeconomic uncertainties have made the lack of nimbleness increasingly unpalatable, forcing some managers to act.

At the same time, managers have been making greater efforts to integrate environmental, social and governance (ESG) signals into their models—a historically problematic challenge, given that these strategies predominantly involve trading ‘macro’ rather than ‘micro’ instruments. Some managers have standalone ESG-specific models, while others look to translate external macro-level ESG data into allocation tilts. We expect this trend to continue, especially among managers that use single-stock equities, but we do not expect to see the emergence of explicit ‘ESG ARP’ strategies.

Recent performance under scrutiny

In evaluating ARP, a sector that was predicated on its ability to eke out gradual gains through a variety of market conditions, it is necessary to seek an accurate understanding of recent results. Although strategies vary greatly in their implementation and parameterisation approaches—and have now evolved further in many cases, as noted above—we must understand 2020 performance and the 2021 recovery in order to form views around the strategic attractiveness of ARP going forward.

As discussed in previous analysis, the collapse in 2020—when the composite showed a record-breaking loss of 10.5%— was in large part driven by losses in the Equity Value premia, which finally enjoyed some respite in late 2020 when vaccine announcements brought about a rotation away from growth assets. Yet 2020 did have its bright spots. Trend premia, for example, performed well for managers that implemented slower-moving signals: thesestrategies entered 2020 very long equities (after the stock market surge of 2019) and held onto those long positions through the drawdown and recovery of March and April—and beyond.

2021 brought a welcome bounce back in manager performance, as illustrated by bfinance’s ARP manager composite (Figure 1). This composite achieved an annualised return of 6.1% in 2021, with 79% of managers delivering positive returns for the year and the median manager returning 4.6%. The strong run meant that managers made some headway in recouping their 2020 losses: of the 32 managers that ended 2020 in negative territory, seven were back in the black by the end of 2021.

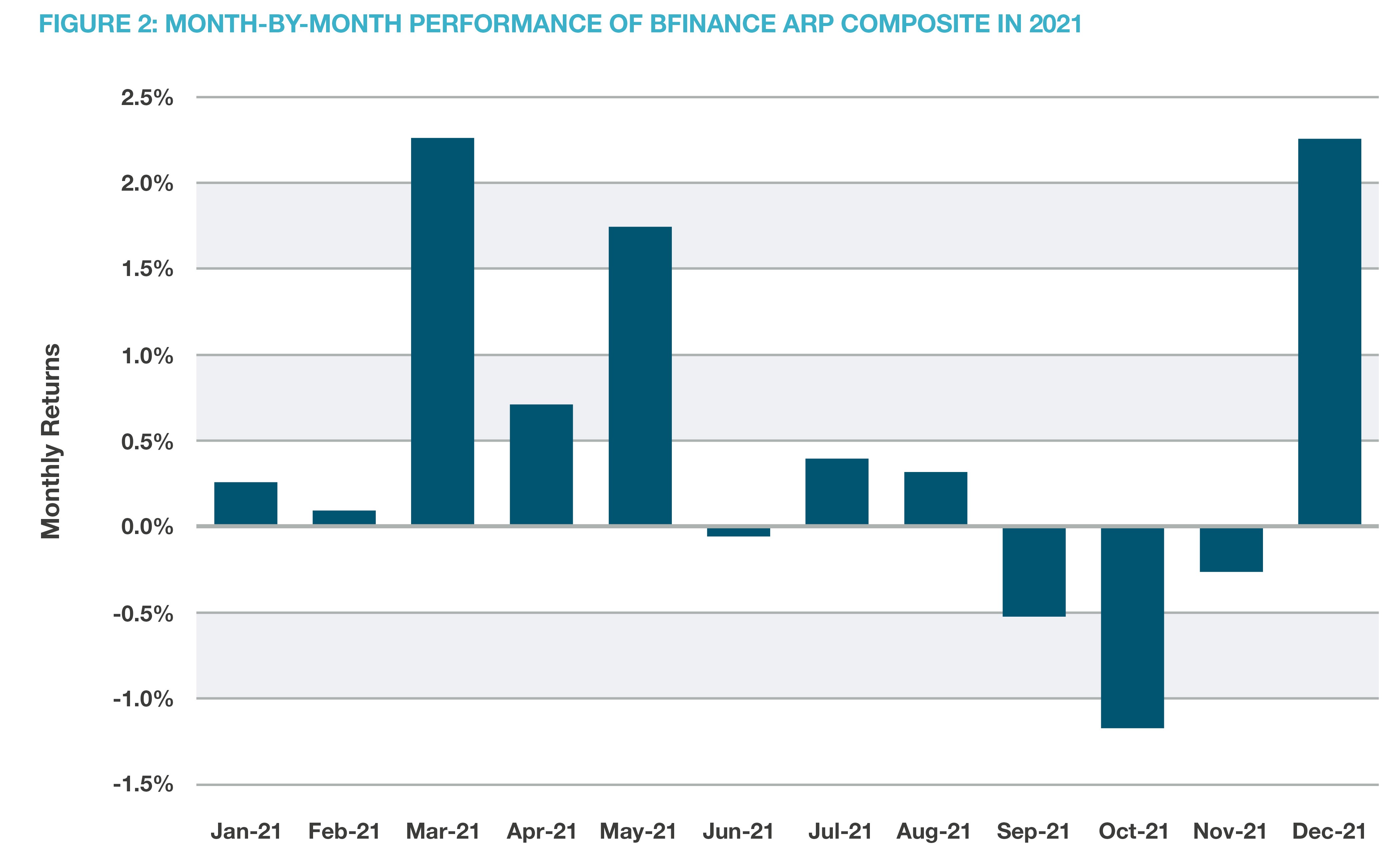

A month-by-month look at returns (Figure 2) shows that the major gains came amid positive sentiment between March and May, and then again in December when Value rebounded and a strong Q3 earnings season bolstered Equity Momentum and Short Equity Volatility strategies. Meanwhile, the most substantial losses came in the risk-off climate from August through September, when China tech sector regulations and COVID infection figures resulted in negative sentiment and increased volatility.

Source: bfinance. An equally weighted net-of-fees composite of ARP managers tracked by bfinance. This is a discretionary composite for reference purposes only; it is not necessarily investible and is subject to change. Strategies that no longer exist/report data are not removed from the composite to reduce survivorship bias.

From a premia perspective, value proved to be a tailwind in 2021, notwithstanding a mid-year pullback and a slight wobble late in the year when the Omicron variant emerged. Trend was another driver of positive performance in 2021, especially in equities (particularly US) andcommodities (oil and natural gas), although the surprise announcement at the June meeting of the U.S. Federal Open Market Committee did unseat some Trend models when the dollar reversed its downward course.

Carry, meanwhile, was a frequent detractor in 2021—particularly in fixed income, as rates experienced a volatile year with economic re-openings, inflation concerns and increasingly hawkish central bank rhetoric spurring aggressive sell-offs. Managers with long exposures at the shorter end of the Australian government bond yield curve in October were particularly affected within their Bond Carry and indeed Trend following strategies.

Broadly speaking, Commodity premia (and particularly Commodity Trend) delivered consistently positive performance across all ARP strategies in 2021. Returns were helped by reinflationary pressures sparked by trade and supply bottlenecks. Agriculture, Base Metals and Energy Markets took turns being core return drivers throughout the year. Dollar strengthening in Q2, OPEC production cuts, and Omicron acted as headwinds (particularly for Commodity Short Volatility) but did not derail a strong year overall.

Finally, the most painful period for ARP returns (the risk-off phase from August to September) was particularly brutal for Short Volatility premia, which had banked the majority of their returns during a more benign H1. This disruption was perhaps to be expected: Short Vol does not typically perform well in volatile markets; as a consequence, investors and managers tend to have a love-it-or-hate-it relationship with these premia.

Manager sub-types

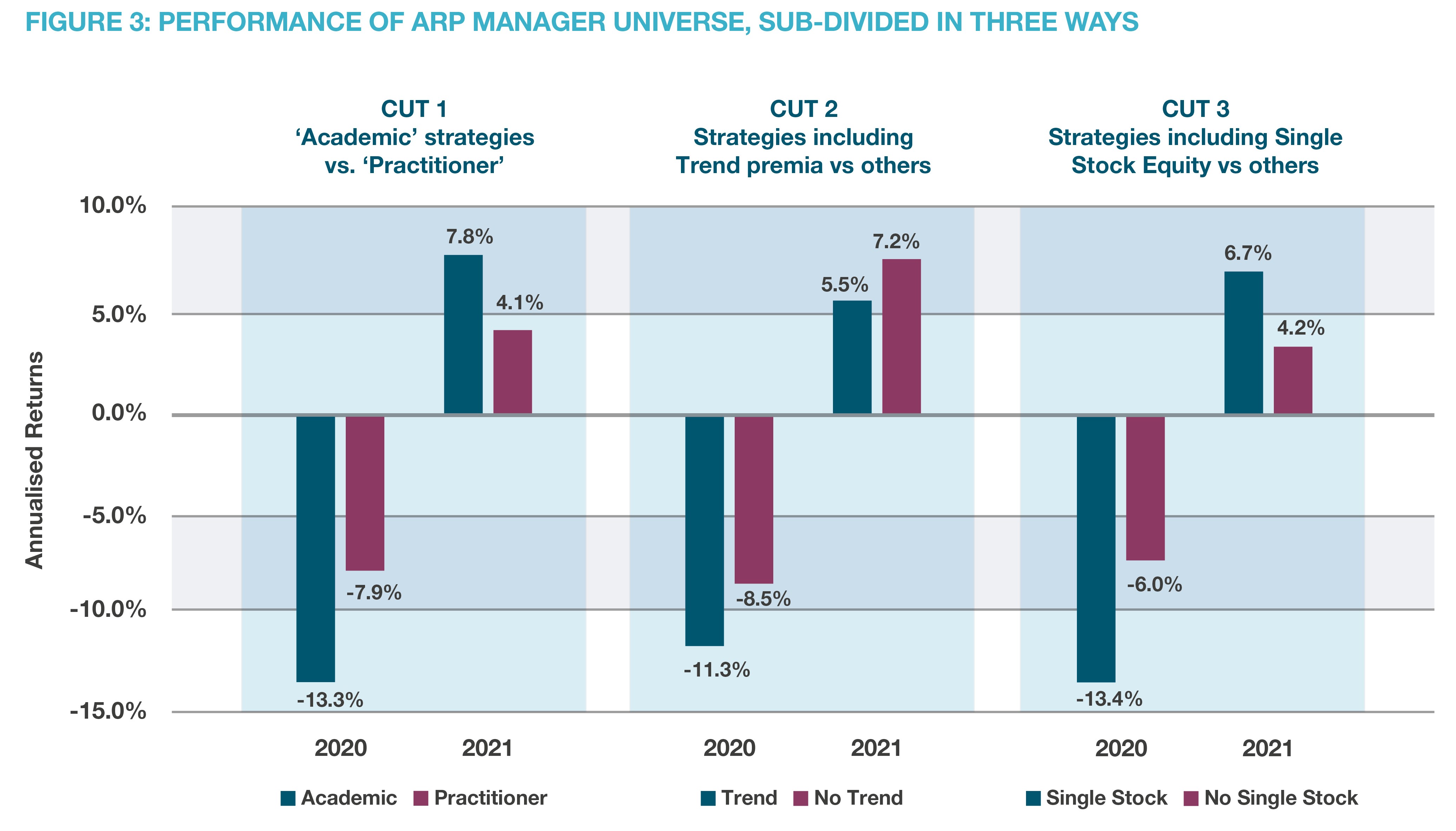

When assessing results through 2020–’21, it can also be helpful to segment the manager universe into relevant subcategories (Figure 3). First, we can divide managers into two camps: one comprises ‘Academic’ strategies and the other features ‘Practitioner’ strategies (a distinction that is explained further below). Second, we can split the universe such that one group uses Trend-following premia, and the other group does not. Third, we can look at those strategies that use Single Stock Equity programmes versus their peers, who do not.

Source: bfinance. All performance data is net of fees.

‘Academic’ strategies are based on classic, academically supported risk premia while ‘Practitioner’ strategies also include systematised versions of alpha-generation techniques that are well-established in the hedge fund sector. The ‘Academic’ group, on average, suffered more pain than its ‘Practitioner’ peer group in 2020 (-13% vs. -7.9% net of fees), as one would expect given its managers’ typically strong exposure to the Value premium, but also recovered most strongly in 2021 (+7.8% vs +4.1% net of fees).

Strategies that use single stock investment programmes, unsurprisingly, suffered more than their peers in 2020 (-13% vs. -6% net of fees)—battered both by the equity sell-off in Q1 and the outperformance of Growth and Low-Quality stocks that followed. Yet this group benefited disproportionately from the Value revival and outperformed its peers in 2021.

Managers that use Trend following premia have underperformed in both years, although we note very substantial outperformance of this group in Q2 2021 due to strong runs in commodities and equities. This overall underperformance may surprise investors, given that trend-following premia have, overall, generated good returns in 2021 (as noted above). There are a number of different reasons for this, including the exposures that these managers have to short volatility premia, single stock equities and commodities.

A sector in revival?

Only time will tell whether ARP will enjoy another surge in investor demand, similar to the trend that we witnessed in 2014–’18. Although recent months have seen strong investor appetite for diversification, this focus has chiefly favoured hedge funds—which have broadly delivered healthy returns throughout the pandemic—and private market strategies.

That being said, these strategies are evidently here to stay. The recent shakedown has produced some healthy consolidation, ousted firms with lower conviction on this strategic approach and provided valuable lessons to support the refinement of quantitative models and processes. We see an ongoing role for ARP within investor portfolios as a source of diversifying return streams at low fees, particularly for asset owners that are not able or willing to access other liquid alternatives, such as hedge funds. In an increasingly uncertain climate for traditional risk assets, this is a sector that still merits attention.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.