English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Anish Butani

Senior Associate, Private Markets

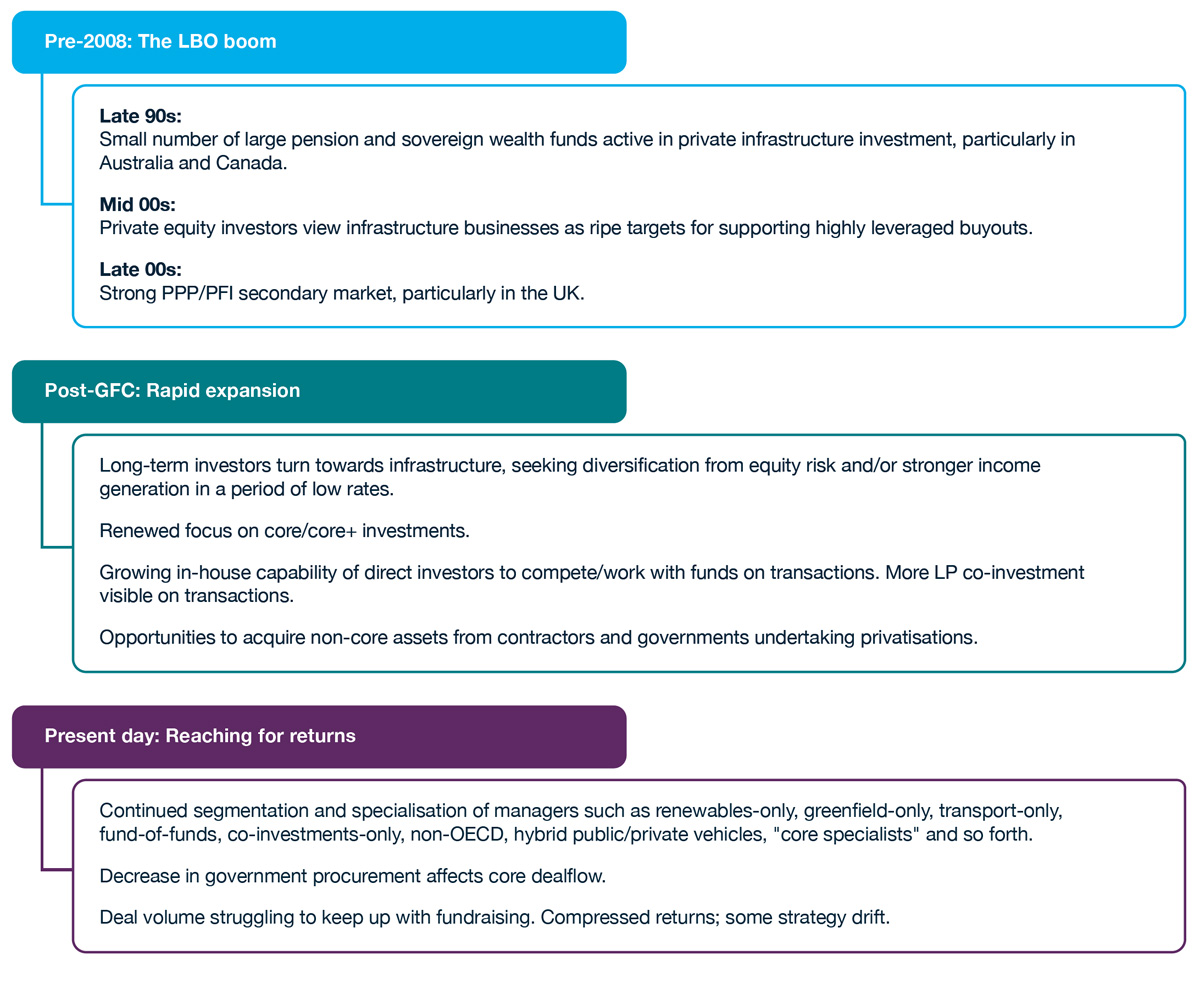

The financial crisis ushered in a new era of unlisted infrastructure investment. Three trends - high appetite for illiquid investments, the desire to reduce equity risk exposure after the lessons of 2008 and the subsequent need for income generation in an era of low rates - converged to create a ‘perfect storm’ of demand.

Dealflow was healthy, buoyed by a stream of asset disposals by financially stretched corporates and privatisations from fiscally stretched governments. Policy-makers from the OECD to the G20 urged pension funds and others to fill the global infrastructure ‘funding gap’.

Yet, if that period of industry expansion might be termed “Infrastructure 2.0,” after the excesses of the pre-crisis LBO boom, we are now in a markedly different phase of the post-GFC era. The practical implications of this shift are explored in a recent bfinance white paper: DNA of a Manager Search: Infrastructure (September 2017).

With direct investors increasingly battling funds for the most prized (typically core) assets in developed markets, the result has been a steep increase in M&A and, by extension, a significant drop in returns. According to Inframation, for instance, M&A deal volume grew 196 percent between 2010 and 2016. Tellingly, non-core infrastructure deals are comprising a larger proportion of the total, particularly in latter years.

ASKING THE TOUGH QUESTIONS

With direct investors increasingly battling funds for the most prized (typically core) assets in developed markets, the result has been a steep increase in M&A and, by extension, a significant drop in returns (see below). According to Inframation, for instance, M&A deal volume grew 196 percent between 2010 and 2016. Tellingly, non-core infrastructure deals are comprising a larger proportion of the total, particularly in latter years.

In order to source the types of deals that will generate the returns they have enjoyed in the past, and which allocators have come to expect, infrastructure managers are adopting new approaches and today’s investors face a far more diverse, segmented universe of available funds and strategies.

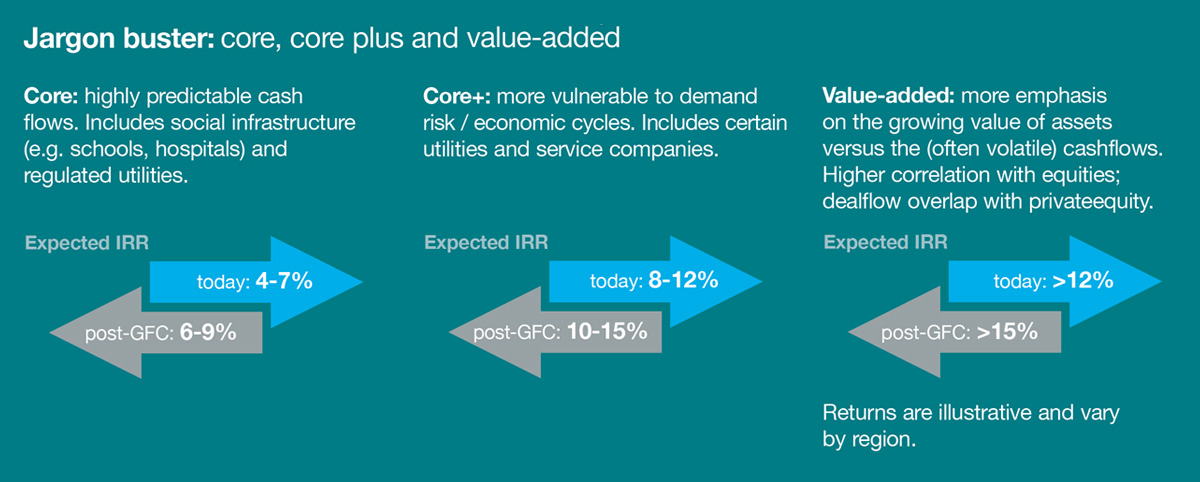

For those selecting asset managers, such as the pension funds and foundations whose searches are explored in DNA of a Manager Search: Infrastructure, the current climate opens up new questions. Is my manager over-paying for assets? Are return expectations too high? Is this fund too large for this strategy now? How can we diversify our infrastructure exposure? Should we be investing more in non-OECD or greenfield assets? Are these deals really ‘infrastructure’ or, given their risk characteristics, more ‘private equity’ in nature?

GREATER VIGILANCE

Whilst none of the developments that we have seen in the industry over the past two years are inherently problematic or undermine the powerful rationale behind infrastructure investment, investors should be increasingly vigilant.

In addition, allocators should routinely interrogate where ‘infrastructure’ (private, listed or debt) is sitting in terms of their portfolio composition, the appropriate benchmark(s), and the objectives which any infrastructure allocation seeks to fulfil. This is a market that has undergone major structural upheaval, and considerable expansion in terms of its scope and definitions, with more and more sub-sectors falling under the “infrastructure” label that would not have been classed as such ten or even five years ago.

In a nutshell? Expectations for risk factor exposures and returns should reflect new realities, not conventional or backward-looking dogma.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.