English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Jamie Duncan

Senior Analyst

Amid the recent rise of Listed Infrastructure and REITs, one particularly notable change is the emergence of strategies that incorporate both of these strategies within one offering.

Manager selection activity for bfinance clients reveals substantial appetite for these hybrid strategies in 2018-19. This is mirrored in growing product availability: there are now nearly 25 funds offering this blend, alongside more than 60 Listed Infrastructure funds – both sectors were negligible before the financial crisis. The true universe for hybrid strategies is even larger, with an element of market-making involved: manager searches conducted by bfinance have received additional proposals with listed infrastructure and REITs providers bringing their strategies together for a combined, customised offering.

Complementary characteristics

Listed infrastructure has largely outperformed REITs over time. Yet the two sectors offer some interesting complementarity as well. While they share certain characteristics, such as stable cash flows and inflation sensitivity, their performance often diverges in different market conditions.

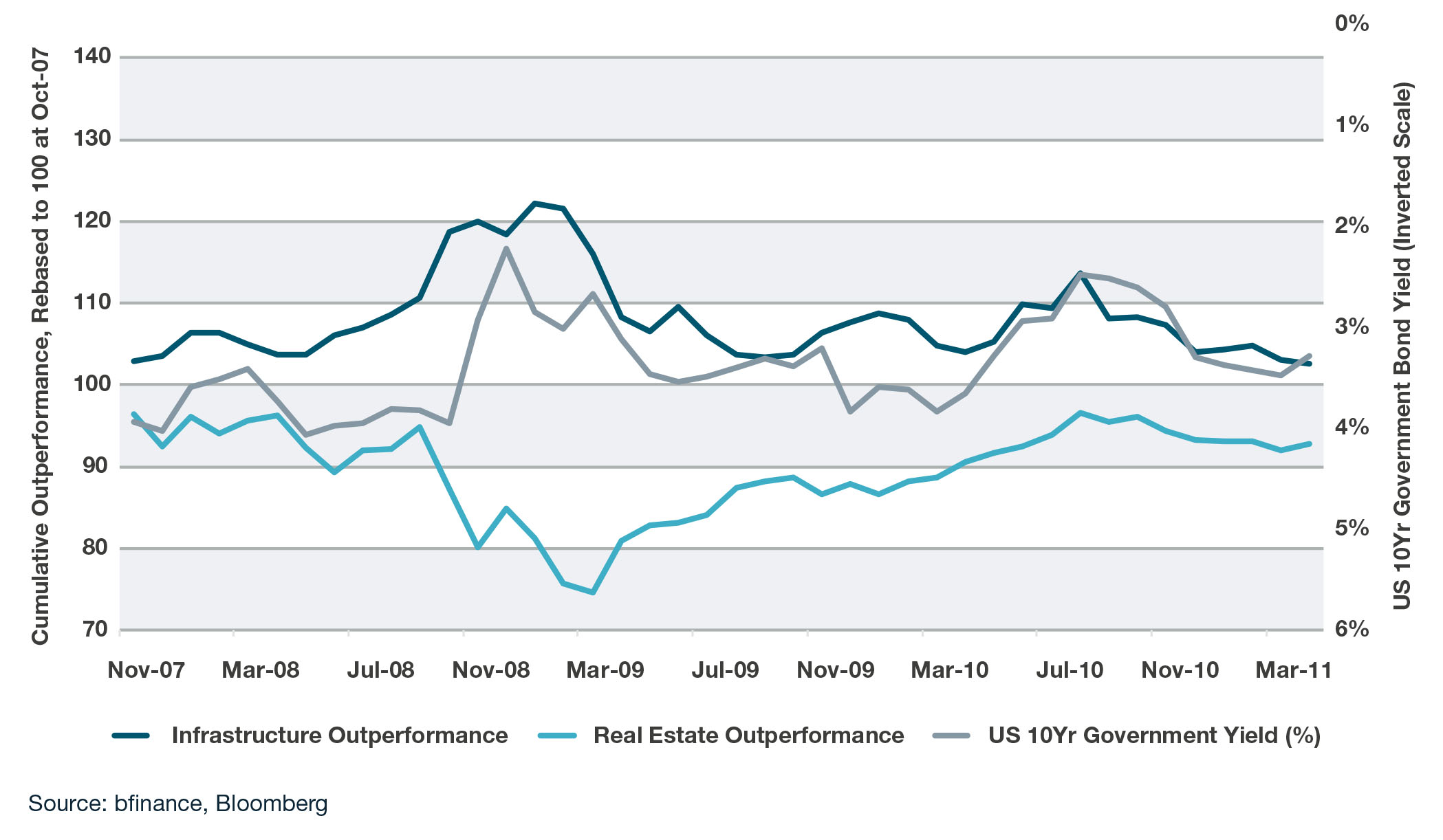

During and since the GFC, listed infrastructure has outperformed equities in all bear markets other than the four-month period that followed the 2013 Taper Tantrum and has produced maximum drawdowns of 7% – half that of the FTSE All World. REITs, on the other hand, underperformed equities during the GFC, with their high leverage at that time making them extremely sensitive to default risk; in the post-GFC recovery, REITs outperformed the global equity market by 45% while listed infrastructure lagged.

Cumulative Performance of Listed Infrastructure, REITs and 10-yr US Treasuries Over the Global Financial Crisis

REITs have become somewhat more resilient since that period, with tighter risk controls and lower gearing; bear markets since the GFC have had less impact on returns. Yet listed infrastructure performance remains more dependent on interest rate changes and subsequent bond yields than listed real estate.

Diversification from equities

There remains considerable debate within the investment community about the extent to which listed real asset performance is correlated with equities or private real assets such as unlisted real estate and infrastructure.

Investors should be careful of the data that is used to make these arguments: different listed infrastructure benchmarks, for example, give a dramatically different profile. We should also be careful of timeframes, with short-term analysis pointing to high correlation with equities while longer-term horizons see that connection declining and the link with private real assets becoming stronger, as shown in bfinance’s 2019 paper REITs: Sector in Brief.

It is increasingly clear that listed infrastructure and REITs do possess characteristics that set them aside from public equities

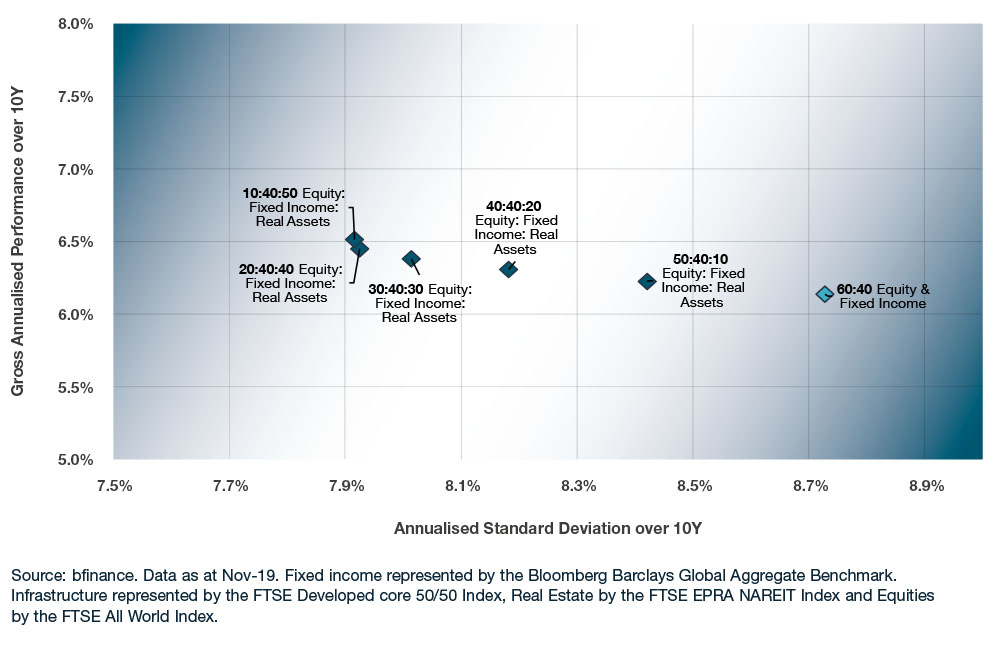

As data and understanding improve, it is increasingly clear that listed infrastructure and REITs do possess characteristics that set them aside from mainstream public equities, such as lower volatility (9.7% over five years for a portfolio of 60% listed infra / 40% REITs, versus 11.7% for the FTSE All World) and higher yield (3.8%, almost double that of equities). The figure below illustrates the effect of an incremental 10% substitution from the equity portion of a classic 60:40 equity:bond portfolio toward listed real assets (split 60:40 to listed infra:REITs). This data, albeit only for the last ten years, showed a reduction in volatility, slightly higher returns and considerably better risk-adjusted returns.

ALLOCATING FROM EQUITIES TO 'LISTED REAL ASSETS' (LISTED INFRA AND REITS)

Implementing hybrid strategies

Managers running products blending listed infrastructure with REITs take very different approaches. Models include the real assets ‘one-stop-shop’ responsible for security selection across both asset classes, the ‘internal fund-of-funds’ dynamically allocating to existing real estate and infrastructure strategy sleeves managed by the firm, and the ‘simple combination portfolio’ offering a static exposure to each asset class.

The approach is often influenced by corporate structure, culture and history. We see a strong trend for managers with a background in REITs expanding to cover listed infrastructure, although we do also see listed infrastructure specialists moving towards REITs, as well as a number of equity houses and other firms developing dedicated listed real asset capabilities.

Relevant managers attribute up to 20% of their outperformance to tactical allocation between the two asset classes

These structures influence team decision-making processes, particularly the asset allocation to the two sectors. It’s important to note that a tactical approach to these weightings can improve potential outperformance: recent engagements show that relevant managers attribute up to 20% of their outperformance to tactical allocation between the two asset classes.

Managers use a variety of different processes and techniques to identify relative value: some emphasising quantitative models while others focus on capital market trends, geopolitical risks and supply/ demand drivers. There’s also huge variation in rebalancing frequency, from daily to monthly or even quarterly. More insight on these strategies can be found in the extended paper: The Rise of Listed Infrastructure and REITs.

Conclusion: demand set to continue

Demand for listed real asset strategies is expected to remain strong in 2020 as investors seek diversification and late-cycle flexibility, and we expect that hybrids will continue to feature strongly alongside the standalone listed infrastructure and REITs activity. Customisation is increasingly important, with investors looking for separate managed accounts that explicitly complement the investor’s existing portfolio in terms of geographies, sectors and exposures.

This article is a shorter extract from new white paper: The Rise of Listed Infrastructure and Real Estate.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.