Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Pravir Sharma

Associate - Diversifying Strategies, bfinance

The see-sawing stock markets of 2018-19 provide an interesting window in which to examine the performance of “diversifying strategies.” Below, we scrutinise the results from more than 45 Alternative Risk Premia managers to find out what they delivered and why.

Most Alternative Risk Premia managers pitch their tents firmly in the camp of equity diversification. Low beta to stocks represents one of the sector’s primary selling points: these are intended to be “all-weather” systematic return streams. While there are some strategies with a more directional profile, such as those making use of the short volatility factor, these represent the minority.

As we shift towards a more volatile (or perhaps more “normal”) climate, substantial market fluctuations give an interesting opportunity to see how this still relatively young group of strategies perform during periods of significant equity revaluation. While diversification is certainly not intended to be a “hedge,” against losses, and should be judged over the long term rather than short horizons, results during such periods can be a cause for concern among some allocators.

Returns under scrutiny

So what does 2018-19 ARP performance tell us? At first glance, the picture is somewhat problematic.

According to our assessment of more than 45 ARP managers, 2018 was the worst year of live performance data on record, with an average loss of 4.2% after all costs, on a 6% vol adjusted basis. Only 14% of them delivered positive returns for the calendar year. At the same time, 2018 was negative for the global equity market, which fell more than twice as hard (-8.7% based on MSCI World before fees). The first quarter of 2019 has seen ARP managers regaining ground (+1.8% on a 6% adjusted vol basis, with 87% of managers in the green). This rebound has been strongly associated with the trend-following, fixed income momentum, carry and short volatility factors, with trend continuing to support solid performance in the first part of Q2. Yet this positive period also saw equities, fixed income and commodities all rise.

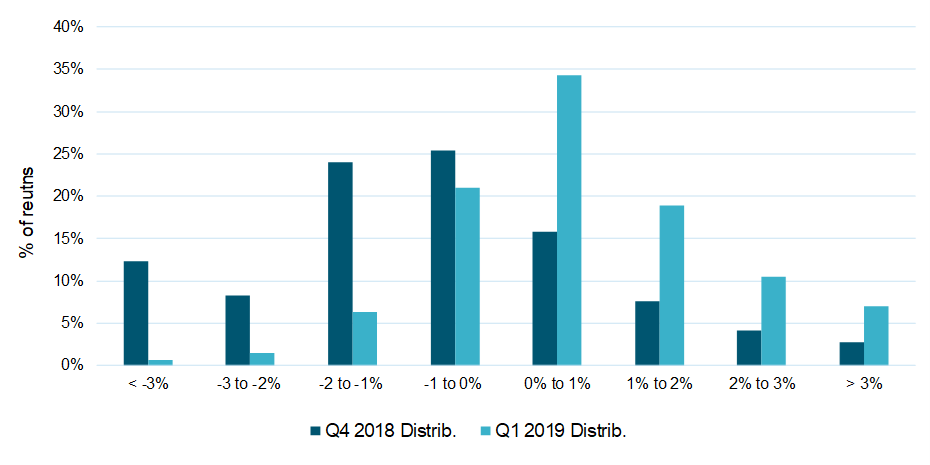

The average ARP manager only lost 2% during Q4, while equities fell around 13%

A closer examination of the worst period for equities – the fourth quarter of 2018 – brings a more positive message. During the October-December window, the average ARP manager only lost 2% while equities fell around 13%. This is perhaps more reflective of the results that we would expect ARP strategies to deliver in significant “risk-off” periods.

Indeed, the worst month for ARP managers was not in the fourth quarter but in the first: February 2018 provided a perfect storm for these strategies, with particularly severe losses to the trend-following and volatility factors (Click Here to read What Volatility in Q1 Revealed about Alternative Risk Premia).

The sector’s overall performance has been somewhat stifled through the past year. Most notably, the equity value factor has been out of favour for four out of the last five quarters, with Q4 being the exception.

The diversification characteristics, however, remain exceptionally healthy. The rolling twelve-month beta of ARP managers to the MSCI World was only 0.07 at March 31st 2019 and also 0.07 at December 31st 2018 – right in line with the long-term figures that have drawn so many investors to this space since 2011. From an R-squared perspective, equity markets explain only 30% of the variation in returns for ARP strategies for the twelve months to March 31st. This data reinforces an essential point: very low beta and moderate Sharpe ratios do not inherently imply that performance should be positive when markets are negative or vice versa.

A maturing industry

The period of relatively weak performance has already had some impact on the funds and managers offering these strategies. Those that came late to the party have struggled to raise assets in what has become an increasingly competitive space, with more than 60 firms now jostling for position. In a few cases, the combination of poor returns and stagnant asset growth has led to closures as the products have become economically unviable.

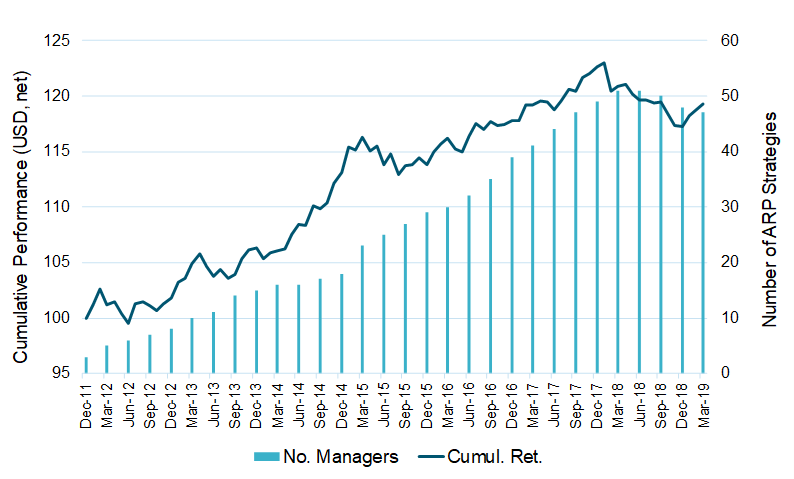

Figure 2: Number of strategies and cumulative performance

Newer entrants largely sit at the more complex end of this space. These do not tend not to offer strategies based purely on the most familiar academically established risk premia, for which there are already multiple players with long track records. Instead, they differentiate themselves through sophisticated portfolio construction and the use of “practitioner-type” risk premia, which exploit behavioural tendencies rather than perceived long-term market anomalies.

The first phase for the ARP sector, marked by a rapid proliferation of strategies of all shapes and sizes, has passed. This no-longer-nascent industry is now in its second phase as it undergoes consolidation and maturation. Its future growth trajectory will undoubtedly be influenced by how these strategies continue to perform amid more volatile market conditions and, in particular, in the event of a severe downturn. Recent ARP results, while somewhat muted, give strong grounds for positive expectations.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.