Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Anish Butani

Senior Director, Private Markets

Infrastructure, as an asset class, is now grappling with something of an identity crisis. Does it offer the same promise that underpinned demand a decade ago?

This article was originally published by Pension Fund Service in Spring 2020.

The last decade has seen an influx of institutional capital, with strong growth in fundraising (Figure A) and many pension funds creating standalone allocations to this sector. The attractions have been well-rehearsed and performance over this period has not disappointed: infrastructure equity funds have delivered healthy yields in an era of low rates, with substantially less volatility than equities. These attractions have, in many markets, been reinforced by encouragement – or even pressure – from governments and pension regulators to deploy capital to the asset class. Indeed, the origins of LGPS pooling in the UK were heavily influenced by policymakers’ desire to see pension funds filling the infrastructure spending deficit, with consultation suggesting that larger pooled entities would be better equipped to invest in this asset class.

Yet, with large swathes of infrastructure now in the hands of private investors, does the asset class still offer the same ‘promise’ that underpinned demand a decade ago? In this article we look back at key changes, consider the future, and note issues that investors should be thinking about when selecting strategies and asset managers within a changing industry.

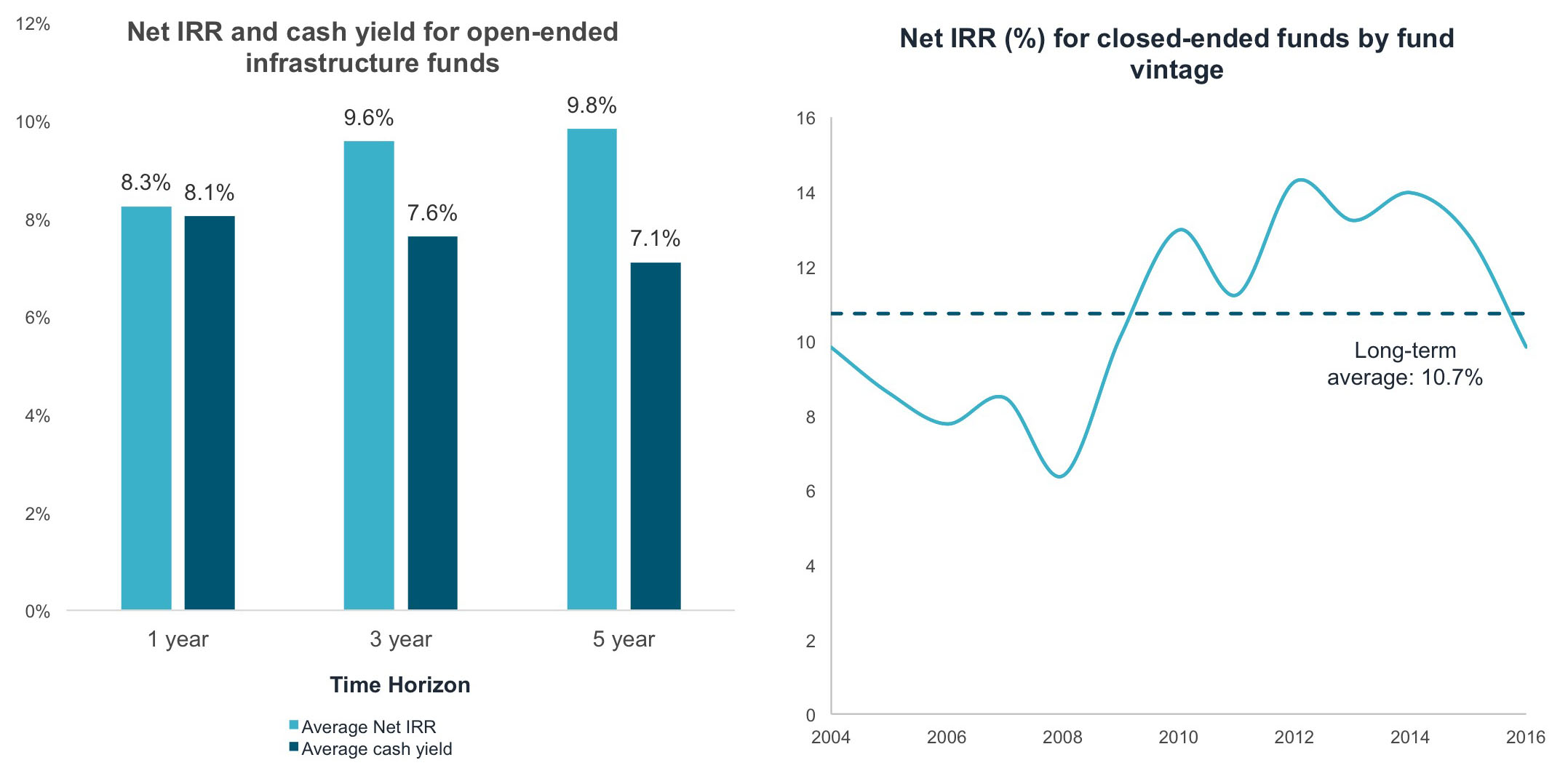

FIGURES A AND B: INFRASTRUCTURE FUND IRR AND CASH YIELDS

Source: bfinance

To some extent, the last decade has been a story of impressive innovation in this sector. Yet innovation comes at a price. For pension funds expecting an 8-10% return from infrastructure equity (before fees), it may now be necessary to consider a fundamentally altered risk/reward profile: one which is somewhat more private equity-like in nature, with less emphasis on reliable cycle-resistant yields and more focus on total returns. In this new environment, pension funds should exercise care in manager selection and seek improved diversification within infrastructure and real asset portfolios.

New fundamentals, old expectations?

Today’s supply-demand fundamentals are undoubtedly different, with stiffer competition for assets, dry powder at record highs and reduced availability of true “core” deal-flow.

On the supply side, there has been a decline in the availability of assets that allow investors to underwrite a truly robust expectation on yields, be it in the form of subsidies, Government-backed availability payments or other forms of contractual level revenue-support. First “social infrastructure” and then “renewable infrastructure” received hefty state backing – backing which has been substantially curtailed (see Investing in Renewables: Navigating the Transition, bfinance, 2019). The old breed of infrastructure investors relied heavily on quasi-monopolistic or government-backed revenue streams, using brownfield assets or those where the public bodies took responsibility for construction and development risks. Today there is substantially less political appetite for this type of financing model. Indeed, in the era of low borrowing costs, Governments are becoming emboldened to self-finance more infrastructure projects, as demonstrated by the latest spree of announcements in the 2020 UK Budget.

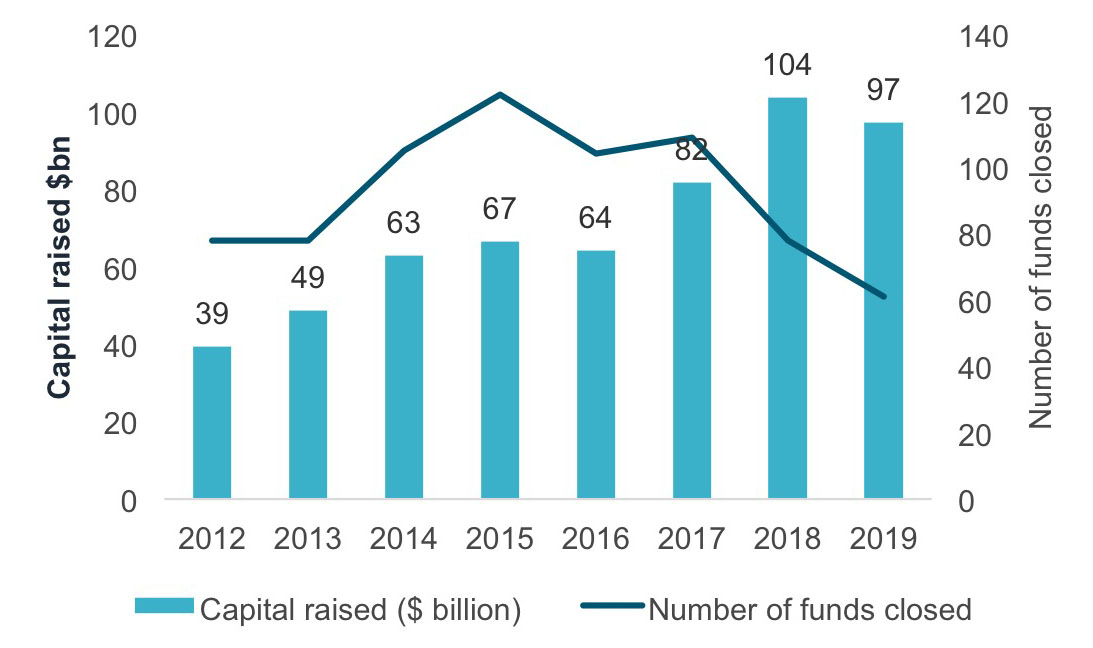

FIGURE C: ANNUAL CAPITAL RAISED BY INFRASTRUCTURE EQUITY MANAGERS AND NUMBER OF FUNDS CLOSED

Source: Infrastructure Investor

The nature of demand is also changing – and not just due to the rising volume invested in funds. Where core infrastructure assets are available, they tend to be targeted by the increasingly long list of direct investors (such as SWF, pension funds and insurers investing for their own balance sheets). Direct investors are often seen to accept a lower return than a fund would be able to tolerate. This type of investor may also be able to hold such assets for an extremely long time, with a focus on yield rather than entry and exit valuations. As such, they can undercut the GPs who usually need to make, at a minimum, 7% net of costs (8-10% gross).

Yet, notwithstanding the evident squeeze on fundamentals, managers have not significantly lowered expectations on successive similarly-branded funds through the years. Instead, we see a change in content, with GPs leaning towards different strategies and sectors in order to ‘bridge the gap’ between expectations and opportunities.

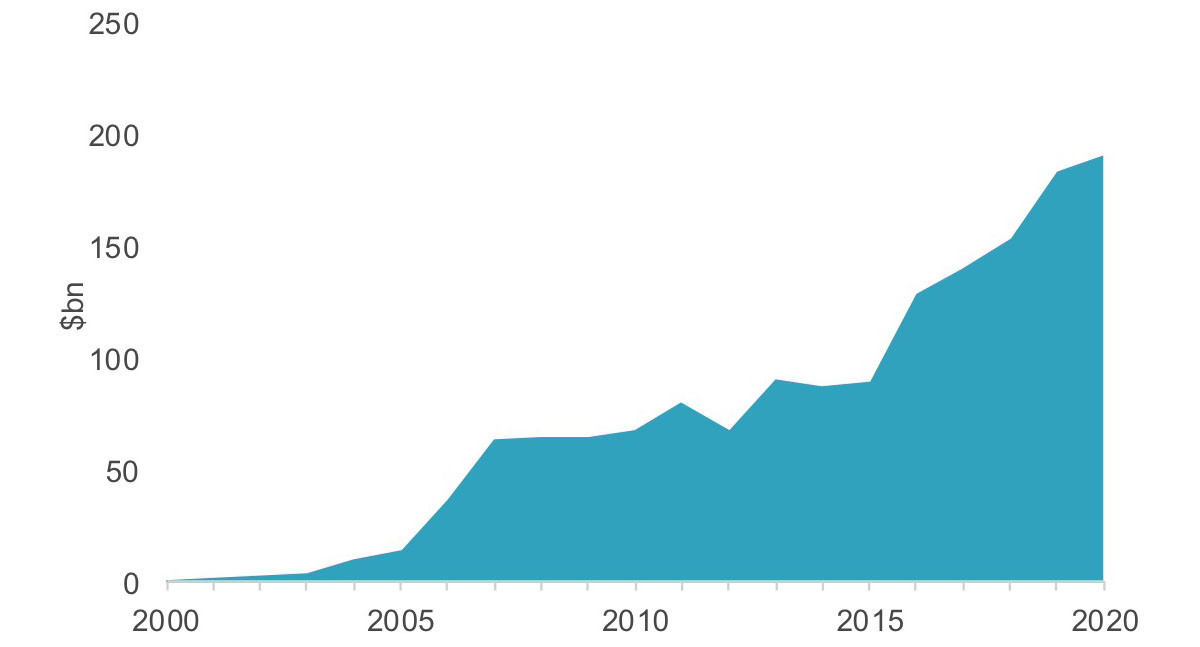

Source: Prequin

This shift reflects two underlying drivers. The first is investors’ need for diversification: having built out a central infrastructure portfolio comprising core-to-core-plus exposure, schemes are looking to complement that with differentiated strategies. The second driver is the changing nature of that central core/core-plus element, as explored above.

One particularly interesting category where we have seen a big rise in product launch activity from a low base is infrastructure mezzanine debt or infrastructure direct lending.

While this added diversity is theoretically helpful, through another lens it can be viewed as a symptom of asset gathering, with managers broadening their range of products across equity and debt to maximise fundraising during an era of strong inflows.

One particularly interesting category where we have seen a big rise in product launch activity from a low base is infrastructure mezzanine debt or infrastructure direct lending, with return targets ranging from about 8% to nearly 15%. This new, higher-returning breed of debt strategies is being marketed on the premise of equity-like returns with more downside protection. Yet it is crucial to bear in mind that debt portfolios are not necessarily more resilient during downturns.

Three themes: greenfield, technology and ESG

As noted above, mainstream infrastructure equity funds are using different strategies and sectors as they seek to meet investors’ needs and expectations. When looking at those changes, three key themes stand out among the rest:

- the rising use of greenfield investment within portfolios;

- the greater relevance of new technology, both for the emerging “digital infrastructure” sub-sector and for value creation in more conventional infrastructure; and

- the changing dynamics of ESG investing in infrastructure, whether in thematic strategies such as renewable energy infrastructure or in generalist funds.

THEME 1: GREENFIELD GOES MAINSTREAM

Manager research data from bfinance strongly indicates that managers are taking more greenfield risk than before in funds with the same return expectations.

However it is worth noting that not all greenfield assets are born equal. In some cases, these greenfield projects are described as “build-to-core,” where opportunities exist to generate strong risk-adjusted returns with a very high yield component by acquiring assets “at cost,” particularly where those assets offer highly contractual cash flows. In other cases, bfinance has observed managers developing and constructing assets that are subject to greater business or re-contracting risk: as such, the risk not only relates to taking a project through construction (such as building a fibre broadband network) but competing in the market to add new customers.

TREND 2: THE RISE OF TECHNOLOGY

It is almost impossible to pick up an infrastructure investment magazine these days that does not have substantial focus on technology. The theme encapsulates two separate developments. The first is the increasing use of non-traditional sub-sectors, among which “digital infrastructure” (such as data centres, high-speed broadband networks and so forth – the infrastructure of the digital age) is particularly prominent. The second is the greater reliance on value creation (versus yields) in more conventional infrastructure assets: it is expected that artificial intelligence and other new technologies can substantially increase the productivity or efficiency of airports, roads and many other types of infrastructure asset.

The digital infrastructure boom is particularly fascinating from the perspective of core versus non-core supply. Although this is area clearly a political priority across many countries – and may well be the big infrastructure trend of the 2020s – this sector is not supported by the types of subsidies or risk-sharing arrangements that characterised previous waves of infrastructure investment. Areas such as fibre broadband involve huge capital expenditure and development risk: while that should be compensated over the very long term, a ten-year investment horizon may actually be too short for investors to reap the benefits.

Digital infrastructure does raise some interesting challenges from an ESG perspective. Data centres, for example, account for relatively high emissions due to their high energy usage. Meanwhile, there is very little way to accurately quantify the beneficial impact of outcomes such as, for instance, reduced employee travel due to better digital connectivity.

TREND 3: ESG DIMENSIONS

The ESG theme within infrastructure investment at present can be thought about in three ways: the integration of environmental, social and governance factors into the investment process, the use of thematic strategies such as renewable energy infrastructure, and the increasing demand to measure “impact” (social and/or environmental) from either of the above.

In the first category, we see infrastructure managers increasingly putting out large amounts of commentary on ESG issues and featuring ESG heavily within pitchbooks or other materials. We see groups like GRESB rating managers’ ESG credentials. Yet much of this activity is relatively superficial. ESG is not a tickbox exercise – except when you measure it! Metrics such as the existence of an ESG person on staff or paid-for memberships are poor barometers of ESG sophistication. The true test of a manager’s regard for ESG should be evidence based: to what extent is ESG demonstrably being considered when assets are being acquired and during the subsequent asset management period? As illustrated in the digital infrastructure comments above, these assessments are far from straightforward and should be handled with care and sophistication.

Renewable energy infrastructure has been the dominant “impact infrastructure” investment of the last decade. Yet the asset class that emerged to foster the energy transition is itself in transition. Ten years ago, governments were offering subsidies (Europe) and tax credits (US) to support investment. Long-term feed-in tariffs and Renewable Obligation Certificates (“ROCs”) helped to provide an almost bond-like income stream. Today, investors are more exposed to merchant power price risk or, in the case of Purchase Power Agreements, corporate risk. As this happens, we may see a bifurcation with this sector separating from the broader infrastructure space, and being viewed as more akin to an “energy play” than an infrastructure one.

Looking ahead: the new generation?

While investors consider these developments, and the fundamental practical questions they necessitate, another, less obvious, development requires equally serious consideration. The changing face of infrastructure investment is soon to be reinforced by the changing faces of infrastructure managers – one that goes beyond the continuation of strategy launches and team spin-outs that we’ve seen in recent years. Many of the founders and leaders who launched infrastructure funds in the last ten-to-fifteen years are likely to start thinking about exits – not just fund exits, but their personal exits from their firms. If done well, these departures could unleash a new generation of leadership that is incentivised to continue delivering performance. If done badly, the departure of senior management personnel has the potential to leave behind a trail of organisational instability and the loss of upcoming talent.

Asset allocators should focus heavily on potential generational changes as they assess the middle management tier, succession plans and corporate stability. Culture, in particular, should not be underestimated: as the familiar saying goes, ‘culture eats strategy for breakfast.’

Infrastructure investment undoubtedly has a bright future, and a lasting role within pension fund portfolios, as it moves towards the new generation. Successful investors will employ careful strategy and manager selection, keeping a sharp eye on current industry realities and exercising caution with backward-looking assumptions.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.