English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

Part of the bfinance Sector in Brief series, this paper offers a swift digest of market and manager developments.

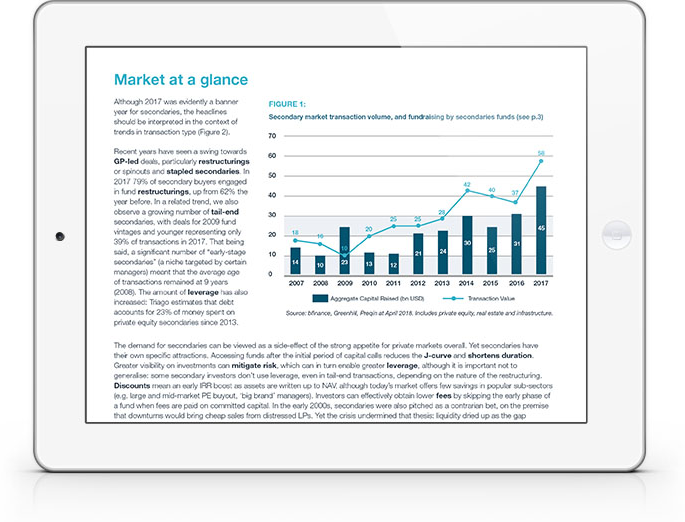

While the large increase in transaction volume, strong fundraising and high prices have been widely reported, those headline trends should be interpreted in the context of underlying shifts in transaction types, buyers and sellers.

Recent years have seen a swing towards GP-led deals, particularly restructurings or spin-outs and stapled secondaries (see the “Jargon Buster”), as well as greater use of leverage. While private equity deals dominate the data, infrastructure, real estate and private credit secondaries represent an increasingly substantial slice. Greater geographical diversification is also evident.

WHY DOWNLOAD?

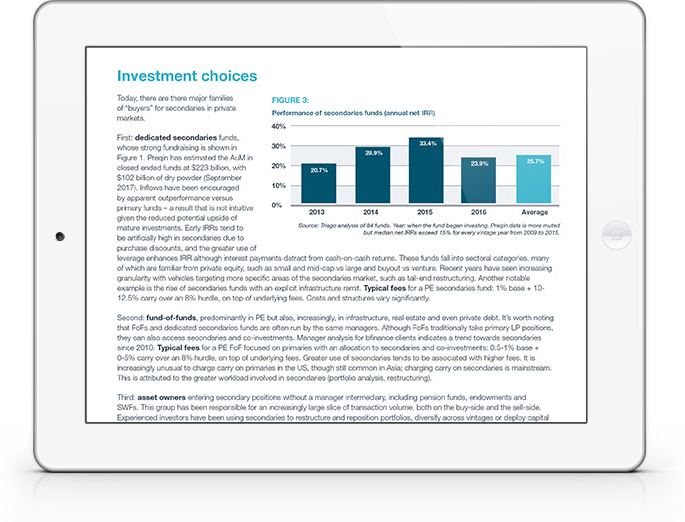

As well as outlining key trends in the market, the paper also tackles developments among three major buyer types: asset owners such as pension funds, dedicated secondaries funds, and fund-of-funds focused on primaries that increasingly allocate a portion to secondaries and co-investments.

For the most part, the current manager response to today’s high pricing and dry powder in secondaries revolves around tighter specialisation, greater complexity and, while generalisations should be avoided, higher leverage.

Manager specialisation is, perhaps, the key trend. In addition to the broad ‘flagship funds,’ we now see a multiplicity of vehicles targeting specific niches.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.