Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada) - Corporation, Benelux

- Q1 2022

- Private Equity, Global

- Approx. EUR 300 million

- Design a private equity portfolio and transition

- Strategic Portfolio Design

Our specialist says:

This institution’s direct investment aspirations and the explicit need for income during the transition period were highly relevant to portfolio construction. ‘One size does not fit all’ in portfolio design and consultants must be flexible in their thinking in order to meet clients’ objectives.

Client-Specific Concerns

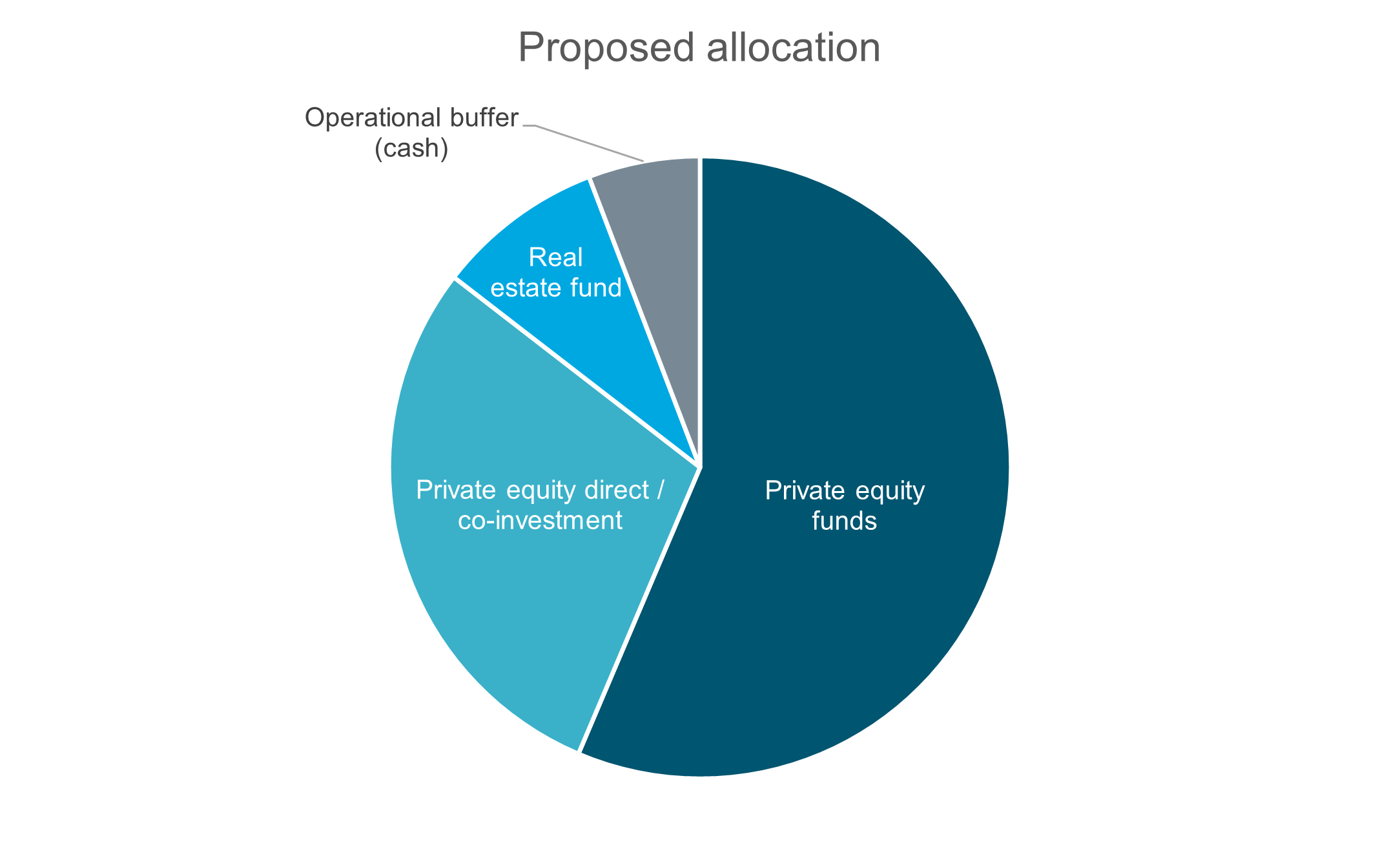

A Benelux corporate was seeking to create a private equity investment unit, making productive use of their strong cash position and bringing potential strategic benefits to the firm. As well as investing in private equity funds, the client was seeking to establish in-house capability to invest (and/or co-invest) directly in unlisted companies: the ‘indirect’ funds portfolio should both generate appropriate returns/diversification and facilitate the development of the direct portfolio, with GPs providing ideas, expertise and co-investment opportunities. In terms of deployment, the intention was to create a transitory portfolio of liquid investments and then shift capital towards illiquid investments over time: the liquid portfolio should provide income to cover operational expenses and allow the organisation to meet the illiquid strategy capital calls as easy as possible.

They engaged bfinance as an advisory partner that would bring institutional experience with portfolio design and fund selection, but with a highly tailored approach that would fit their specific strategic objectives. bfinance would also assist in the design of this transitory portfolio and relevant cashflow planning. In early discussions it became evident that the client would be willing to consider a wide range of fund strategy types: primaries and secondaries; single-manager funds and fund-of-funds; private equity and perhaps also a limited amount of real estate if appropriate.

Outcome

- Building an indirect funds portfolio that supports an internal investment programme that invests into companies directly. Researchers advocated a differentiated focus between European funds (which should supply information and co-investment opportunities for the ‘home market’ region) and international funds (offering good diversification across strategies and vintages, but not needing to facilitate direct investment). This made single manager funds more appealing in Europe and fund-of-funds more interesting internationally. With internally-managed investments expected to be concentrated and irregular, it was particularly important that externally-managed investments provided regular deployment of capital and diversification (though not over-diversification!).

- Developing direct investment capability. Given the level of resourcing and the portfolio size, bfinance recommended starting with syndicated co-investments and then moving towards underwriting direct co-investments as the team’s capabilities and resources increase.

- Allocating to European core real estate via an open-ended fund. In order to alleviate some of the pressure to generate income and add a degree of quarterly liquidity that might support unforeseen future events, the team proposed the inclusion of a conservative European core real estate allocation.

- Transition portfolio: While all major income generating asset classes were considered for the transition portfolio, researchers ultimately recommended a base-layer of short duration investment grade credit, given the risk tolerance and income requirements.