English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Justin Preston

Senior Director, Head of Equity, Public Markets Investment Advisory

The year was 2009. Amid a climate of investor cynicism, disappointment and self-examination, two papers were published that would fundamentally change the way that the investment industry viewed active equity management.

Clients have clamoured for 'real active managers' and managers have marketed themselves accordingly.

INVESTMENT MANAGEMENT FEES: NEW SAVINGS, NEW CHALLENGES (BFINANCE, 2017)

The first, which bore the deceptively dry title “Evaluation of Active Management of the Norwegian Government Pension Fund Global,” catapulted into mainstream consciousness the notion that investors’ equity returns could largely be attributed to a set of well-known risk factors such as value and momentum.

Ang, Goetzmann and Schaeffer ushered in a tidal wave of related academic research that, among other things, underpinned the emergence and rapidly increasing popularity of Smart Beta. Few equity managers in 2009 could have told you the factor attribution of their portfolios; today, products such as Style Research’s Skyline have become almost ubiquitous. Various managers even base their more sophisticated marketing efforts on their low combined exposures to these factors, claiming a high degree of “idiosyncratic” or “stock-specific” risk.

In the second, “How Active Is Your Fund Manager? A New Measure That Predicts Performance,” Martin Cremers and Antti Petajisto first advanced the concept of Active Share. Although the argument that high Active Share is correlated with positive outperformance has since been undermined by other studies, which instead found that high active share was merely linked (as intuition would suggest) with high performance dispersion, the metric has become extremely popular.

In 2016-17, low active share scores – or “closet tracking” – regularly dominated headlines the asset management press. Morningstar’s influential paper Active Share in European Equity Funds branded a fifth of European large cap funds with the “closet tracker” label. Managers have advertised their high active share percentages as a testament to their active credentials.

On a related note, investors have also paid significantly more attention to turnover numbers, tracking error and concentration over the past few years, as well as showing increasing appetite for unconstrained or benchmark-agnostic strategies.

There is no doubting the influence of factor attribution analysis and active share percentages on investor consciousness. Investors have been increasingly vocal in recent years with demands for ‘real’ active managers and refusal to ‘pay for beta dressed as alpha.’ There is also no doubting the instinctive appeal of attractive, comprehensible graphs that appear to reveal what managers are “really” up to and may even, at the extreme, present a case for considering cheaper, systematic forms of investment. It’s a tantalising prospect.

But how helpful is this data – really – in selecting active equity managers that will outperform going forwards? The answer, at least according to equity manager data analysed here at bfinance, is: “handle with care.” Neither a Skyline analysis nor an active share number are hugely meaningful without a deeper understanding of a manager’s approach, especially when viewed at a single point in time. Active share, style exposures, information ratio, turnover, tracking error and the rest are all useful metrics, to a certain degree. Yet none of them in isolation hold the key to establishing what a ‘real active’ manager – much less a good active manager – looks like.

For example, on first inspection, a manager may appear to have engaged in “style drift” from value towards growth during recent years, but closer inspection can reveal a consistent focus on “Quality.” Likewise, a disciplined Buy-and-Hold manager with low turnover may appear to have changed their risk exposures when the team has retained appropriate discipline amid evolving markets.

Meanwhile, virtually all active global equity managers vying for significant institutional mandates through bfinance these days have high (>70%) active share percentages and, it’s worth noting, there is no statistical evidence in our research that those at the lower end of the active share spectrum are underperforming those at the upper end. The now-conventional wisdom that managers with higher active share, lower turnover and higher concentration will tend to do better is flawed at best and misleading at worst.

When it comes to performance and how ‘active’ the manager appears to be, there are some intriguing suggestions that emerge from recent manager analysis.

The first: unconstrained or benchmark-agnostic long-only active equity managers do appear to be outperforming their benchmark-relative counterparts over the past one and three years, based on the suitable strategies available for the large ($50 – 300m) institutional mandates in 2017. This is a preliminary finding, based on in-house manager research, which we will seek to explore and question with further analysis, especially since the definitions and distinctions are not straightforward.

The second: emerging market equity managers with lower portfolio turnover appear to be outperforming their higher-turnover competitors. This is a finding that has been noted elsewhere, such as Churn is Not Necessarily Burn: Debunking the Myths of Portfolio Turnover (Schroders, 2017).

The third: as a group, equity managers appear to demonstrate rather lower tracking error over the past year than has historically been the case. Yet this doesn’t mean a decline in “activeness” by any means. Instead, it stems from the very low volatility in the equity market during the recent period, with stocks largely moving in tandem.

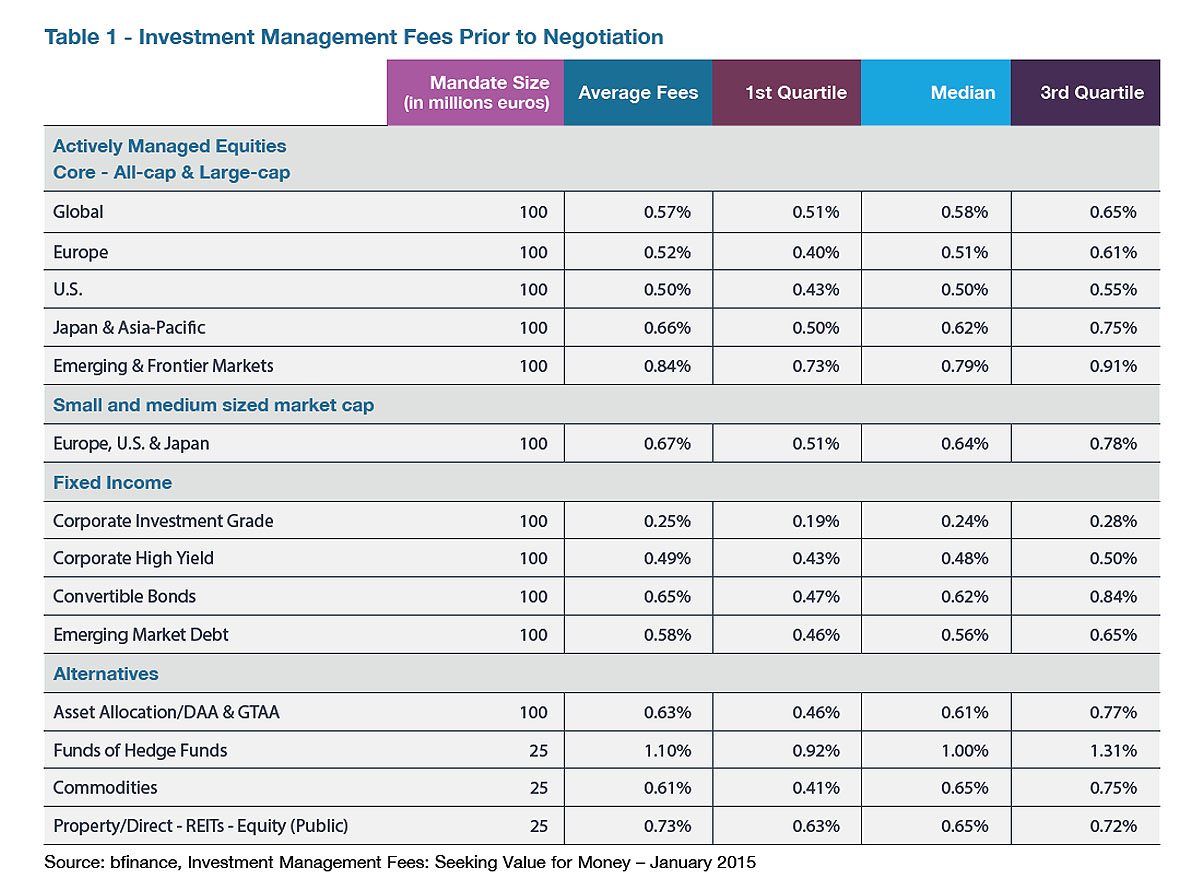

Managers, of course, have another very strong incentive for showcasing their active credentials, especially when it comes to their factor exposures: fees. Active managers in the more systematic sub-sectors of the universe have been under the most severe pricing pressure. Low volatility manager fees, for instance, have compressed by 25% since 2010 (Investment Management Fees: New Savings, New Challenges, bfinance, 2017).

Conversely, despite the effervescent rise of passive investing and an increasingly cost-conscious clientele, the fees for broader global active equity mandates have only fallen by a marginal amount. The median quoted fee for active global equity searches declined by only 8% between the pre-09 period and 2015-17, moving from 61bps to 57bps. (Readers should note that these figures are drawn from quoted fees and that the average negotiated discount for equity searches has been 12%.)

Although some interesting and innovative fee structures have been developed that enable better economics for investors, the much-touted broader trend towards performance fees has stalled as investors largely continue to prefer the simplicity of management fees and question – sometimes as a result of bitter experience – the extent to which performance structures really facilitate alignment.

All in all, this represents remarkable resilience from a price perspective, given the circumstances Providers’ efforts to present themselves as ‘the real active managers,’ whether spin or substance, have - by this financial measure at least - been successful.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.