English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Chris Stevens

Director, Diversifying Strategies

Hedge fund managers have long defied the asset management industry’s drive toward greater consideration of ESG-related investment factors, but investors’ shifting priorities are sparking change. As demands for accountability increase, many asset owners are encouraging their managers to assimilate relevant ESG metrics into their investment processes – and provide more visibility into their firms’ governance practices.

Just how far does the industry need to go? According to 256 investors surveyed as part of bfinance’s ESG Asset Owner Survey, the hedge fund industry has much to learn. Among the respondents, only 7% of all investors (and 13% of large investors with more than $25 billion in assets under management) reported that their hedge fund and liquid alternatives managers currently offer “high integration” of ESG principles in their investment processes.

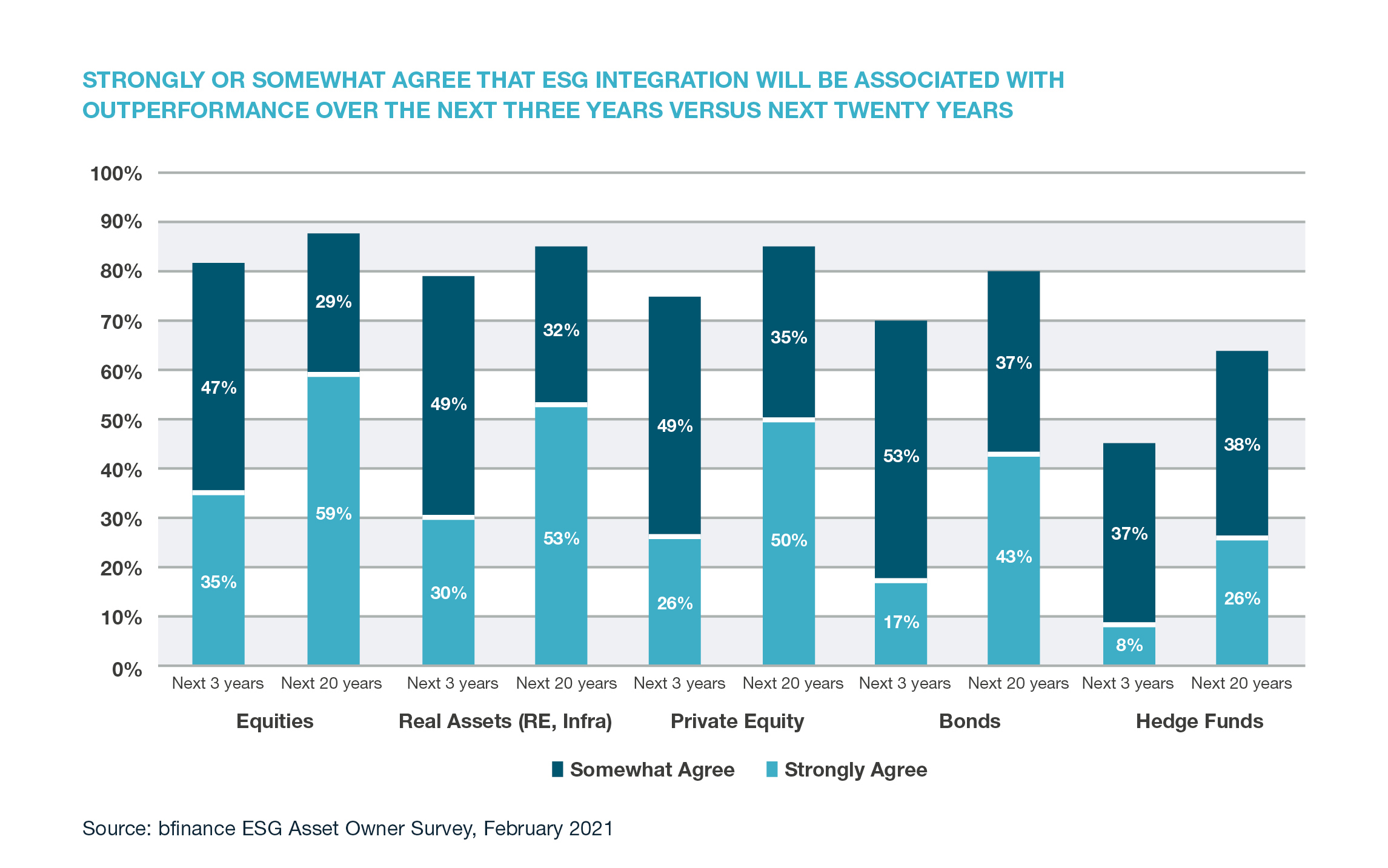

These figures are low relative to other asset classes, and even lower when we consider that 45% of all respondents in the same study envisage that ESG adoption will be associated with at least some degree of relative outperformance among hedge funds over the next three years – a figure that is lower than that seen in other asset classes but still substantial.

That expectation of relative outperformance rises significantly over the longer term. Over the next 20 years, 64% of asset owners surveyed by bfinance expect that ESG integration will be positively associated with hedge fund outperformance, compared to 88% in equities, 85% in private equity and real assets (real estate, infrastructure) and 80% in bonds.

What that ESG integration looks like, however, will vary significantly across different hedge fund strategies, some of which may remain largely untouched by sustainable investment considerations. The various forms – including screening, risk management and alpha-oriented approaches – are discussed in more detail below.

Should managers care about ESG ?

Many hedge funds are still reluctant to make ESG integral to their investment processes. The additional monitoring and reporting requirements are not yet typical of most hedge funds, nor do many have the capability for active engagement with portfolio companies in order to drive change. Hedge funds may reject the applicability of ESG considerations to the investment universe or strategy, such as short-term trading. Some argue that ‘ESG trades’ are overly crowded or are unwilling to accept a reduced investment universe.

According to a survey of hedge fund managers conducted by BNP Paribas, Hedge Funds and ESG: Finding Their Place on the ESG Spectrum, published in October 2020, some managers feel that the choice to integrate ESG is beyond their control. More than half – 56% – said that the asset classes they use, in combination with short holding periods, make ESG integration “irrelevant,” “immaterial,” or “impossible to quantify.”

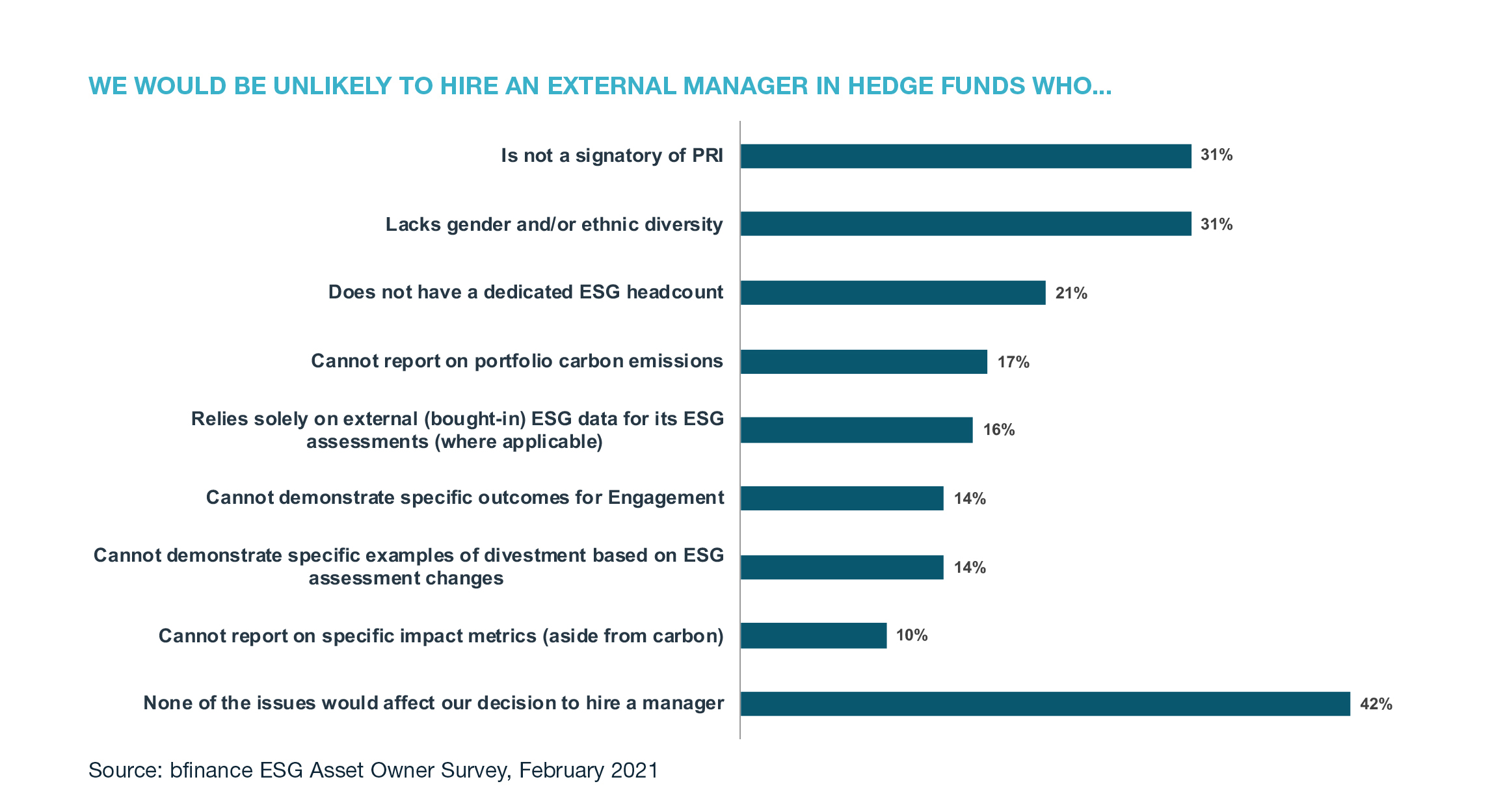

Investors, however, take a different view: Of the asset owners surveyed by bfinance, a full 60% indicated that ESG issues currently play a major role in manager selection, up from 41% in 2018. That finding was recently corroborated by market research provider HFM’s ESG Trends 2021 report, which found that 53% of institutional investors now say that ESG factors “directly impact their decision to invest with a manager.”

When it comes to manager selection, investors are not only looking at the investment strategy. Some, as shown above, screen out prospective managers based on an evident lack of diversity across their firms’ investment teams. Judging by our survey results, hedge fund managers who ignore the trend towards greater emphasis on ESG-related factors may face significant headwinds as they seek to raise additional capital in the future.

Some managers appear to be getting the message. According to the HFM report, 23% of hedge funds with more than $1 billion in assets under management are now signatories of the United Nations’ Principles for Responsible Investment (UNPRI); approximately half of those firms signed up in the past three years, while more than a quarter signed up in 2020. Based on the HFM study, managers who might have feared that ESG policies “would place constraints on returns and, by proxy, investor inflows” have had their fears assuaged: hedge fund firms managing in excess of $1 billion in assets “saw an average 32% increase in ticket sizes after signing up” to UNPRI, according to HFM.

ESG-oriented approaches in the hedge fund space

Data provided by Eurekahedge shows there are currently 65 live ESG-focused hedge funds that account for around 3% of the total hedge funds in the industry. Meanwhile, hedge funds that do not bear a specific label are increasingly adopting ESG-oriented approaches.

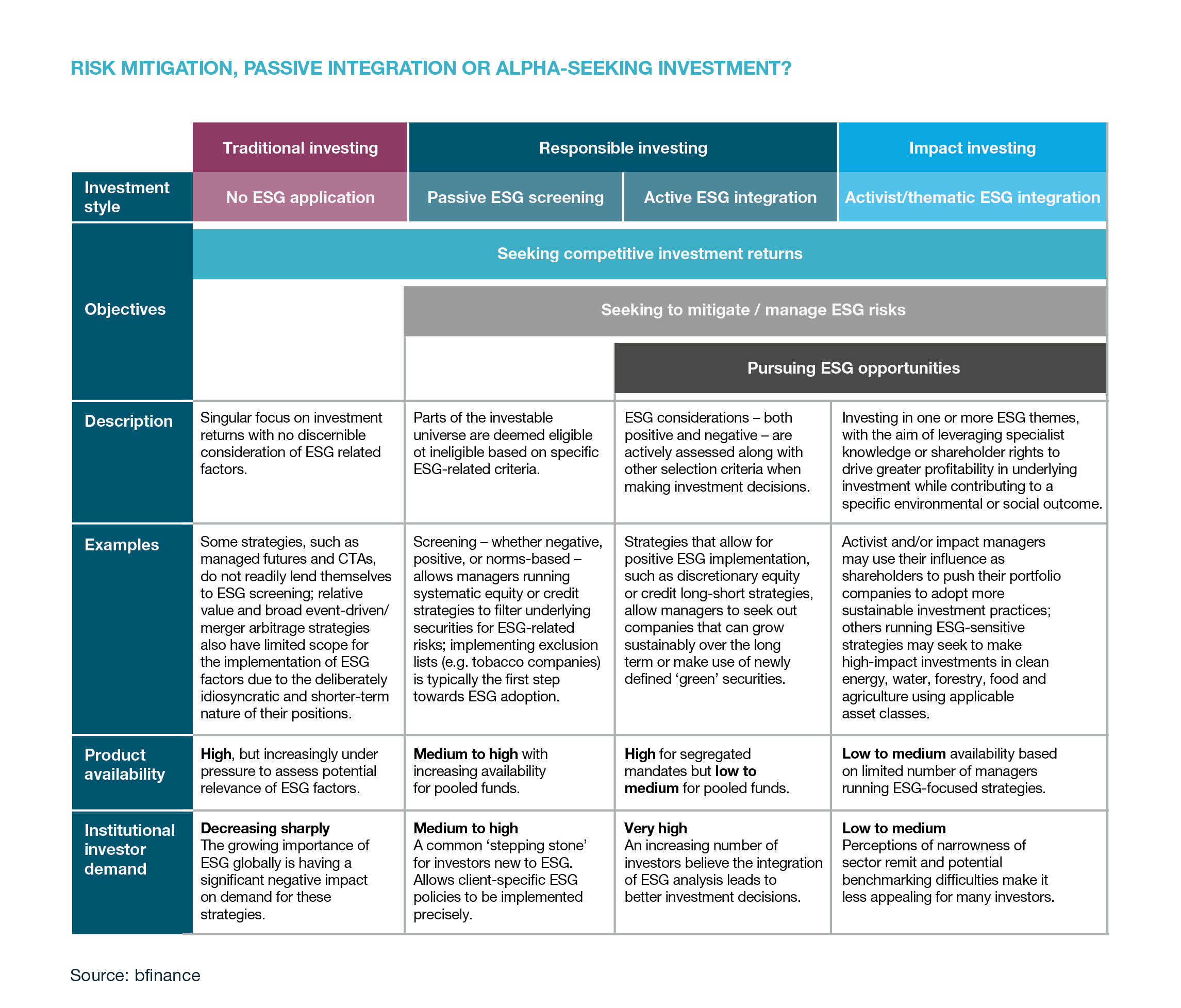

At one end of the spectrum, passive negative screening allows managers running long-short equity and credit strategies to take an ESG-conscious approach and exclude companies with unsustainable or damaging business models; similarly, positive screening enables managers to invest in companies with a commitment to responsible and sustainable business practices. Whether executed separately or in combination, passive screening amounts to the very minimum managers can do to integrate ESG without material disruption to their investment processes (and will likely be sufficient for many allocators).

At the other end of the spectrum, impact investing – and, most relevant for the hedge fund space, activist investing – go much further, empowering managers to engage directly with their portfolio companies to drive positive change. We also see a handful of boutique alternative investment firms whose strategies are predicated on the outperformance of securities with high or rising environmental ratings, such as Eco Advisors and Osmosis Investment Management. That being said, most of the hedge fund firms that are actively engaged in integrating ESG metrics right now – either by tweaking existing strategies or launching ESG variants – are large, well-established businesses with significant track records.

In the middle of the pack we find managers going beyond a laundry list of exclusions and implementing ESG within investment processes. Risk reduction is a primary driver of activity: ESG criteria can allow hedge fund firms to look at specific risk factors more accurately, as long-term, thematic macro risks such as evolving financial market regulation and country-level resource management.

Yet how easy – or difficult – is it to integrate ESG considerations into any given hedge fund firm’s investment portfolio? The answer lies in the nature of the strategy. At bfinance, we have observed a high-level split between so-called micro assets (individual equity or credit names) being more ESG-relevant than macro assets (index futures, forwards, ETFs and options, etc.). This division typically carries through to specific strategy labels as well: equity and credit long-short strategies, for example, are highly adaptable to ESG screening, whereas CTA and discretionary global macro strategies present more of a challenge.

Despite the inherent difficulties, however, even some of the largest practitioners of systematic trading and macro strategies have begun to adapt their approaches to reflect increased awareness of ESG. London-based Aspect Capital, which began integrating ESG factors in November 2020, uses company-specific ESG data as a source of “useful information on the future outperformance” and implements an overlay that creates a portfolio-level tilt towards “good” ESG assets. “It’s no longer enough to say ‘ESG isn’t relevant to our strategy,’” says John Springett, the firm’s Director of Investor Relations and Marketing.

We also see sustainability issues at play in the multi-manager sector, with providers scrambling to offer investors top-down access to ESG-focused funds-of-hedge-funds and multi-manager platforms. In March 2020, for example, J.P. Morgan Asset Management launched a Multi-Manager Sustainable Long/Short fund, which the alternatives division seeded with $100 million. In December 2020, Stamford, Connecticut-based investment firm Titan Advisors announced the launch of Titan’s first ESG-focused fund of hedge funds, Titan Eclipse, in collaboration with ESG advisory firm Flat World Partners.

The rise of ‘green’ securities

Across the industry, hedge fund managers are starting to use new products, services, securities and data to advance ESG integration. Although the process still presents challenges – sourcing reliable and consistent ESG data is difficult – managers pride themselves on their ability to extract alpha from a wide range of emerging investment products and securities. No sooner do market-makers create a new category of ‘green asset’ than managers implement strategies to trade it. In November 2019, for example, the CME Group launched trading of E-mini S&P 500 ESG futures, which are based on an ESG-filtered version of the S&P 500 Stock Index.

In fixed income, the universe of green bonds is expanding rapidly as governments seek to mitigate the economic shock of the Covid-19 pandemic and embed sustainable development goals. In September 2020, for example, Germany issued its first-ever green bonds, with a 10-year maturity, in a heavily oversubscribed floatation that raised €6.5 billion. Germany is now intent on creating a green sovereign bond curve ranging from 2 to 30 years. France and Italy have also ramped up their issuance of green bonds, and in March, the UK announced plans to issue two tranches of “green gilts” worth a total of £15 billion in 2021.

By far the largest issuance of green bonds will come from the EU itself, however, with the inauguration of the €750 billion Next Generation EU (NGEU) programme, which expects to launch its inaugural bond in June 2021, after which it will remain a regular issuer until 2026. With a planned total issuance of €240 billion in green bonds over the next five years, NGEU will soon become Europe’s largest non-sovereign issuer in the public sector.

Carbon-emissions credit trading is also expanding: A number of firms running managed futures strategies are already trading carbon emissions, particularly in Europe, which boasts the world's biggest carbon credit exchange, The European Union Emissions Trading System. For some time, investors have sought to speculate on the price of carbon credits based on existing and perceived regulations, which could filter into regional arbitrage strategies. As the European regulators extend CO2 requirements to cover more industries – and reduce the surplus of allowances in the market – regional arbitrage strategies may yet emerge: Spurred by Brexit, the UK launched its own carbon-emissions trading scheme on 1 January 2021 to replace participation in the EU’s joined-up carbon-trading market.

Hedge fund managers may also start to make use of structured products that offer niche exposure to highly specialised themes, such as reforestation and biodiversity; others may seek to apply structured solutions, such as emission-reduction overlays to mitigate carbon exposure in existing portfolios. The drive toward greater innovation seems unlikely to fade: According to BNP Paribas’ hedge fund manager survey, 55% of the respondents reported that they believe “we will see an increased demand for ESG-integrated investments post-Covid” and even larger slice – 85% of all respondents – expect to see increased requirements for ESG disclosure in the year ahead.

Learning from other asset classes

Hedge fund firms may be coming late to the revolution, but their tardiness does confer a singular advantage: their managers can look to see where mistakes have already been made by some mainstream asset management houses and avoid those missteps. When hedge fund firms, as an industry, decide to embrace ESG integration and move to meet investor demand, we expect the transition to happen swiftly. The Covid-19 crisis will not stall that progress – if anything, the crisis highlights the need for managers to think anew about future risks and opportunities in a changed world.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.