Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Ruben Mutsaers

Risk Solutions Manager

“Paying alpha fees for beta performance” has become an investor bugbear. This has created a need to differentiate more carefully between outperformance derived from established risk factors and outperformance based on idiosyncratic risk exposures.

With the emergence of factor investing and a greater understanding of systematic risk premia, the definition and delivery of “alpha” has become an increasingly complex and even controversial topic. Assessing performance in excess of a conventional market benchmark remains mainstream practice. Yet recent years have brought increasing scrutiny of the sources of return.

For example, an investor selecting a style-oriented strategy, such as a value equity manager, may well wish to monitor whether outperformance is being delivered in conjunction with exposure to the relevant factor or whether the manager has veered away from the expected style in search of returns. An investor selecting a manager in a particular asset class may need to understand how much of their performance has been based on leveraging up or dialling down exposure to market risk.

More fundamentally, there is a growing belief among pension funds and other sophisticated institutional investors that there is a different price tag associated with the outperformance that can be attributed to factor exposures and the outperformance beyond those factor exposures, which is seen to represent a purer category of manager skill.

The rise of semi-passive and “smart beta” products – which theoretically offer a cheaper access point to well-understood risk premia such as value, momentum and low volatility – have created new pricing tensions. We can already see the effects of pricing tension in the lower fees commanded by systematic active equity strategies versus fundamental strategies (see Investment Management Fees: Is Competition Working?). Yet the same rationale can be applied to fundamental managers.

In practice, converting this belief into a viable analytical approach is far from straightforward. “Alpha” is a personal property: different investors bring different philosophies on defining outperformance, different beliefs on subjects such as factor performance and factor timing, different portfolio construction methodologies, and different wishes in terms of the types of exposures they wish to see among their active managers.

Better benchmarks?

How should manager performance be assessed, in addition to the classic measures of relative return versus conventional market benchmarks and absolute return?

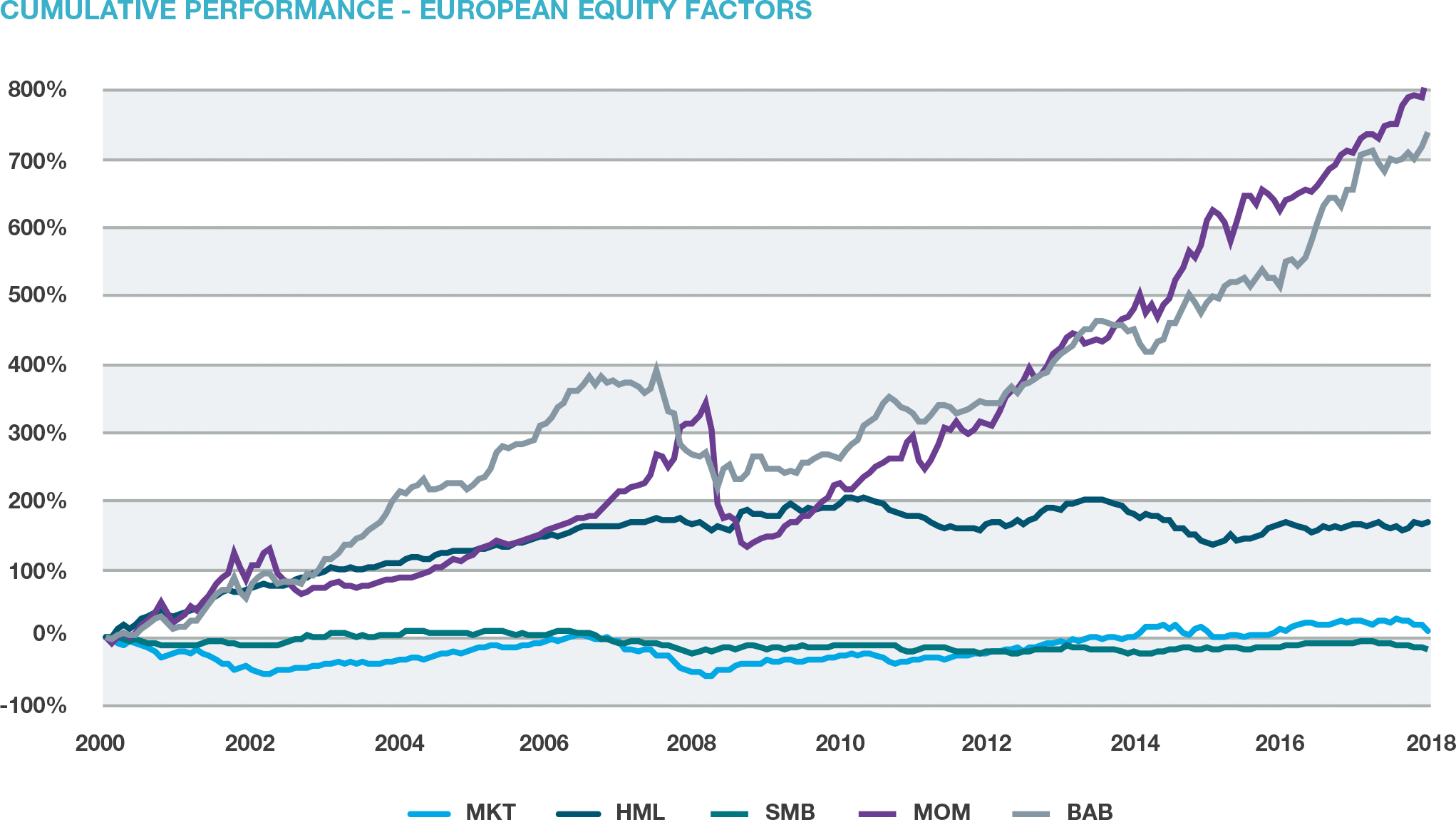

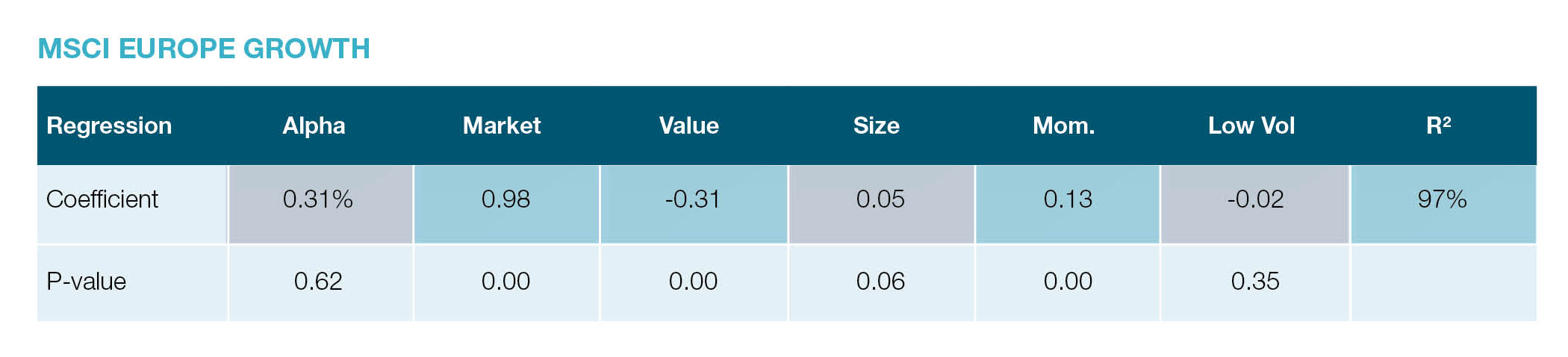

One relatively simple approach may be to assess manager performance versus widely accessible style indices. This has the advantage of being a transparent, investible comparator. Yet the insights provided by such analysis are limited. It is important to realise that a style is never just a style. “Growth” is not just “growth”: growth means exposure to a range of other factors as well. A style assessment of the MSCI Europe Growth index shows this well:

This index includes significant growth exposure (negative coefficient to value), but also significant small cap exposure and momentum exposure. This means that when we would use the MSCI Europe Growth as a benchmark, what we are really comparing against is a collection of factors. Similarly, the MSCI Europe Value index has a notable tilt away from the momentum and size factors.

Another approach that we have found particularly interesting and useful is generating specific tailored benchmarks that match a particular manager, using factors as building blocks and tailoring exposures to the manager’s investment process. This helps to (a) check manager delivery of style exposure, (b) isolate manager skill beyond style exposure and (c) provide insight into the consistency of manager skill.

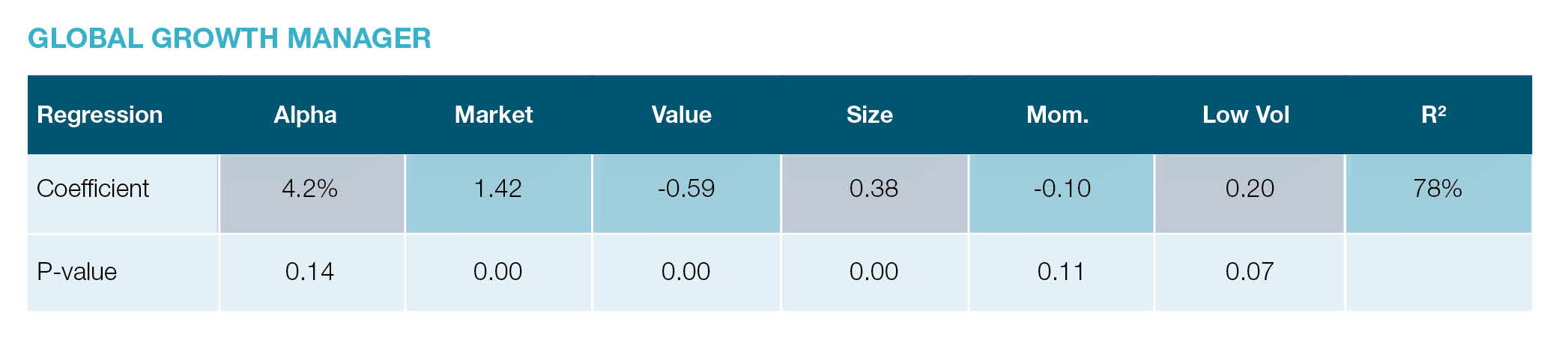

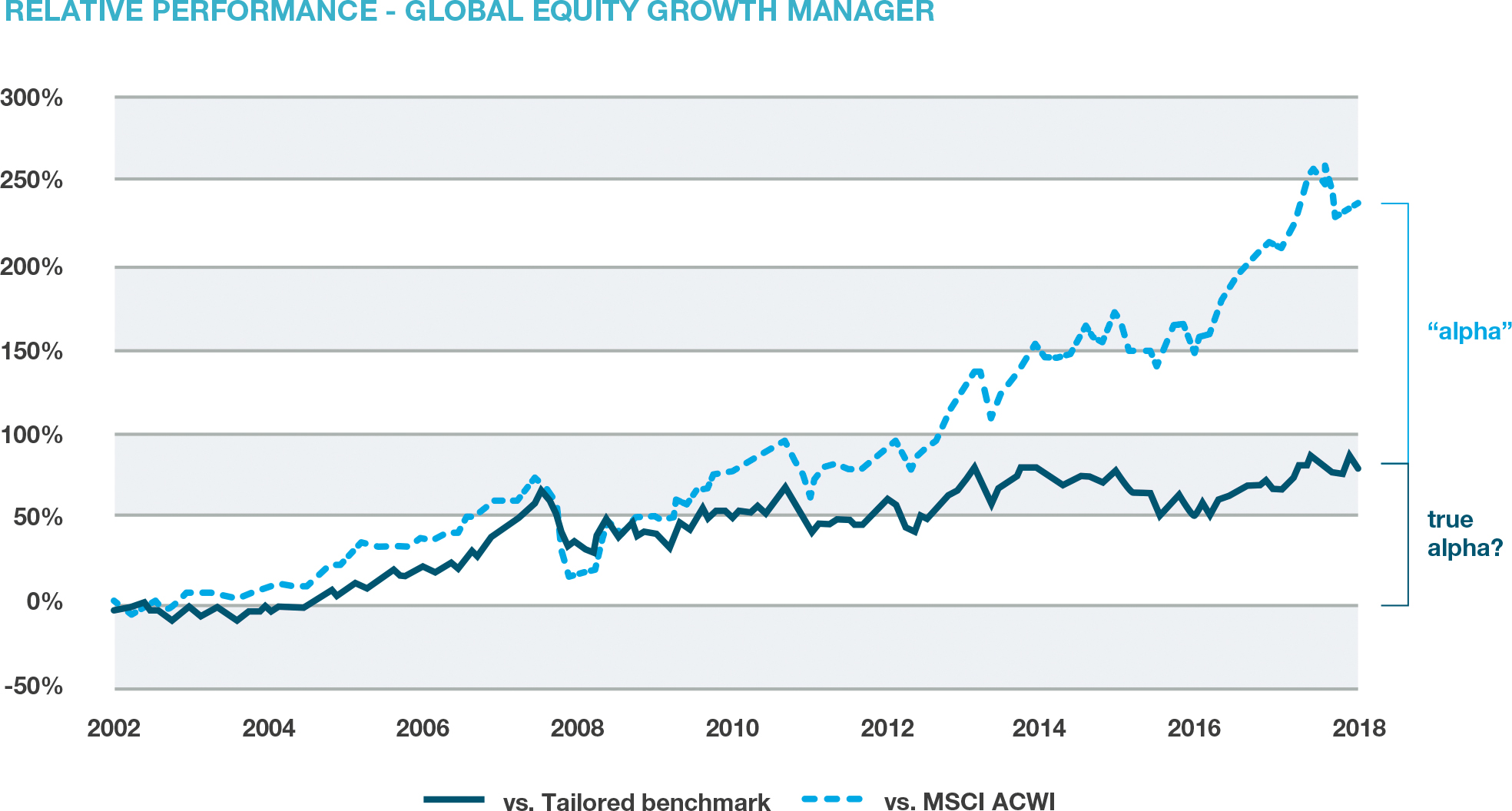

One interesting example was a recent review of a Global Equity Growth manager. The manager describes itself as “high octane” “long-term growth” and had indeed generated significant outperformance versus regular market indices. Yet are they, in fact, worthy of a higher fee than their peers?

As it turns out, this ‘high octane’ manager has a beta of 1.4, substantial growth exposure (-0.6) and significant small cap exposure. This chart shows how our assessment of relative performance is affected if we build a benchmark of these factors and exposures. There is manager skill in delivering such factor exposures and sticking with them, but this analysis is hugely empowering in value-for-money assessments. All of the regression alphas shown here are calculated on an annualised basis and, as such, are directly comparable to an annual investment management fee.

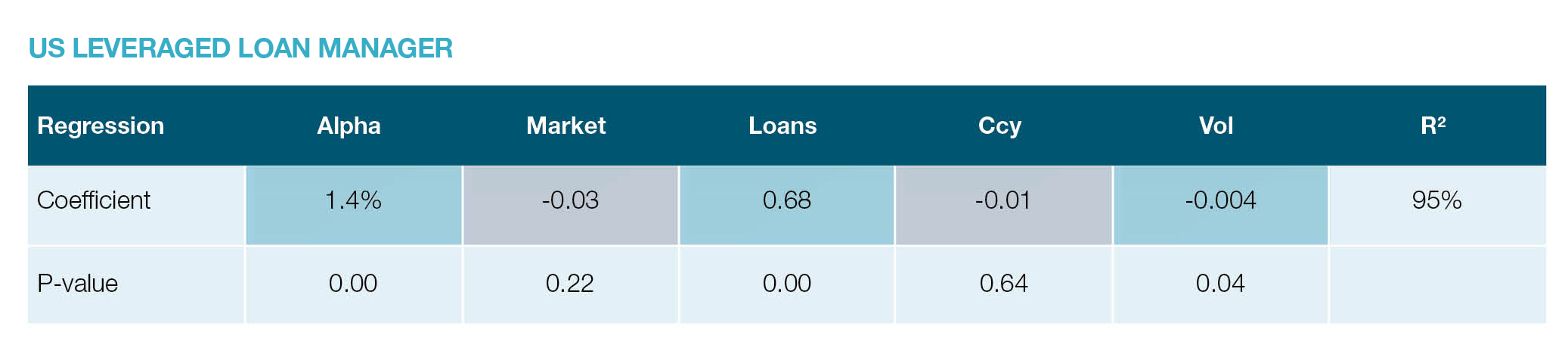

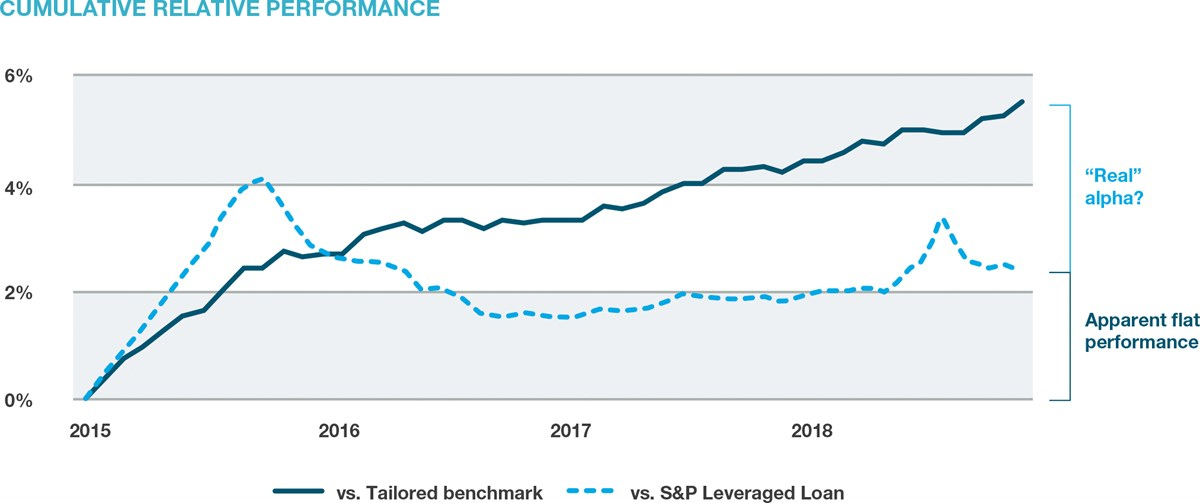

Style analysis and attribution can cut both ways: it may well show the strengths of a manager that appears to be performing poorly. Consider the following US Leveraged Loan manager, whose client had strong reservations about their performance versus the benchmark, which had effectively been flat for a number of years. A factor model and performance attribution reveals more:

In this case, a tailored benchmark acknowledges the manager’s lower risk profile with a beta to the S&P Leveraged Loan index of only 0.68. A performance comparison directly versus the S&P Leveraged Loan index (implicitly assuming a beta of 1.00), could “punish” the manager for simply having a lower risk profile than the benchmark. This has a big impact on the client’s perception of outperformance (see graph). The regression alpha for this manager, in this analysis, worked out at 0.12% on a monthly basis and 1.4% on an annualised basis. Of course, the interpretation of this finding depends on whether the investor wanted the manager to maintain a lower risk profile or not.

Assessing value for money is more art than science, given investors’ different attitudes and needs. Yet stronger analytical tools, if used sensitively, can add a great deal of clarity to discussions on performance and fees.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.