Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

The latest facts and figures.The TMB market has nearly quadrupled since 2008 to c. $300 billion. This research note provides an at-a-glance digest of market size, issuer numbers, asset manager and fund universe, expected returns, historic default rates and more.

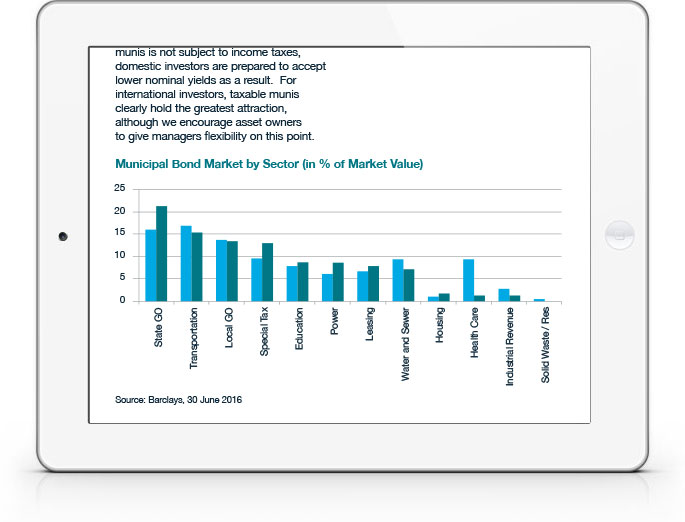

Introduction to the asset class. There are multiple types of munis with different characteristics: GO bonds versus Revenue bonds linked to different sectors and thus featuring different credit risk profiles, tax-exempt versus taxable, and the now-discontinued Build America Bonds.

What makes a strong manager? The severe inefficiencies in this market, which include its continued domination by retail investors, make it a strong candidate for active management. But muni managers’ core expertise lies in tax-exempt bond investment for a domestic clientele. Important differentiators include buy-and-hold versus total return strategies, credit research capabilities, the integration of experienced traders into the investment decision-making process and effective dealer coverage. Fund size can be a blessing and a curse.

WHY DOWNLOAD?

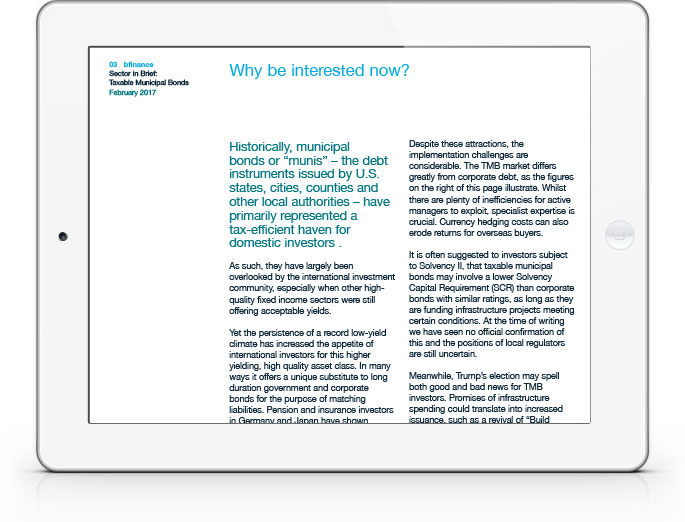

Historically, municipal bonds have primarily represented a tax-efficient haven for U.S. investors, widely overlooked by the international community.

Yet the persistence of a record low-yield climate has increased the appetite of international investors for this higher yielding, high quality asset class. Pension and insurance investors in Germany and Japan have shown particularly strong interest, as evidenced by recent bfinance manager searches. Simultaneously, U.S. muni bond managers have surged offshore, drawn by the opportunity to grow and diversify their client base.

The vast majority of the US$1.7 trillion municipal bond market still comprises tax-exempt bonds, whose yields are typically depressed due to the income tax advantage. Yet the smaller taxable municipal bond (TMB) sector offers more appeal to overseas buyers. The TMB market has nearly quadrupled since 2008 to c. $300 billion and has been one of the highest performing investment grade fixed income sectors over the past decade, albeit with higher volatility than corporate bonds.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.