Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Julien Barral

Director, Equity Research

Investors today are being presented with an increasingly diverse and confusing menu of smart beta strategies. The newest products claim to incorporate the latest research innovations, particularly those concerning the construction and implementation of portfolios.

It is sometimes assumed that raising the tracking error constraints could lift the excess return from the 1% to the 2%-plus mark. That is not the case in practice.

This new generation is particularly evident in “multi-factor smart beta,” perhaps for the simple reason that it is the most complex segment of the smart beta landscape from an implementation perspective. Issues such as rebalancing frequency become more challenging in a multi-factor context. There are numerous different ways of combining multiple factors in the same portfolio. Bringing multiple factors together also raises the question of factor timing – the debate that apparently won’t go away.

DEALING WITH DIVERSITY

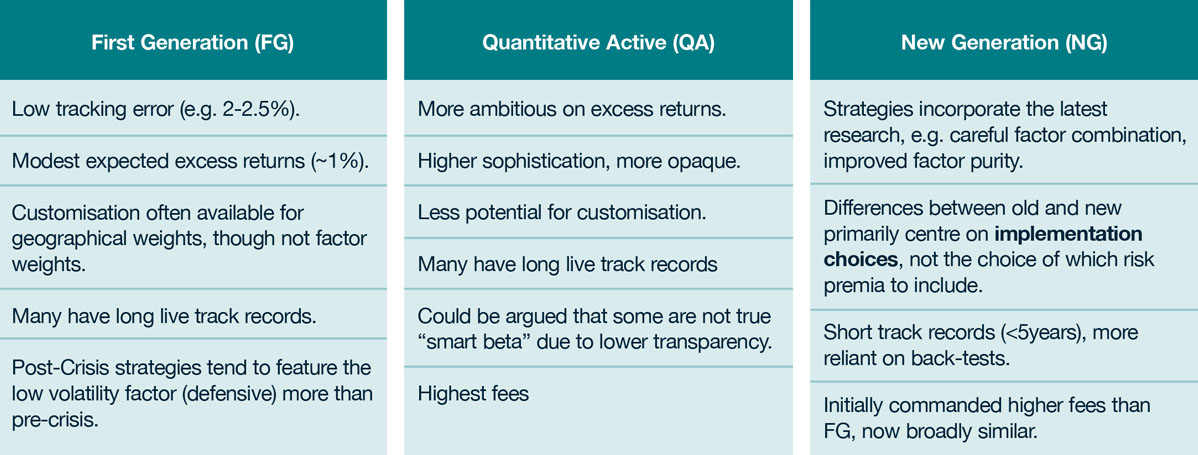

There are many ways that one could break down the multi-factor smart beta product universe, such as tracking error level or factor type. During recent smart beta projects for investors around the world, we have found it rather useful from a practical perspective to think about three families: First Generation, Quantitative Active and this younger group of New Generation strategies.

The multi-factor smart beta universe:

The First Generation (FG) family includes low tracking error products that claim to deliver a small excess return (e.g. 1%) over the benchmark over the long term. These are familiar, long-established, highly transparent strategies that can be customised to some degree, such as weighting country exposures according to investors’ internal benchmarks, although the factor weights themselves are typically not customisable.

By contrast, the Quantitative Active (QA) family might not fall comfortably within everyone’s definition of smart beta: although fully systematic and rules-based, the rules used to construct the portfolio are not always transparent. There is something of a “secret sauce” attitude involved, which is not to everyone’s taste in this context. Although significantly cheaper than fundamental active management, these are pricier than FG strategies. Yet it does often make sense to include them, perhaps for one reason above all others. The awkward truth is that many investors searching for smart beta, particularly for the first time, are initially hoping for greater excess performance than FG approaches are likely to provide and QA strategies, by way of comparison, do present more ambitious return targets.

Indeed, the subject of target return is the focus of many of our conversations with investors. It is sometimes assumed, for instance, that raising the tracking error constraints on FG strategies could lift that excess return figure from the 1% to the 2%-plus mark. Yet those presumptions are not borne out by practice. The amount of tracking error in this space is usually directly linked to the proportion of low volatility exposure rather than the expected return. When investors press the point, managers push back strongly against constructing or customising more aggressive versions of FG strategies.

The New Generation (NG) family are somewhat closer to First Generation strategies in terms of return objectives and transparency.

Smart beta was initially intended to be simple and cheap. But we must remember: there is no completely simple decision

According to estimates developed by Harvey, Liu, and Zhu (2016), approximately 40 new factors are announced each year, in addition to the 300 or so that have currently been published. Yet, in most cases, the innovations underpinning the New Generation products do not revolve around new factors: they primarily involve construction, implementation and execution.

One interesting example is the group of young strategies that supposedly deliver greater “factor purity” or “higher factor efficiency” (aka “High Factor Exposure” per EDHEC, “enhancing informational efficiency” per GSAM, or “orthogonalization” per HSBC). This is the result of portfolio construction techniques which range from the highly quantitative to the more straightforward (e.g. stock exclusions). The objective is usually to eliminate “factor losers” in the context of a multi-factor portfolio.

IMPLEMENTATION INNOVATION

In 2017-18, publication after publication has trumpeted the importance of smart beta providers’ implementation differences - the sources of the significant performance dispersion among strategies that target nominally similar factors. Investors are now faced with a barrage of messages telling them that these differences matter.

They range from stock weighting schemes to trading methods that minimise market impact. AQR has coined a new term for this collection, which will make many smart beta advocates recoil: “Craftsmanship Alpha”. In a new paper bearing the same name, published in The Journal of Portfolio Management, Asness and co. lay out ten different decision-making steps where practitioners will differ. It is a very helpful shortlist:

Ten sources of performance dispersion between "similar" smart beta strategies

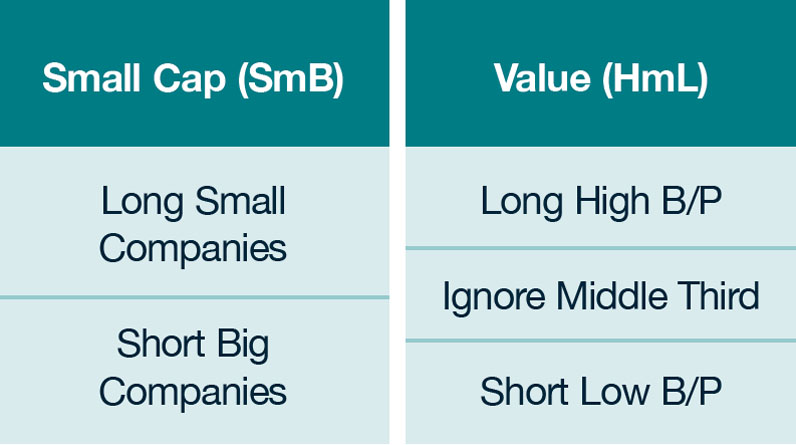

Smart beta was initially intended to be simple, and cheap. But we must remember: there is no completely simple decision. Even the venerated Kenneth French engaged in a few strategic choices when he chose a different selection scheme for Value versus Size, and probably did so simply because it worked better on the historic data, which is not a solid basis for a forward-looking implementation decision.

Kenneth French's (back-fitted?) implementation choice

This AQR list also makes it clear why New Generation approaches are particularly relevant in the multi-factor segment of the smart beta world. Many managers have focused on improving factor combination methodologies (e.g. aggregating signals for different factors before stock selection or not) and factor independence (avoiding double counting), with an awareness that various approaches can rely in overly diluted exposures, problematic contra-bets or unintended tilts.

The combination challenge is complicated further by the time variation between different factors – a point that Richard Wiggins (who works at a large Middle Eastern corporate pension fund) summarised aptly in a recent Institutional Investor article: “Momentum is like watercress,” he writes, “ready for harvest about 14 days after it’s sown. But value is like snap beans, which take nine or ten weeks to mature. Forcing all into one basket and rebalancing (“harvesting”) at the same time creates a whole new set of issues.”

Meanwhile, the issue of strategic allocation (static) versus tactical allocation (timing) of multiple factors rumbles on: the very public AQR versus Research Affiliates showdown on the subject in 2017 has not resolved the question. What we find in practice, when scrutinising products, is that even some managers who don’t officially believe in timing factors are actually doing a little bit of tilting towards the winning styles.

LOOKING AHEAD

It is immensely positive, from the perspective of investors’ interests as well as the sector’s sustainability, that the managers’ different implementation methodologies are now being more closely scrutinised, and that the importance of these differences is better understood.

It is also healthy that this examination is driving product innovation, although investors should always have a sharp eye on back-testing, over-fitting and “p-hacking” (crunching masses of data to find an approach that gives a good p-stat, then working backward).

Over the coming years we will be watching with great interest to see how these implementation improvements play out in live track records.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.